Worldwide Nefopam Hydrochloride Market — Strategic Outlook for 2026: Actionable Insights from PW Consulting

As healthcare systems, formulary committees, and pharmaceutical manufacturers prepare strategic roadmaps for 2026, a clear understanding of the nefopam hydrochloride landscape has become essential. PW Consulting’s latest Worldwide Nefopam Hydrochloride Market report delivers a concise, decision‑ready intelligence package that blends rigorous forecasting, regulatory context, competitive profiling, and pragmatic go‑to‑market frameworks — all crafted to inform commercial, manufacturing and regulatory choices in the coming 18–24 months.

Worldwide Nefopam Hydrochloride Market

Why this report matters for 2026 decisions

- Timing-driven opportunity: The nefopam market is at an inflection where clinical evidence, patent activity and shifting analgesic stewardship practices intersect. Executives making 2026 product, investment or partnership decisions need forward-looking, scenario-based analysis rather than retrospective summaries.

- Risk‑aware commercialisation: With non‑opioid pain management high on payer and hospital agendas, understanding reimbursement mechanics, tender dynamics and formulary positioning is crucial to set realistic launch and pricing strategies.

- Operational planning: Raw material sourcing, capacity planning and regulatory filing strategies for APIs and finished forms require granular operational foresight to avoid supply disruptions during scale-up phases planned in 2026.

Macro view — market size and trajectory

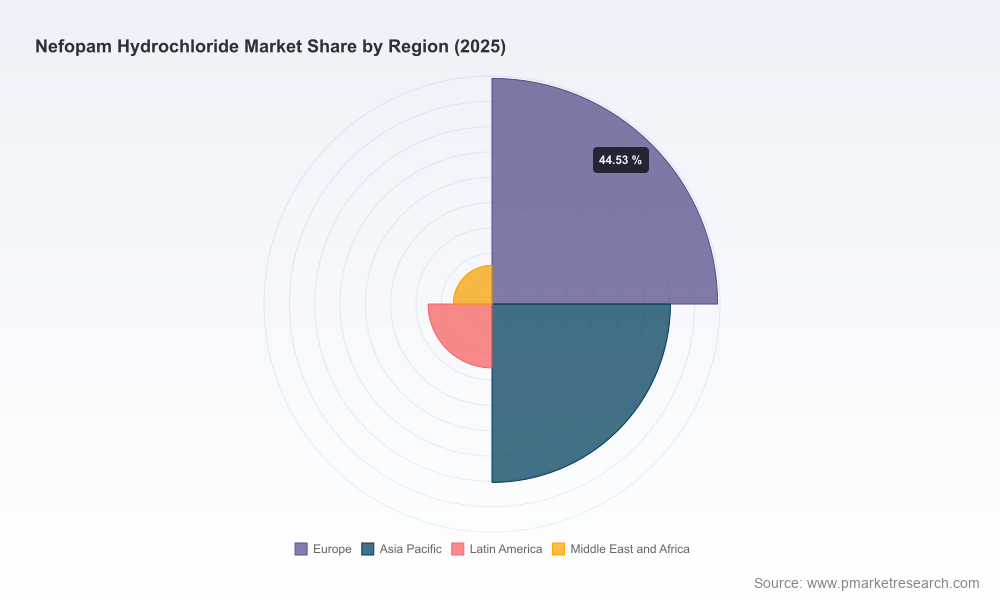

PW Consulting’s market model shows that the global nefopam hydrochloride market grew from an estimated USD 198.45 Million in 2020 to USD 257.4 Million in the 2025 base year. Looking ahead, our central forecast projects the market expanding at a compound annual growth rate (CAGR) of 5.5% through 2032, reaching approximately USD 374.44 Million by the end of the forecast horizon. This trajectory reflects a combination of steady clinical uptake in established markets, incremental formulary acceptance in selected public systems, and ongoing supplier consolidation that is shaping availability and pricing.

Worldwide Nefopam Hydrochloride Market

Key market drivers and near‑term disruptors

- Clinical evidence evolution: Recent randomized trials and publications (including a 2025 cardiac surgery analgesia study) are refining clinical positioning for nefopam, particularly as an opioid‑sparing adjunct. PW Consulting interprets aggregated clinical findings as supportive of expanded perioperative use where opioid reduction is a priority.

- Intellectual property and formulation innovation: Patent activity on optimized nefopam formulations (notably a 2025 patent grant for an optimized nefopam product intended for both acute and chronic pain) introduces differentiation opportunities for originators and may alter competitive dynamics around modified‑release or combination products.

- Regulatory and reimbursement contours: The regulatory landscape remains fragmented — nefopam formulations hold authorised status across multiple European national markets and have specific assessment histories in UK formularies. It is important to highlight that nefopam is not approved by the US FDA for marketing in the United States, a structural factor that constrains US commercial expansion without a change in approval status.

- Stewardship and cost pressure: Growing emphasis on non‑opioid pathways in enhanced recovery protocols and payer cost containment will increasingly determine adoption at hospital and system levels, heightening the importance of health‑economic evidence and local cost comparisons during procurement rounds.

Supply chain and manufacturing dynamics

Our analysis identifies a market where a handful of API and finished‑product manufacturers supply the majority of demand. The market demonstrates moderate concentration — with the top three suppliers accounting for a majority share and the top five approaching three‑quarters of market supply. That concentration, coupled with periodic API availability swings, creates both risk and opportunity: buyers face potential supply vulnerability, while suppliers with certified GMP facilities and strong regulatory dossiers stand to capture incremental share as buyers consolidate vendors to secure supply continuity.

