Worldwide Oxcarbazepine Market: Strategic Imperatives for 2026 — PW Consulting Industry Brief

Executive summary

The Worldwide Oxcarbazepine Market is entering 2026 from a position of steady, measureable growth and operational complexity. Our latest market model—anchored on a 2025 base year—shows the global Oxcarbazepine market at USD 310.0 Million in 2025, rising to a projected USD 325.98 Million in 2026 and reaching approximately USD 385.17 Million by 2032, reflecting a compounded annual growth rate (CAGR) of 3.15% over the 2026–2032 forecast window. Historical figures between 2020 and 2025 evidence modest volatility and resilience, moving from USD 265.47 Million in 2020 to USD 310.0 Million in 2025 amid episodic supply disruptions and shifting payer dynamics.

Worldwide Oxcarbazepine Market

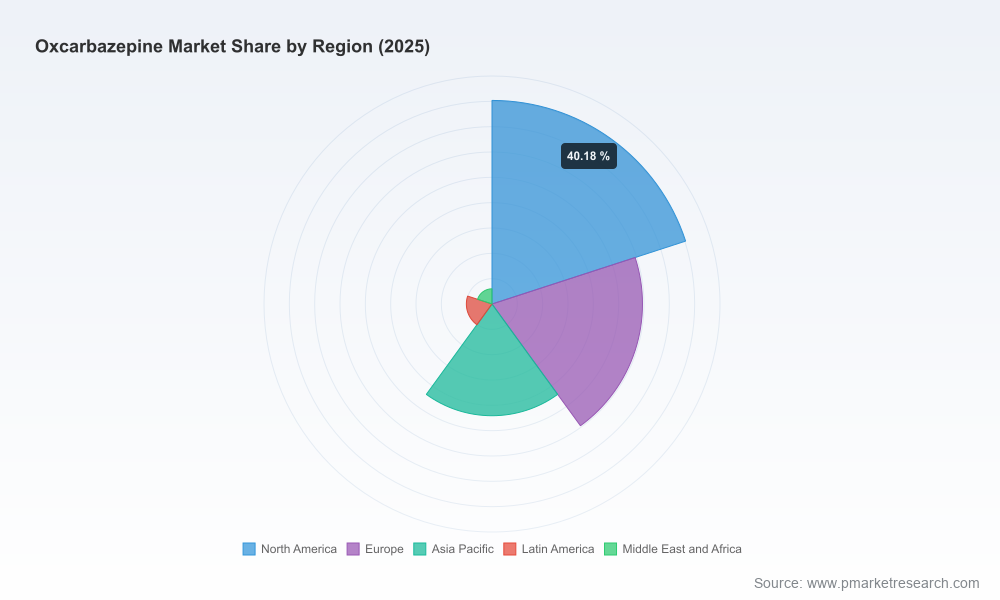

For senior executives, portfolio managers, manufacturing leaders and strategic investors making decisions in 2026, this report is designed as a practical decision-support tool: it distills macro momentum, uncovers pockets of commercial and operational risk, and maps clear pathways to protect and grow Oxcarbazepine franchises in an increasingly concentrated generics ecosystem (CR3 ~38.5%; CR5 ~52.2%).

Worldwide Oxcarbazepine Market

Why this matters for 2026 decision-making

- Predictable but constrained growth: A mid-single-digit CAGR signals a market where topline expansion will come from share gains, formulation diversification and selective geographic plays rather than from broad demand expansion. Organizations must therefore prioritize efficiency, product differentiation and channel strategy.

- Fragmented competitive field with consolidation potential: Concentration metrics indicate that a meaningful portion of the market is controlled by a handful of global and regional players. This leaves space for bolt-on acquisitions, strategic alliances and scale-driven cost optimization.

- Supply-side fragility: The market’s dependence on a concentrated API supply chain—predominantly sourced from India and China—and episodic manufacturing disruptions means 2026 is a critical year to execute supply resilience plans and dual-sourcing strategies.

- Regulatory and reimbursement leverage: With Oxcarbazepine recognized on the WHO Model List of Essential Medicines and covered under major payer schemes (e.g., Medicare Part D), pricing and access tactics will materially influence uptake and margins in 2026.

What the PW Consulting report delivers — actionable, operational intelligence

Beyond headline forecasts, the study provides a suite of hands-on tools and frameworks tailored to support 2026 execution cycles:

Worldwide Oxcarbazepine Market

- Integrated forecasting model: A dynamic forecast (2026–2032) with sensitivity levers for pricing, tender wins, supply disruptions and market-entry timing. The model is provided in an editable spreadsheet to enable scenario-run by corporate finance and commercial teams.

- Demand-supply matrix: A granular conceptual map that aligns manufacturing capacity, API availability and logistics risk with demand drivers—designed to prioritize capital allocation and contingency planning.

- Regulatory risk tracker: A living dashboard that flags key regulatory events, US ANDA and EMA submissions to watch, and implications for exclusivity windows and competitive entry timing.

