Worldwide Multi‑Sensor & Multi‑Directional Security Camera Market: Strategic Imperatives for 2026

PW Consulting’s new market brief on the Worldwide Multi‑Sensor and Multi‑Directional Security Camera Market synthesizes seven years of historical performance and a seven‑year forecast to deliver a decision‑grade intelligence package for executives planning capital, procurement, and technology roadmaps in 2026. The market has demonstrated robust expansion—more than doubling in scale since 2020—and our forward projection to 2032 reflects sustained, high‑teens growth driven by converging forces in AI, edge compute, and public infrastructure investment. This release highlights the strategic takeaways CIOs, CPOs, and security system integrators need now, while reserving the full segmentation matrices and vendor scorecards for report subscribers.

Worldwide Multi-Sensor and Multi Directional Security Camera Market

Why this market matters to 2026 decision‑makers

- Scale and momentum: The market’s trajectory shows a rapid shift from early adoption to mainstream deployment across government, transport, and large commercial campuses. Our consolidated view shows strong year‑over‑year expansion through 2025 and a forecast path to 2032 that underpins multi‑year procurement planning.

- High growth, concentrated competition: Compound annual growth remains elevated as enterprises invest in wide‑area situational awareness and cost‑efficient device consolidation. Market concentration is meaningful—leading suppliers command a sizeable share of installed base and R&D investment—creating both opportunities for premium differentiation and risks for buyers tied to single‑vendor roadmaps.

- Technology leverage point: Advances in onboard AI (serverless inferencing), multisensor fusion, and PoE++ power delivery are reducing total cost of ownership for wide‑area coverage while increasing the value of analytics. This is shifting procurement decision criteria from pure hardware price to integrated analytics, manageability, and compliance capability.

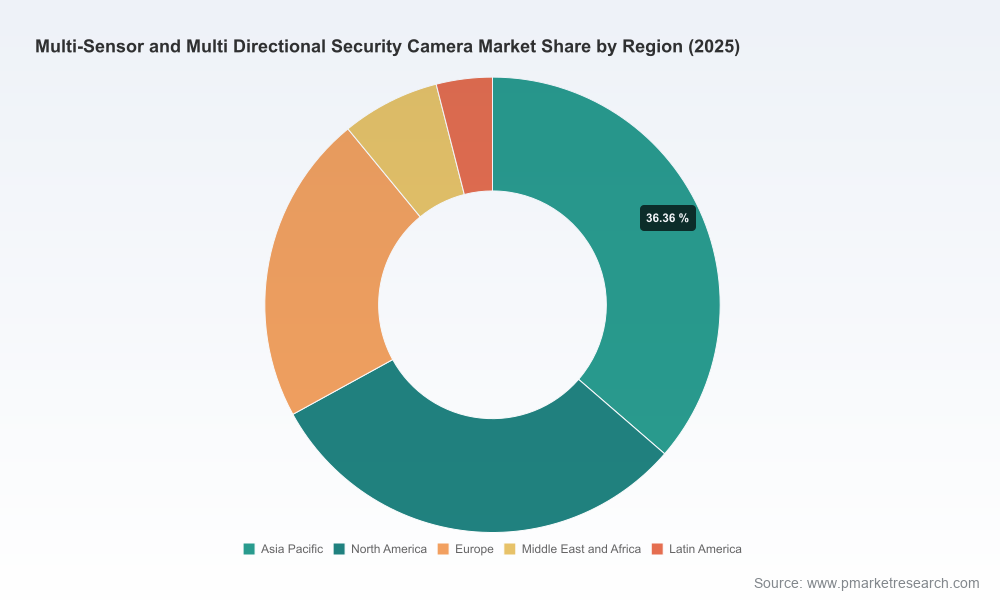

Data snapshot (high‑level)

Our modeling captures the market’s evolution from an early phase in 2020 to a structurally larger, more commercially viable industry by 2025, with a multi‑year forecast that assumes continuation of current technology adoption curves, regulatory dynamics, and infrastructure spending programs. The report quantifies this trajectory and translates it into procurement runway scenarios and budget implications for 2026–2032. For confidentiality and to preserve the tactical value of the report, the granular split tables and regional/application line items are available only in the subscriber deliverable.

Worldwide Multi-Sensor and Multi Directional Security Camera Market

Key market dynamics shaping 2026 choices

- Edge AI and serverless analytics: The move toward onboard inferencing (e.g., NVIDIA Jetson integrations and vendor‑specific ASICs) changes architecture decisions. Deployments that once required server racks for video analytics can now run perceptual models at the camera, reducing latency and bandwidth while increasing privacy controls. Procurement plays must evaluate model TOPS, update pathways, and lifecycle provisioning.

- Consolidation of coverage vs. sensor specialization: Multi‑sensor designs enable fewer physical nodes to cover wider footprints, but they also introduce dependence on stitching, synchronization, and consistent optics. Buyers must balance the capital savings from fewer units with the operational requirements of more complex firmware, calibration, and maintenance.

- Interoperability and standards: ONVIF and network video standards remain a gating factor for integrator flexibility—and in many government contracts, NDAA compliance is now a threshold requirement. These regulatory and standards backdrops materially affect sourcing, warranty risk, and lifecycle upgrade paths.

