Worldwide Micronized Silica Market: Strategic Outlook for 2026 Decision-Making

PW Consulting’s new Worldwide Micronized Silica Market study (base year 2025; forecast period 2026–2032) is being released as an indispensable strategic briefing for industrial leaders, investors, and procurement executives preparing for the 2026 planning cycle. Combining a detailed historical view (2020–2025), a robust scenario-based forecast, and an actionable playbook, the report translates industry complexity into concrete choices—without giving away the proprietary sub‑segment matrices that make the difference in a competitive bidding environment.

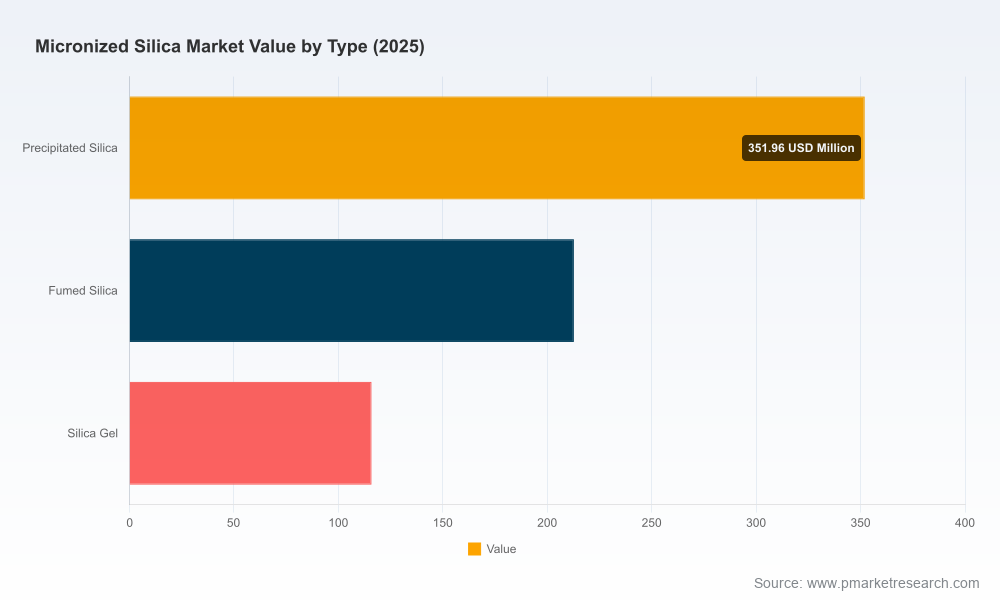

Worldwide Micronized Silica Market

Executive snapshot

The micronized silica market demonstrated steady expansion over the 2020–2025 period, moving from a mid‑hundreds million USD base to an estimated market size of roughly USD 680.6 Million in 2025. Our modelling anticipates an average compound annual growth rate (CAGR) of 6.8% across the 2026–2032 forecast window, guiding the market toward an equilibrium in the high triple‑digit million USD range by 2032.

Worldwide Micronized Silica Market

Two structural features shape near‑term strategy: moderate market concentration (the three largest suppliers together account for a meaningful share, while the top five command just over half of global revenues) and a demand profile increasingly shaped by advanced end‑uses such as battery materials, pharmaceuticals, optical coatings and high‑performance composites. These characteristics generate both scale advantages and niche opportunities for differentiated players.

Worldwide Micronized Silica Market

Why this report matters for 2026 planning

- Translate macro momentum into capital allocation: The 6.8% CAGR in our base forecast is not uniform across applications or geographies. For 2026 budgeting, CFOs and corporate strategy teams need to identify which product grades and value chains will capture premium growth—and where to defer or accelerate CAPEX.

- Inform sourcing and inventory policy under volatility: Recent feedstock and logistics shocks have increased working capital risk. Procurement teams will benefit from the report’s stress‑tested supply scenarios and hedging templates tuned to silica’s supply dynamics.

- Shape product and regulatory roadmaps: Regulatory shifts require product reformulation and compliance roadmaps well ahead of market deadlines. The report maps regulatory timelines to product development milestones for 2026 and beyond.

- Prioritize M&A and JV targets: With a moderately concentrated market structure, there is an emergent premium on bolt‑on acquisitions that bring either specialized grades or regional logistics footprint. Our target screening narrows the opportunity set for strategic acquirers.

What the report contains (practical, transaction‑ready modules)

- Comprehensive market sizing and validated growth scenarios (base year 2025; 2026–2032 forecast) with sensitivity analyses to feedstock, freight, and tariff shocks.

- Demand maps by end‑use, linked to downstream adoption curves and price elasticity estimates (delivered as decision rules rather than raw segment tables to preserve client advantage).

- Supply chain heatmaps and supplier cost stacks, including primary cost drivers, regional logistics corridors, and capital intensity benchmarks for micronizing technologies.

- Regulatory and product compliance matrix—timeline, impact severity, and mitigation playbooks—for key jurisdictions and use cases.

- Competitive landscaping and capability benchmarking focused on technology competence, grade portfolios, and channel access.

- Investment and M&A playbook with valuation frameworks, synergy hypotheses, integration checklists, and red‑flag diagnostics for deal teams.

- Commercial go‑to‑market playbooks: pricing architecture, customer segmentation, and contract templates tailored to micronized silica customers.

Key market dynamics shaping 2026 strategy

Several contemporaneous dynamics increase both risk and optionality for companies operating in the micronized silica domain.

