Worldwide GMP Protein (E. coli) Contract Manufacturing Market: Strategic Imperatives for 2026

Executive summary

As biopharma companies shift pipelines toward next-generation protein therapeutics, contract manufacturing for GMP-grade proteins produced in Escherichia coli is moving from a boutique service to an essential industrial capability. PW Consulting’s latest market study—using 2025 as the base year and projecting through 2032—shows a market that expands from a 2025 baseline of USD 1,585.4 Million to an anticipated USD 3,396.8 Million by 2032, reflecting a compound annual growth rate (CAGR) of 11.45% over the forecast period. The pace and profile of that growth have profound implications for supply security, partner selection, and capital allocation in 2026.

Worldwide GMP Protein (E. coli) Contract Manufacturing Market

This commentary highlights the strategic value of the report for leadership teams planning manufacturing footprints, M&A activity, or outsourcing strategies next year. In keeping with our “trailer” approach, we surface the analytical rigor and decision tools contained in the full report while deliberately withholding certain segmented datapoints to encourage direct access to the source report for program-level decisions.

Worldwide GMP Protein (E. coli) Contract Manufacturing Market

What this report delivers — practical, decision-ready content

- Forward-looking market sizing and validated CAGR projections for 2026–2032, anchored to a detailed 2020–2025 historical analysis and reconciled across multiple commercial scenarios.

- Actionable supplier benchmarking that goes beyond marketing claims: facility certifications, platform capabilities (incl. secretion and refolding technologies), quality performance indicators, and preferred regulatory pathways for E. coli-derived products.

- Operational toolkits: total cost of goods (TCO) models for microbial protein production, sensitivity analyses on key cost drivers (raw materials, labor, QC analytics), and capacity-utilization scenarios for clinical versus commercial programs.

- Regulatory and analytical playbooks: matrixed guidance on host cell protein (HCP) and host cell DNA monitoring, recommended orthogonal assay strategies, and stepwise risk-reduction workflows to meet FDA, EMA, and ICH expectations.

- Negotiation-ready commercial frameworks: sample contractual clauses for tech transfer, capacity reservation, change control, and liability for product-related impurities.

- Decision-support outputs: heatmaps for outsourcing risk (supply, regulatory, quality), go/no-go thresholds for building vs. buying, and M&A scorecards for evaluating CDMO targets.

Key market dynamics shaping 2026 choices

Three structural forces are converging in the E. coli GMP protein CDMO market:

Worldwide GMP Protein (E. coli) Contract Manufacturing Market

- Accelerating demand from therapeutic protein pipelines and ancillary needs (e.g., plasmid DNA, research-grade proteins) is driving capacity uptake and premiumization of service tiers.

- Regulatory and analytical expectations have risen: recent FDA guidance emphasizes the characterization of host cell proteins (HCP), and ICH/EMA frameworks continue to formalize residual impurity monitoring—requiring platform- or process-specific HCP assays and orthogonal analytics for clinical and commercial batches.

- Technology differentiation and supply resilience matter. Proprietary secretion systems, advanced inclusion-body refolding technologies, and ultra-low endotoxin processes are becoming non-price decision drivers for partners and acquirers alike.

These dynamics are already visible in industry movement: strategic partnerships to secure high-efficiency pDNA production that leverages E. coli platforms, service-expansion announcements from regional CDMOs, and recent GMP certifications that broaden capacity for antibody fragments and other protein classes. Collectively, these signals point to a market increasingly defined by specialization, certification, and regulatory readiness.

Competitive landscape — consolidation vs. specialization

The market is neither hyper-fragmented nor locked into an oligopoly. Our concentration metrics indicate a mid-level consolidation: the top three suppliers account for a meaningful share of the market, and the top five approximate a majority block—an environment conducive to both scale-focused global CDMOs and specialized regional providers. This mixed structure supports multiple strategic postures depending on an organization’s risk tolerance, product complexity, and speed-to-clinic requirements.

Representative providers profiled in the report span global incumbents and specialized niche players. Among them:

- Large, integrated CDMOs with global footprints and microbial toolboxes that include E. coli systems, able to support end-to-end programs from process development to commercial supply.

- Regional specialists with deep expertise in microbial expression and regulatory-compliant manufacturing for complex proteins and antibody fragments.

- Technology-focused firms offering unique competencies—refolding methods for inclusion bodies, secretion platforms, or ultra-low endotoxin processes—that materially reduce downstream risk for certain product classes.

For executives evaluating partner sets, the practical takeaway is simple: prioritize fit-to-product (e.g., inclusion-body prone sequences need a partner with proven refolding throughput), regulatory track record in target markets, and demonstrable analytics competency for HCP/HCD control. The full report contains a supplier scorecard template and facility-level capability matrices to accelerate that assessment.

Regulatory and analytical imperatives

Regulatory agencies now expect a higher standard of impurity characterization for E. coli-derived biologics. FDA guidance emphasizes tailored HCP assays per USP <1132> and process- or platform-specific validation; ICH and EMA guidelines require routine monitoring using sensitive immunoassays or orthogonal methods. In practice, this raises three operational requirements for 2026:

- Early investment in analytics: developers must budget for platform-specific HCP assays, host cell DNA clearance studies, and orthogonal validation to de-risk pivotal batches.

