Swedish Massage Tukwila WA | Relax at Blue Lotus Spa

Other |

2026-07-03 10:20:38

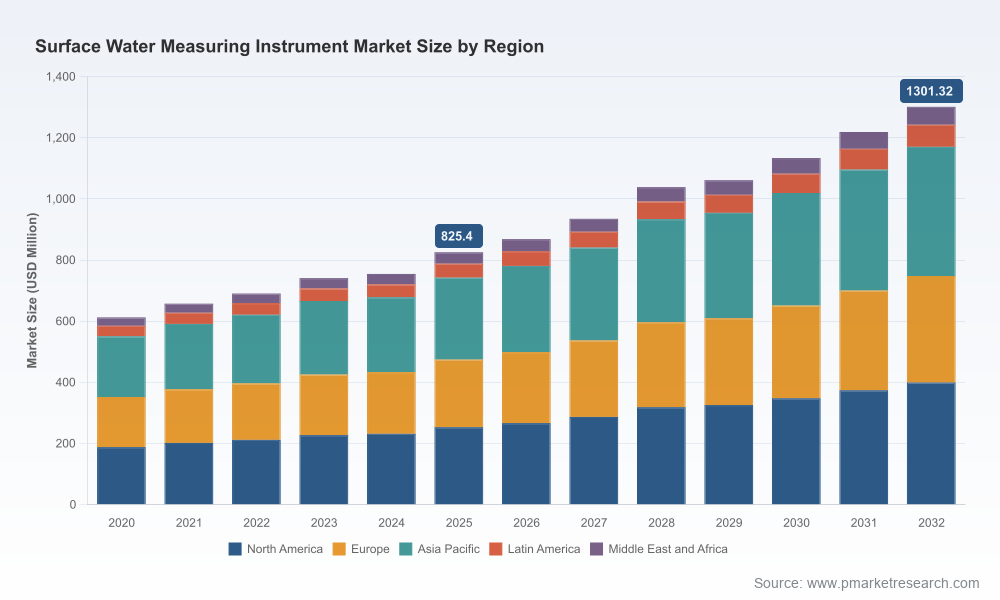

PW Consulting’s latest market research on the Worldwide Surface Water Measuring Instrument Market provides a timely strategic compass for companies planning capital allocation, product development, and go-to-market moves in 2026. Built on a 2020–2025 historical baseline and a 2026–2032 forecast horizon, the study quantifies a resilient market that expanded from a multi-hundred million-dollar base in 2020 to an estimated USD 825.4 Million in 2025, and that is projected to grow at a compound annual growth rate (CAGR) of 6.72% through the forecast window. By 2032 the market is modelled to reach roughly USD 1.30 billion (USD Million unit convention throughout).

Worldwide Surface Water Measuring Instrument Market

Actionable Sizing and Momentum: The report translates macro momentum into operationally relevant metrics — not just headline CAGR, but scenario-driven topline paths under differing technology adoption and procurement cycles. That allows executives to test capital plans against realistic adoption curves for remote sensing, telemetry, and integrated monitoring kits in surface water contexts.

Worldwide Surface Water Measuring Instrument Market

Technology-Weighted Forecasts: We layer adoption assumptions for non-contact radar (including recent advances in FMCW radar), submersible probes, flow meters and integrated telemetry stacks into the forecasting engine. The result is a forecast that differentiates near-term retrofit cycles from longer-term replacements driven by regulatory and data-quality demands.

Worldwide Surface Water Measuring Instrument Market

Decision-Ready Benchmarks: For procurement, R&D and M&A teams, the study delivers vendor benchmarking, product positioning matrices and an assessment of total cost of ownership (TCO) drivers — from sensor material choices (titanium vs. 316L stainless housings) to remote calibration needs — enabling pragmatic trade-offs when scaling deployments in saline, tidal or remote freshwater environments.

Practical market model with scenario toggles — baseline, accelerated IoT adoption and conservative CAPEX cycles — enabling rapid sensitivity testing for FY26 budgeting.

Go-to-market playbooks for three typical buyer archetypes: agencies (e.g., flood and watershed management), utilities/agriculture, and industrial customers requiring effluent monitoring. Each playbook maps procurement cycles, specification templates and service-level expectations that materially shorten sales cycles.

Vendor selection and procurement templates — requirement checklists, test-and-acceptance criteria, and supplier evaluation scorecards — designed to reduce deployment risk and align procurement teams on long-term data integrity and maintenance burdens.

Technology and product roadmaps — comparative analyses of sensing technologies (radar FMCW, pressure transducers, electromagnetic and propeller flow meters, multiparameter probes), telemetry options, and edge vs. cloud processing strategies.

Supply-chain and component analysis — including critical raw-material considerations for probe housings and electronics, and the implications of sourcing choices for lifecycle economics in harsh or saline environments.

Financial templates and ROI frameworks — payback calculators and fleet-sizing models that link device-level costs and reliability assumptions to service revenue opportunities and capex allocation decisions.

Risk registers and mitigations — regulatory, environmental, and operational risks (including field calibration frequency, vandalism and extreme-event survivability) with prioritized mitigation actions.