- Input cost pressure: Sodium silicate feedstock experienced a material price uptick (double‑digit YoY movement in late 2025), which compresses incremental margins on standard grades and accelerates demand for higher‑value differentiated chemistries.

- Logistics volatility: Ocean freight surcharges and episodic route disruptions increased landed cost volatility in early 2025. For 2026, commercial teams should bake route and schedule risk into contract terms and working capital models.

- Trade policy shifts: Elevated import tariffs on certain trade lanes have altered arbitrage flows, prompting regional supply adjustments and localized sourcing strategies.

- Regulatory tightening: New restrictions on nano‑sized particulates in consumer sprays require product reformulations and labeling changes—creating a compliance cost for generalist suppliers and an opening for certified specialty producers.

- Transport classification and handling: While micronized silica remains classed as non‑hazardous for standard road/rail transport in most jurisdictions, operational controls for dust suppression are increasingly mandated at warehousing and intermodal interfaces.

Competitive landscape — what to watch in 2026

The market is dominated by a cohort of global chemical and specialty mineral companies that mix capacity scale with application know‑how. Several leading players are actively investing in capacity, product innovation, and certification to capture growth in high‑value segments.

- Evonik Industries AG (Essen, Germany): Recognized for fumed and precipitated micronized grades, Evonik’s recent capacity expansion to support battery and pharmaceutical demand signals a strategic bet on advanced applications. Expect continued capital deployment into capacity that supports controlled particle morphology and purity.

- W.R. Grace & Co. (Columbia, MD, USA): With brands focused on anti‑blocking, matting and flow enhancement, Grace’s recertification moves for food and pharma markets improve access to regulated end‑markets—an advantage for customers seeking compliant suppliers in 2026.

- PPG Industries (Pittsburgh, PA, USA): PPG’s updated micronized silica portfolio with low‑VOC options reflects an industry trend toward sustainability‑aligned formulations, particularly in coatings and cosmetics.

- Cabot Corporation (Boston, MA, USA): Recent hydrophobic micronized grades targeted at optical and LED applications position Cabot for growth where transparency and refractive index control are critical.

- PQ Corporation, Innospec, Sibelco, Quarzwerke, Arkema, Imerys: These firms collectively pursue niches—anti‑slip flooring, fuel additives, specialty fillers, plastics reinforcement—that together broaden the market’s technical depth. Strategic moves tend to be focused on product differentiation rather than price competition.

For 2026 planners, the competitive implication is clear: scale will protect margin in commoditized grades, while technical differentiation and compliance certifications will capture outsized returns in regulated and high‑performance end‑uses.

Strategic playbook for executives in 2026

We propose a pragmatic set of options tailored to company scale and ambition. Each option is supported by the report’s scenario outputs, cost‑curve models, and go‑to‑market playbooks.

- For integrated majors: Accelerate capacity and grade specialization in battery and pharma applications where purity and morphological control command premiums. Protect margin with forward hedges on feedstock and multi‑year logistics contracts.

- For mid‑sized specialists: Double down on certification (pharma/food/optical) and secure niche distribution partnerships. Consider targeted M&A to acquire localized logistic capabilities and customer relationships in high‑growth corridors.

- For processors and tollers: Offer low‑risk contract manufacturing and certification support to brands seeking rapid reformulation. Invest in dust control and compliance systems to turn safety into a commercial differentiator.

- For private equity and strategic investors: Use the report’s valuation templates to screen targets that either consolidate regional fragmentation or provide proprietary grades with defensible margin profiles.

Practical near‑term moves (90–180 days)

- Run a short‑list of suppliers against feedstock and freight scenario stress tests in the report to renegotiate 2026 supply terms.

- Prioritize product certification workstreams where regulatory timelines could impose market access limitations.

- Initiate a rapid M&A diligence for 1–2 bolt‑on targets identified in our screening matrix to secure distribution or grade specialty.

- Deploy margin‑preserving price escalation clauses linked to clearly defined feedstock and freight indices.

How to use our analysis in boardroom decisions

PW Consulting’s study is structured to support board level and operating committee decisions alike. Use the report to:

- Validate or challenge internal forecasts with independent scenario outputs;

- Quantify CAPEX tradeoffs using supplied NPV and payback templates calibrated to silica‑specific cost drivers;

- Frame M&A cases with synergy checklists, integration risk matrices and quick‑win commercialization plans;

- Build procurement playbooks that lock in supply while maintaining flexibility amid tariff and freight volatility.

Conclusion and next steps

The micronized silica market entering 2026 presents a rich but nuanced opportunity set. Growth—anchored by an approximate mid‑single digit CAGR across 2026–2032—will reward firms that combine technical grade leadership, regulatory foresight, and fortified supply chains. PW Consulting’s report delineates where to place strategic bets and where to preserve optionality.

To preserve the commercial value of our in‑depth segment tables, regional splits and proprietary pricing ladders, this release intentionally summarizes high‑level conclusions and actionable frameworks while withholding granular sub‑segment data. For teams preparing 2026 budgets, M&A pipelines, or product roadmaps, access to the full report will deliver the detailed inputs required to execute with confidence.

Request the complete Worldwide Micronized Silica Market report and the tailored executive briefing for your leadership team at our official report page. PW Consulting’s analysts are available to present the findings and work through customized implications for your business.

For detailed analysis of this topic, please visit the official page:Worldwide Micronized Silica Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com