Worldwide Nefopam Hydrochloride Market

Key supply considerations for 2026 include: qualification of secondary API sources, dual‑sourcing strategies for finished products, and proactive regulatory filings (EDMF/ASMF/CEP) to support cross‑border tender participation. Manufacturers that invest early in dossier harmonisation and localised release testing capabilities will shorten tender response times and improve commercial flexibility.

Competitive landscape — profiles and strategic takeaways

- Polpharma (Poland): Positioned as a commercial‑scale API producer with established GMP credentials and regulatory filings, Polpharma’s strength lies in supply reliability for non‑opioid analgesics. For competitors, Polpharma is a model of scaling API capabilities while managing cross‑market regulatory compliance.

- Global Calcium (India): An established exporter of nefopam API, Global Calcium benefits from competitive production economics. Firms seeking cost‑effective sourcing or co‑development partners should evaluate quality consistency and long‑term capacity commitments when engaging suppliers in this segment.

- PMC Isochem (France): With regulatory dossiers such as CEP/COS and JDMF filings, PMC Isochem offers a European‑centric supply option for firms prioritising quick access to EMA‑aligned documentation and EU tender eligibility.

- Emcure, Micro Labs, Maiden Group, CF Pharma, PRG Pharma, Taj Pharma, Guangzhou Green Cross: Collectively, these companies represent a mix of integrated pharma players and specialist API suppliers. Their strategic moves — from finished‑dosage manufacturing to focused marketing in select geographies — will determine how pricing and availability evolve across hospital and retail channels.

Recent company‑level and ecosystem developments — including a 2025 patent grant for an optimized nefopam formulation, a randomized clinical study on post‑cardiac surgery analgesia, and updated NHS formulary assessments — are already influencing procurement behaviour and formulary positioning. These developments underscore the need for dynamic competitive monitoring and scenario planning in 2026.

Strategic implications and recommended actions for 2026

- For manufacturers and API suppliers: Prioritise dossier completeness (EDMF/ASMF/CEP), validate secondary supply lines, and invest in capacity that can be flexed to meet tender windows. Early completion of regulatory paperwork in target markets shortens commercial lead times.

- For brand and generic pharmaceutical companies: Evaluate platform differentiation through formulation patents, lifecycle strategies (e.g., modified‑release or fixed‑dose combinations), and robust health economic dossiers demonstrating opioid‑sparing benefits within local care pathways.

- For hospital procurement and payers: Adopt a supplier risk‑scoring framework that incorporates regulatory filings, capacity redundancy, and real‑world analgesic outcomes. Tender specifications should require transparency on API provenance and release testing to mitigate supply‑quality risks.

- For investors and M&A teams: Target assets that combine regulatory readiness with scalable manufacturing footprints and differentiated formulations. Companies with strong EMA‑aligned documentation or exclusive patented formulations present higher strategic value, particularly for roll‑out in European and select APAC markets.

What PW Consulting’s report delivers — practical, action‑oriented contents

The report is built for decision makers who need executable insight, not just descriptive data. Highlights include:

- Robust market model: Historical (2020–2025) and forecast (2026–2032) financials with scenario‑based sensitivity analyses anchored to a 5.5% central CAGR.

- Regulatory and reimbursement map: Country‑level regulatory status summaries, formulary case studies, and payer positioning frameworks to support market entry and pricing strategies.

- Supply chain due diligence toolkit: Supplier selection matrix, recommended audit checklists, and contingency sourcing pathways to mitigate API disruption risks.

- Competitive intelligence: Vendor profiles, capability assessments, and strategic positioning advice for top industry players — focused on commercial and manufacturing tactics rather than raw market share tables.

- Commercial playbooks: Tender tactics, hospital engagement templates, and evidence‑generation roadmaps to accelerate uptake in perioperative and chronic pain settings.

- Appendices and data packs: Methodology notes, data sources, interview transcripts with key opinion leaders, and an anonymised transaction comparable set to support valuation work.

What we intentionally do not publish in this communique

In line with our “trailer” principle, this press synopsis demonstrates analytical depth while intentionally withholding the complete granular segmentation tables and proprietary price matrices. Readers requiring the comprehensive regional, product‑form and application splits, the full company share tables and the downloadable datasets should consult the full report via the PW Consulting portal.

How clients are using the report in 2026 planning

- Manufacturers are aligning capital expenditure timelines to the forecasted demand inflection points to avoid either idle capacity or supply shortfalls.

- Commercial teams are building formulary dossiers targeted to hospital systems’ opioid‑sparing initiatives using the report’s template health economic models.

- M&A and corporate development groups are using our valuation scenarios to screen acquisition targets with CEP/JDMF-ready dossiers and IP positions that support premium pricing in selected markets.

Next steps and how to access the full intelligence

For teams preparing 2026 business plans, the primary value is in the full dataset, the supplier risk matrices, and the therapeutic‑area commercial playbooks included in the complete report. Access to the comprehensive segmentation tables, transaction comparables and downloadable model files is available through the PW Consulting report page. This is where we provide the actionable detail that supports contract negotiations, tender responses, regulatory filing schedules and investment approvals.

PW Consulting stands ready to support bespoke strategy workshops, supplier due‑diligence engagements, and rapid‑turn scenario modelling to help clients convert the report’s insights into executable plans for 2026. Contact our industry team via the PW Consulting portal for report access and advisory services.

For detailed analysis of this topic, please visit the official page:Worldwide Nefopam Hydrochloride Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com