- Deployment economics: Power delivery (PoE++), cabling, and mounting strategies represent a substantial portion of installed cost for wide‑area projects. Strategic choice of camera architecture (fixed multi‑sensor vs. PTZ‑hybrid vs. motorized multi‑imager) has ripple effects across civil works, connectivity, and long‑term maintenance budgets.

Competitive landscape: what the supplier map means for buyers

We profile more than a dozen suppliers across product archetypes—from cloud‑native providers to legacy OEMs now offering multi‑sensor portfolios. The market is neither fully fragmented nor monopolized: the top vendors hold a meaningful share but competition remains vibrant, particularly around AI capabilities, system integration, and compliance credentials.

Worldwide Multi-Sensor and Multi Directional Security Camera Market

- Large OEMs with broad portfolios: Firms with deep R&D and global channel reach continue to push integrated multi‑sensor options that pair high‑resolution imaging with on‑device analytics and enterprise VMS compatibility. These players are attractive for complex, multi‑site rollouts where global support and lifecycle services matter.

- Cloud‑first entrants: Newer vendors emphasize cloud management, SaaS analytics, and simplified install paths (PoE++), appealing to retail and midmarket customers seeking lower first‑stage operational overhead and rapid scale‑up.

- Regional specialists and niche innovators: Companies focused on ruggedized environments, transportation hubs, or industrial settings differentiate through optics, environmental sealing, and specialized AI models tailored to domain‑specific detection needs.

Recent vendor moves illustrate the dynamic competitive posture in the market: a leading OEM's 2024 launch of a multi‑channel AI camera leveraging Jetson‑class processing signals a broader industry trend toward serverless analytics. In 2026, several established manufacturers refreshed NDAA‑compliant multisensor lines, underscoring how regulation reshapes product roadmaps and supplier selection. The full vendor profiles, product comparisons, and procurement scorecards are included in the full report.

What our report delivers — the practical toolkit for 2026

PW Consulting’s report is structured as an operational playbook rather than a high‑level briefing. Key components include:

- Actionable market sizing and scenario forecasts to align multi‑year procurement budgets with likely adoption curves.

- Technology archetype maps that compare multi‑sensor fixed, multi‑directional adjustable, and PTZ‑hybrid solutions against use‑case suitability, lifecycle cost, and integration complexity.

- Vendor assessment frameworks and a five‑axis scorecard (technology, compliance, support, integration, TCO) to accelerate RFP shortlists.

- Deployment blueprints and installation cost drivers (power, mounting, cabling), including recommendations to optimize for PoE++ and edge‑compute strategies.

- Procurement templates, sample RFP language, and evaluation checklists that incorporate compliance (NDAA, export control awareness) and interoperability (ONVIF, VMS compatibility).

- Risk matrix and mitigation playbook covering supply‑chain dependencies, firmware security, and model drift for AI analytics.

Strategic recommendations for 2026 planning cycles

- Prioritize sensor economics over upfront unit price: Evaluate per‑coverage and per‑analytic cost over a 5–7 year horizon. Multi‑sensor consolidation can lower unit counts but requires assessing firmware update cadence and replacement pathways.

- Insist on verifiable AI and security lifecycles: Require patch schedules, model update guarantees, and demonstrable adversarial testing as part of procurement contracts.

- Design for hybrid edge/cloud architectures: Architect solutions that allow analytics to run on‑device for low‑latency needs, while leveraging cloud services for centralized management and archival analytics—this balances bandwidth and operational resilience.

- Embed regulatory compliance into supplier evaluation: NDAA and export controls are not checklist items—they influence supplier availability, warranty support, and future upgradeability. Include compliance as a pass/fail gating criterion for government and critical infrastructure projects.

- Use vendor scorecards to avoid single‑source lock‑in: Given meaningful concentration among top providers, structure procurement with interoperability clauses and phased adoption to retain future flexibility.

How to use this research in boardroom and procurement cycles

Security and infrastructure investments are increasingly strategic, touching privacy, legal, and operations. The report provides materials designed to inform: capital request narratives; total cost of ownership models; migration roadmaps from legacy PTZ fleets to multi‑sensor arrays; and sample SLA language for managed services. For C‑suite and procurement leaders, these deliverables translate technical options into financial and risk outcomes so that spending decisions align to broader enterprise objectives.

Conclusion — the signal amid the noise

The multi‑sensor and multi‑directional camera category has matured into a strategic component of modern surveillance architecture. For 2026, the intersection of edge AI, regulatory pressure, and infrastructure modernization creates a narrow window where well‑timed, standards‑aware procurement can yield durable benefits. PW Consulting’s new report translates macro growth trends and supplier dynamics into executable guidance—while reserving the detailed segmentation, vendor benchmarking, and deployment models for report subscribers who require the full, decision‑ready dataset.

Next steps

Executives preparing 2026 capital plans should request PW Consulting’s full report to obtain the complete segmentation tables, vendor scorecards, and ready‑to‑use procurement artifacts. The full deliverable contains the detailed datasets and appendices necessary to convert high‑level strategic intent into procurement and deployment actions.

For detailed analysis of this topic, please visit the official page:Worldwide Multi-Sensor and Multi Directional Security Camera Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com