Fresh Meat Packaging Market Size, Share, Trends, Growth Opportunities, Key Drivers and Competitive Outlook

Other |

2026-06-30 11:42:12

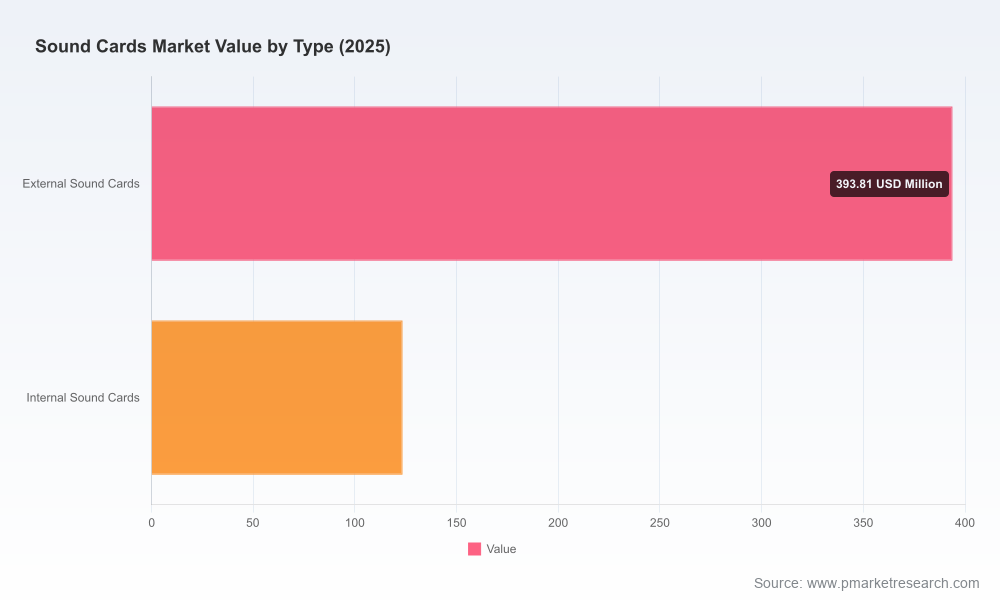

As companies calibrate product roadmaps, supplier strategies, and capital allocations for 2026, the global sound cards market presents a clear — yet nuanced — growth opportunity. PW Consulting’s latest market study, with a 2025 base year and a 2026–2032 forecast horizon, shows the market expanding at a steady compound annual growth rate of 5.88%. The market crossed the half‑billion USD threshold in 2025 and is projected to approach three‑quarters of a billion by the end of our forecast window. For decision‑makers, this trajectory signals predictable growth tempered by structural headwinds that require targeted strategic responses.

Worldwide Sound Cards Market

Consolidation of hardware and software value: Audio hardware is increasingly evaluated not only on raw analog/digital performance but on the quality of DSP, driver ecosystems, and bundled software experiences. Companies that combine premium converters with integrated software and services capture outsized margin and loyalty.

Worldwide Sound Cards Market

Multiple addressable end markets: Gaming, professional production and broadcasting, and consumer/home entertainment continue to drive distinct purchase behaviors. Each segment demands different go‑to‑market plays — from retail and e‑commerce for consumer devices to pro‑audio distribution and OEM partnerships for studio‑grade interfaces.

Worldwide Sound Cards Market

Supply‑chain and component dynamics are strategic levers: Semiconductor policies, lead‑time volatility, and the pace of DAC/ADC innovation materially influence product roadmaps, time‑to‑market and margin compression.

Demand drivers. Continued growth in high‑fidelity content creation, live streaming, and premium gaming peripherals sustains demand for external and discrete audio solutions. Professional recording and broadcast workflows are also upgrading to higher channel counts and lower latency interfaces, supporting a persistent upmarket shift.

Technology enablers. Advances in DAC/ADC performance, integrated DSPs, and high‑efficiency audio codecs enable product differentiation beyond raw SNR figures. These component innovations unlock new form factors and user experiences (e.g., compact USB DAC/amps with near‑studio performance), creating fresh product cycles.

Supply and regulatory constraints. Export controls on advanced semiconductors, tariff uncertainty, and tightened lead times for passives and discrete components have created episodic cost and timing pressures. These constraints are not uniform across suppliers and geographies — they are strategic issues that influence sourcing, inventory policy and localization decisions.

Channel evolution. The mix of direct‑to‑consumer sales, specialty pro‑audio distribution and OEM integration continues to evolve. Vendors who successfully blend digital direct channels with traditional reseller ecosystems gain faster feedback loops and higher lifetime value per customer.

The market today is composed of distinct cohorts: consumer and gaming specialists, chip and OEM platform providers, and professional audio manufacturers. Understanding their comparative advantages is essential for partnership, sourcing and M&A decisions.

Consumer and gaming players — Firms with strong brand recognition and software ecosystems remain influential. Creative Technology continues to leverage its Sound Blaster heritage, driving incremental product refreshes (including a recent USB DAC/amp launch and firmware upgrades) to defend relevance across gaming and enthusiast channels. ASUS uses motherboard expertise to extend audio capabilities into high‑value gaming SKUs. Budget OEMs likewise capture volume at lower price points through aggressive channel tactics.

