Turn Every Call Into Revenue with OmniCaaS's AI-Powered VoIP Solution

Security |

2026-06-25 06:04:34

PW Consulting’s latest market study, "Worldwide Classified Circuit Breaker Market" (base year 2025), delivers a focused, forward‑looking playbook for executives and investors planning capital allocation and go‑to‑market moves in 2026. The market has re‑centered after a volatile early‑decade period and is now on a sustained growth path: our model projects the market at approximately USD 578.6 million in 2026 and expanding at a 6.0% CAGR through the 2026–2032 forecast window, approaching roughly USD 812 million by 2032. This briefing synthesizes the report’s strategic value without exposing the proprietary segmentation matrices reserved for subscribers.

Worldwide Classified Circuit Breaker Market

Two factors make 2026 a pivotal year for operators across the classified circuit breaker value chain. First, macro tailwinds — grid modernization, accelerating renewables integration, and the shift to digitally enabled distribution components — are converging with renewed end‑market investment cycles in residential retrofit and commercial upgrade work. Second, supply‑side dynamics — from raw material cost pressures (copper, steel, engineered polymers) to evolving interchangeability rules and UL‑classification pathways — are altering margins, sourcing risk, and competitive advantage.

Worldwide Classified Circuit Breaker Market

For C‑suite leaders and business unit heads, the report transforms these trends into actionable vantage points: priority markets for incremental investment, product and certification roadmaps, supplier consolidation opportunities, and acquisition targets that deliver immediate market access or technology differentiation.

Worldwide Classified Circuit Breaker Market

The classified breaker segment shows meaningful concentration: the top three players control a majority share, while the top five approach a high‑sixty percent share of the market. This structure produces a dual landscape: established multinational incumbents that compete on breadth, certification footprints and channel relationships, and specialist OEMs and regional players that compete on price, form‑factor compatibility and rapid local assembly.

Key strategic implications:

Our competitive benchmarking in the report profiles global brands and regional specialists. Highlights from our qualitative analysis:

Collectively, the market is evolving into a bifurcated structure: scale incumbents defending certification and channel moats; nimble regional players exploiting cost and proximity; and technology challengers embedding digital features into breakers to capture services value.

UL classification remains a decisive enabler of third‑party replacements and a hard requirement for interoperability in many markets. Our field work and interviews show that the ability to demonstrate safe mechanical and electrical interchangeability with major loadcenter brands — and to maintain those compatibility lists — is a recurring purchase criterion for both distributors and installers.

From a procurement standpoint, firms must balance the certification lead time and testing costs against the long‑term channel access that UL classification delivers. For product strategy teams, this converts into a prioritization matrix: which loadcenter families to certify for, which protection functions to bundle, and which geographies warrant the upfront testing investment.

Manufacturing of circuit breakers depends on a narrow set of critical materials — copper conductors, structural steels, and advanced polymers for insulating housings and arc extinguishing components. Volatility in these inputs directly compresses margin or forces price adjustments at the channel level. The report includes a supplier risk heat map and suggested sourcing strategies that materially reduce exposure via hedging, long‑term supplier agreements and near‑shoring options.

Digitalization of breakers — remote monitoring, trip analytics and integration with building energy management systems — is shifting some value from discrete hardware sales to recurring services and firmware ecosystems. Our technology roadmaps demonstrate where digital features deliver the most commercial leverage (e.g., managed retrofit programs, commercial building energy optimization) and which certification pathways are required to bring those products to market.

Trade show intelligence from 2026 highlights this transition: several vendors showcased digitally enabled prototypes and announced regional production initiatives, indicating that product roadmaps are converging on remotely manageable breakers and smarter retrofit solutions.

PW Consulting’s full report is purpose‑built for executives who need to act in 2026. Key deliverables include:

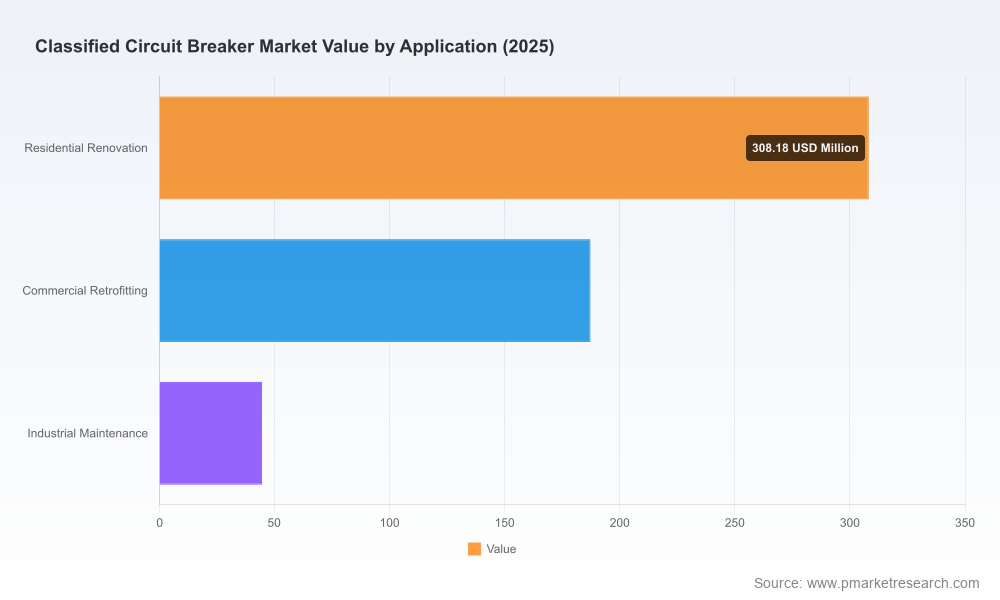

Note: detailed regional and application‑level splits, price decks and granular company revenue estimates are intentionally omitted from this briefing and remain available only in the full subscription version of the report.

Based on our findings, PW Consulting recommends the following priority actions for 2026:

Our report is constructed to be directly actionable. Clients receive bespoke briefings that map the forecast and competitor intelligence to their P&L and operational KPIs. For organizations evaluating entry, expansion or consolidation strategies in 2026, we provide a short, high‑impact engagement option that aligns the market forecast and scenario outputs with transaction diligence or product launch roadmaps.

To access the detailed regional, application and company revenue breakdowns that underpin these strategic recommendations, please consult the full "Worldwide Classified Circuit Breaker Market" report. That dataset includes the granular segmentation, price decks and the three scenario matrices required to finalize capital allocation and M&A decisions.

The classified circuit breaker market presents a classic 2026 strategic paradox: steady overall growth and meaningful innovation opportunities, set against tightening certification and material cost constraints. Leaders who combine disciplined certification strategies, targeted supply‑chain hedging and rapid digital product iteration will create durable differentiation. PW Consulting’s research equips decision‑makers with the quantified scenarios and executable playbooks to convert that potential into measurable commercial outcomes.

For detailed analysis of this topic, please visit the official page:Worldwide Classified Circuit Breaker Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com