- Launch and commercialization playbooks: Tactical checklists covering timing of launches, channel segmentation, payer contracting, sample strategy and value communication for both tablets and oral suspension formulations.

- Supply-chain resilience framework: Step-by-step guidance on supplier qualification, API dual-sourcing, inventory policy adjustments and nearshoring options to mitigate the manufacturing shocks experienced in 2022–2023.

- Deal origination templates: A structured M&A and licensing evaluation toolkit—valuation yardsticks, synergy mapping and quick diligence checklists tuned to Oxcarbazepine assets.

Competitive landscape — what the leading manufacturers signal for 2026

The competitive set comprises large global generics teams and regionally strong Indian and European manufacturers. Key players include established multinational generics groups and major Indian exporters. Each type of competitor brings distinct strategic advantages:

- Global generics leaders (e.g., Teva, Sandoz, Viatris): Scale advantages in manufacturing, established distribution in regulated markets and broad product portfolios enable rapid route-to-market for incremental demand. These firms are best positioned to execute large-scale contract wins and to absorb pricing pressure through volume economics.

- Large specialty generics and Indian-origin manufacturers (e.g., Sun Pharma, Dr. Reddy’s, Lupin, Aurobindo, Zydus, Cipla, MSN, Alembic, Apotex, Apotex-equivalent regionals): Strong API sourcing relationships, competitive cost structures and regulatory familiarity with ANDA/EMA pathways provide opportunities for targeted geographic expansion and tender-driven growth. Several of these players have pursued filing and product launches to fill gaps created by prior shortages.

- Smaller, niche manufacturers and new entrants: Firms that pursue differentiated formulations (e.g., extended-release or suspension formats) or focused channels (paediatric formulations, hospital tenders) can win sustainable pockets of business even in a mature market.

Notable recent developments inform competitive positioning: the final approval of extended‑release formulations by certain manufacturers in 2023, resolution of intermittent shortages (notably of the 300 mg tablet) in 2023, and product launches such as oral suspension introductions—all of which highlight both supply-side vulnerability and the commercial value of formulation breadth.

Regulatory and market dynamics to watch in 2026

- Post-patent generic maturity: With originator patents expired well over a decade ago, competitive dynamics are governed by cost, scale, and regulatory approvals rather than IP protection. This changes the calculus for premium pricing and requires firms to deploy service- or formulation-based differentiation.

- Payer and procurement pressure: Coverage under major public programs and frequent tendering in some markets shift the battle to net pricing and supply reliability. Effective 2026 strategies will combine flexible contracting with assurances of continuity.

- API concentration risk: The reliance on a relatively small set of active ingredient suppliers means any material disruption can create near-term scarcity and price spikes—events that favor incumbents with deep upstream relationships or diversified supplier portfolios.

- Clinical and off-label use dynamics: While epilepsy remains the core application, alternative neurological indications and paediatric formulations represent modest but strategic extension opportunities for firms seeking to differentiate.

Strategic imperatives and 90–180 day plays for 2026

- Lock in supply continuity: Activate dual-sourcing plans, convert critical suppliers to commercial agreements with robust service-level commitments, and stress-test contract manufacturing partners by Q2 2026.

- Optimize portfolio mix: Reassess SKU rationalization versus formulation expansion (e.g., extended-release, suspension) using the report’s elasticities and margin simulations to prioritize SKUs that maximize return on invested capital.

- Prepare for opportunistic consolidation: Use the provided M&A playbook to identify tuck-in targets that deliver immediate manufacturing scale or new regulated-market registrations.

- Secure payer and tender pathways: Build tender and payer submission templates now to be ready for rolling RFPs and formulary reviews, leveraging evidence packages and supply warranties to win preferred status.

- Invest in commercial differentiation: For markets where price competition is intense, move to service-led offerings—patient support, adherence programs, and bundled hospital support—that create value beyond unit price.

How PW Consulting supports your 2026 execution

PW Consulting couples deep market analytics with hands-on implementation capabilities. Clients receive the full forecast model, an executive briefing, a tailored workshop to translate findings into an operational plan, and optional retained advisory support to execute priority plays—whether that is supplier diversification, commercial negotiations, or M&A diligence. The full report includes the granular regional and application splits, scenario outputs, and downloadable models that we intentionally do not publish in this preview.

Conclusion — actionable clarity for a complex market

As Oxcarbazepine moves through a steady-growth phase, 2026 will separate organizations that execute disciplined, risk-aware plays from those exposed to cost and supply shocks. Our report is crafted to inform board-level strategy, commercial planning cycles and operational investments—delivering the tools needed to convert a modest market growth rate into sustainable value creation.

To access the full dataset, detailed regional and application breakdowns, and the interactive forecast model, please visit our report landing page or contact PW Consulting for a tailored briefing. The proprietary elements behind our forecast are intentionally reserved for report subscribers, enabling you to act with confidential, validated intelligence in 2026 and beyond.

For detailed analysis of this topic, please visit the official page:Worldwide Oxcarbazepine Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com