The competitive map in surface water instrumentation is a mix of established instrumentation OEMs, specialized probe manufacturers, and solutions providers increasingly combining hardware with data services. The market’s structure rewards domain expertise in hydrology and proven field reliability while opening win windows to companies that can deliver turnkey data and analytics for real-time decision-making.

Instrument platform leaders: Companies with deep expertise in rugged, unattended monitoring systems remain market anchors. Their strengths lie in durable dataloggers, proven sensor suites and recognized compliance with customer accuracy expectations — attributes that public agencies and long-term monitoring programs value highly.

Flow and sensor specialists: Suppliers focused on electromagnetic, propeller and submersible sensing continue to win on technical fit for specific use-cases (e.g., shallow channels, high-sediment rivers, irrigation headworks). These firms are well positioned to capture retrofit and replacement spending where sensor-specific performance is the deciding factor.

Integrated-systems players: A new wave of offerings bundles high-resolution radar level sensing, IoT edge devices and cloud-based alerting into flood monitoring appliances. These systems simplify procurement but require robust integration, lifecycle support and clear SLAs.

Notable market moves in 2025 illustrate these dynamics. One provider announced a next-generation 80 GHz FMCW radar level sensor and an integrated flood monitoring appliance, underlining the accelerating adoption of high-frequency radar for low-maintenance, high-accuracy level measurement in riverine and tidal contexts. Another strategic acquisition expanded a specialized probe maker’s capabilities by adding complementary water quality probes and tying them into existing level and datalogger portfolios — a clear signal that consolidation to broaden end-to-end product suites remains an active play.

Taken together, these developments emphasize two imperatives for 2026: (1) investments in system-level integration that reduce buyer friction and (2) targeted M&A to close product gaps quickly.

Accuracy and standardization: Regulatory guidance that influences measurement practice — such as standards for non-contact radar accuracy in surface water applications — is steering sensor specifications. Vendors that align product R&D to meet these guidance documents accelerate procurement approvals in agency markets.

IoT and analytics: Continued adoption of IoT-enabled radar and telemetry units is turning sensors into data platforms. Customers increasingly value end-to-end solutions that combine real-time alerts, cloud analytics and APIs for integration into broader hydrometeorological systems.

Materials and durability: Component choices (e.g., titanium vs. 316L stainless steel housings) are important differentiators in saline or highly corrosive environments, affecting warranty, mean-time-between-failures and lifecycle cost.

Prioritize integration-first development: Allocate R&D budgets to make sensors “deployment-ready” — pre-configured telemetry, automated health-checks, and cloud onboarding — so procurement teams face lower operational friction. This increases win rates in agency and utility tenders.

Adopt modular product architectures: Design platforms so customers can upgrade sensing modules independently from telemetry and analytics subscriptions. This reduces replacement cycles and creates recurring revenue pathways.

Pursue tuck-in acquisitions that add complementary sensing or software capabilities rather than broad horizontal expansion. Faster time-to-market for integrated offerings beats incremental organic development in this market.

Differentiate on service economics: Build transparent TCO calculators and field support contracts that lower perceived long-term risk for buyers. For many customers, lifecycle predictability outweighs small upfront price advantages.

Engage with standards-setters and agencies early: Participation in working groups and collaborative pilots speeds procurement approvals and positions vendors as preferred suppliers in public-sector programs.

Focus on data monetization pilots: Where privacy and procurement rules permit, package anonymized, value-added data services (e.g., flood-risk indices, long-term trend analytics) as subscription offerings to diversify revenue.

Supply-chain volatility: Component lead times and raw-material pricing can compress margins. Mitigation: dual-sourcing strategies for critical housings and early component hedging.

Standards divergence: Emergent sensor standards could create retrofit waves that accelerate obsolescence for older platforms. Mitigation: invest in backward-compatible gateways and firmware update capabilities.

Competition on price: As integrated offerings commoditize, firms focused solely on hardware risk margin pressure. Mitigation: emphasize services, analytics and performance guarantees that are harder to replicate.

Decision-makers should treat the report as both a market map and an operational playbook. Use it to stress-test 2026 budgets, prioritize product and M&A investments, and calibrate commercial models (capex sale vs. device-plus-subscription). For procurement teams, the vendor scorecards and test templates can be plugged directly into RFP processes to shorten evaluation timelines. For R&D leaders, the technology assessment spotlights where to accelerate workstreams to meet imminent regulatory and customer expectations.

PW Consulting’s research reveals a market that is mature in its core reliability expectations yet still in motion at the edges — driven by radar advancements, IoT integration, and demand for complete data solutions. In 2026, winning will be a function of speed to integration, clarity on lifecycle economics, and the ability to demonstrate reliable, standards-aligned performance in the field.

To access the full dataset, provider scorecards, region-and-application breakouts, and the detailed financial model that underpins our scenarios, visit the official report page. The public summary establishes the strategic outline; the full report delivers the numerical granularity and executable templates that procurement, product and corporate development teams need to act in 2026.

For detailed analysis of this topic, please visit the official page:Worldwide Surface Water Measuring Instrument Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com