- QC and talent upskilling: robust GMP programs demand experienced QC staff and ongoing training to meet international expectations across multiple authorities.

- Contractual clarity on release criteria: responsibility for impurity-related investigations must be explicit in tech-transfer and supply agreements to avoid supply interruptions or regulatory findings.

Strategic recommendations for 2026 decision-makers

Based on cross-industry benchmarking and scenario modeling in the report, PW Consulting recommends that biopharma leaders adopt a multi-dimensional supply strategy next year:

- Hedge capacity with a tiered partner ecosystem: combine a primary global CDMO for scale with specialized regional providers for product classes that require unique technologies (e.g., inclusion-body refolding, secretion systems).

- Mandate pre-transfer analytics packages: require platform-specific HCP and DNA assays, and include contingency testing plans in contracts to accelerate regulatory filings.

- Design procurement around TCO, not headline price: include QC staffing, assay development, regulatory support, and change-control timelines in cost comparisons.

- Preserve optionality through modular capacity investments: where in-house manufacturing is considered, favor modular clean-room designs and single-use lines that shorten ramp-up time and support multiple product types.

- Use M&A selectively to access capability gaps: target acquisitions that bring differentiated technologies (e.g., novel refolding, secretion, or endotoxin-reduction platforms) rather than generic capacity.

- Stress-test supply agreements for regulatory friction: include clear timelines and responsibilities for deviations, recall coordination, and inspections to limit business interruption risk.

How to use this research in the boardroom

Boards and executive committees will find the report valuable as a strategic briefing and an operational playbook. Recommended uses include:

- Scenario planning: apply the report’s high/medium/low demand scenarios to test capital allocation for 18–36 month capacity plans.

- Vendor selection: adapt the report’s supplier scorecards and facility benchmark to compress due diligence timelines for critical suppliers.

- Regulatory readiness: adopt the analytical playbook to set budgets and timelines for assay development and validation so pivotal batches are not delayed.

- M&A screening: use the M&A scorecards to prioritize targets that close critical capability gaps rather than only expand capacity.

Closing note and next steps

The E. coli GMP protein contract manufacturing market is entering a more industrialized phase—growth is robust and predictable at the macro level, but competitive advantage will be earned through technology differentiation, regulatory excellence, and contractual agility. PW Consulting’s full market study provides the detailed sub-segment intelligence, facility-level maps, and contract-play decks that procurement, development, and strategy teams need to make confident 2026 decisions.

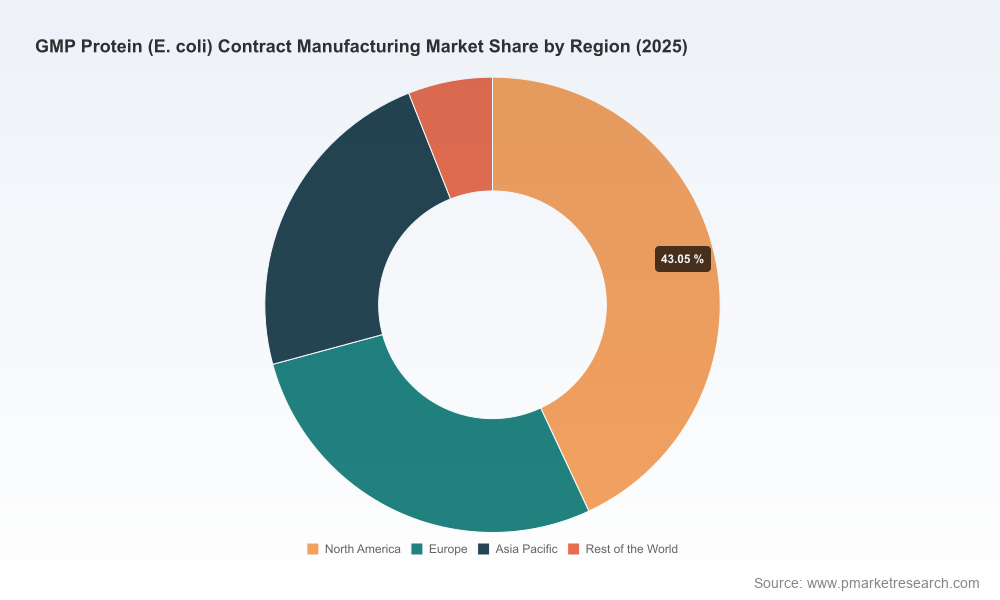

To preserve strategic leverage for our clients, this release offers a forward-looking synthesis of the market’s scale and drivers while intentionally withholding granular regional and application splits. Stakeholders seeking the complete dataset—facility-by-facility capability matrices, detailed segmentation, and downloadable commercial modeling tools—are invited to access the full report on PW Consulting’s report page or contact our advisory team for a guided briefing.

For detailed analysis of this topic, please visit the official page:Worldwide GMP Protein (E. coli) Contract Manufacturing Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com