Chipset and platform suppliers — Companies supplying audio codecs and controller chips underpin the majority of onboard and many aftermarket solutions. These vendors act as both enablers and gatekeepers: their product roadmaps and supply constraints cascade into downstream design choices for device makers.

Professional audio specialists — A cadre of companies focused on studio and broadcast workflows continue to command premium pricing through superior preamp technology, driver stability, low‑latency architectures and robust multichannel support. These vendors win on product reliability, technical support and integration with DAW ecosystems.

Niche and boutique suppliers — Small, specialized manufacturers deliver high‑margin audiophile and bespoke PCIe cards, cementing leadership in specific enthusiast verticals. Their agility and product depth make them attractive targets for selective partnerships or acquisitions by larger players seeking premium positioning.

Market concentration metrics indicate a moderately consolidated market: the top three players account for a material share, and the top five collectively hold a majority position. This structure yields both competitive pressure on mid‑tier vendors and strategic opportunity for consolidation. Incumbents with scale can extract distribution advantages and invest in cross‑platform software ecosystems, while buyers and private equity have room to create scale through targeted roll‑ups.

For product and R&D leaders: Prioritize investments in end‑to‑end user experience — combining high‑performance converters with best‑in‑class drivers, DSP features and software services. Roadmaps should explicitly account for alternative sourcing for critical DAC/ADC components and plan for firmware/update revenue streams.

For supply‑chain and procurement teams: Reassess inventory and dual‑sourcing strategies in response to semiconductor export controls and component lead‑time volatility. Short‑cycle buffering, strategic supplier partnerships and qualified second‑sources for key analog ICs will reduce time‑to‑market risk.

For commercial and channel executives: Differentiate GTM by bundling software and post‑purchase services for higher retention. Expand direct digital channels for premium SKUs while optimizing pro‑audio distribution for studio customers. Use data‑driven pricing experiments to identify willingness‑to‑pay across gaming, content creation and studio segments.

For corporate development and investors: Seek bolt‑on acquisitions that add complementary software, IP or distribution while filling product‑line gaps. Targets that strengthen firmware ecosystems, low‑latency drivers, or high‑end preamp capability yield disproportionate strategic value. Given the market’s moderate concentration, selective consolidation can meaningfully improve scale economics.

Our Worldwide Sound Cards Market report is structured to move leaders quickly from insight to action. Highlights include operational tools and analyses you can put to immediate use:

Actionable market sizing and scenario models — base, upside and downside forecasts designed for integration into capital planning and product investment models.

Vendor scorecards and product‑level benchmarking that compare performance claims, driver maturity, software ecosystems and channel reach (presented without publishing the granular segment tables here to protect the report’s proprietary datasets).

Supply‑chain heatmaps and risk matrices that highlight single‑source exposures, tariff and regulatory sensitivity, and component lead‑time variability.

Commercial playbooks — pricing experiments, bundling strategies and channel mixes tailored to gaming, pro audio, and home entertainment buyers.

M&A and partnership screening frameworks that identify strategic targets by capability, geography and technology adjacency, complete with integration risk checklists and valuation sensitivity analyses.

Geopolitical and regulatory risk: Continued semiconductor export controls and tariff uncertainty could raise component cost and constrain supplies for specific product classes unless mitigated by sourcing diversification or domestic qualification programs.

Technology substitution risk: Integration of high‑quality audio on mobile SoCs and expanding capabilities of onboard audio may compress certain aftermarket opportunities unless vendors innovate in features and software differentiation.

Market‑timing risk: Short windows for product refreshes and seasonal demand cycles mean that lead‑time shocks can translate directly into missed revenue opportunities.

Establish cross‑functional “audio resilience” teams that pair product, procurement and legal to model supply and regulatory scenarios.

Invest in software ecosystems and firmware monetization to protect margins and customer relationships.

Pursue selective M&A to acquire driver/IP capabilities or to consolidate niche premium positions where scale delivers distribution leverage.

Run at least two strategic supplier qualification projects for critical DAC/ADC components to reduce single‑source exposure.

Differentiate on end‑to‑end experience — low latency, robust drivers, and integrated software communities are the most defensible levers.

This brief highlights the strategic imperatives and tactical options that PW Consulting recommends for organizations engaging the sound cards market in 2026. The full report contains comprehensive regional and application breakdowns, granular product‑type splits, company profiles, and downloadable models that support deal diligence and budget planning. To access the complete dataset, segmented forecasts and our vendor scorecards with the underlying assumptions, please visit the PW Consulting research portal for the Worldwide Sound Cards Market report.

In a market growing at a mid‑single‑digit CAGR and reshaped by technological and geopolitical forces, timely, disciplined action will separate winners from laggards. PW Consulting’s analysis arms you with the frameworks and prioritized playbook to make those investments decisively in 2026.

For detailed analysis of this topic, please visit the official page:Worldwide Sound Cards Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com