Military Power Solutions Market Opportunities in Mobile Energy Platforms

Other |

2026-03-13 12:12:15

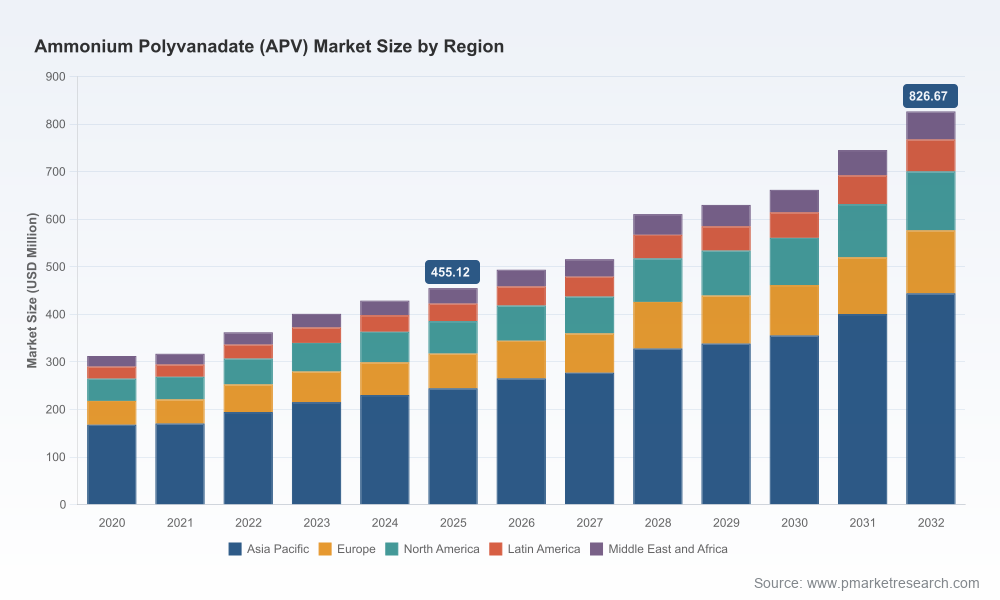

As strategic advisors to resource-backed manufacturers, advanced materials buyers, and downstream industrial users, PW Consulting presents a concise but forward-looking lens on the ammonium polyvanadate (APV) market as companies prepare decisions for 2026. Our new market study establishes a clear macro context: the APV market stood at USD 455.12 Million in the report base year (2025) and is projected to grow to USD 826.67 Million by 2032, reflecting a compound annual growth rate (CAGR) of 8.9% across the 2026–2032 forecast period. This growth trajectory is underpinned by converging demand drivers, raw material dynamics, and regulatory developments that will reshuffle competitive advantage in the near term.

Worldwide Ammonium Polyvanadate (APV) Market

Timing of capital allocation: The mid‑decade inflection in APV demand and pricing dynamics requires firms to re-examine near‑term CapEx schedules for purification and downstream vanadium conversion units.

Worldwide Ammonium Polyvanadate (APV) Market

Supply-chain security: With primary vanadium production concentrated in a limited set of producing countries and the raw material subject to geopolitics, 2026 is a critical year to enact hedging, supplier diversification, and traceability measures.

Worldwide Ammonium Polyvanadate (APV) Market

Product and process differentiation: Demand themes — from metallurgical alloys to battery chemistries and catalytic applications — are raising the bar on purity, particle morphology, and consistency; firms that can operationalize tight quality control will capture out-sized margins.

Three structural dynamics define the 2026 strategic landscape. First, supply-side concentration in primary vanadium production creates persistent raw‑material asymmetries: global contained vanadium production was approximately 100,000 metric tons in 2023, with China alone accounting for the dominant share of output. Second, geopolitics is actively reconfiguring access and risk — production from some regions declined in 2023 due to international sanctions — elevating country risk premiums and logistics complexity. Third, policy recognition of vanadium as a strategic mineral (for example, inclusion on the European Union's Critical Raw Materials list) accelerates public-sector interest in domestic sourcing, recycling programs, and strategic inventories.

These structural factors combine with demand-side evolution. Traditional metallurgical demand for ferrovanadium remains a backbone use case, but growth pockets — notably advanced catalysts and battery systems such as vanadium redox flow batteries (VRFBs) — are amplifying requirements for higher-purity intermediates and predictable long-term supply contracts. The net effect for 2026: price volatility and premiumization of quality segments by specification.

Our report is engineered to inform boardroom choices and investment theses in 2026. It delivers:

Data-backed market sizing and trend analysis — comprehensive historical review (2020–2025) and robust forecasting (2026–2032) built on transaction-level intelligence, producer capacity audits, and demand-model triangulation.

Supply-chain heatmaps — supplier concentration, feedstock dependencies, logistics chokepoints, and scenario-based disruption modeling to stress-test procurement strategies.

Price and cost modeling — dynamic cost curves and price sensitivity analyses that isolate feedstock, energy, and conversion cost drivers across quality tiers.

Regulatory and policy matrix — a practical guide to emerging trade measures, critical minerals policy interventions, and environmental compliance constraints in material-producing and consuming jurisdictions.

Company dossiers and strategic benchmarks — operational profiles, capacity footprints, technology positioning, and M&A readiness assessments for key APV producers and integrated players.

Actionable playbooks — procurement templates, JV term sheets, CapEx decision frameworks, and prioritized investment roadmaps tailored to producers, buyers, and financial sponsors.

The APV market exhibits moderate concentration: the top three producers account for a meaningful share of industry supply while the top five approach a clear majority of market presence (CR3 ~42.2%, CR5 ~58.4%). This structure favors firms with integrated feedstock access, scalable purification capability, and diversified offtake relationships.

Key industry players profiled in the report include:

EVRAZ plc (Moscow) — a globally integrated vanadium producer with established ammonium polyvanadate operations focused on metallurgical applications. Their asset base and downstream linkages position them to capture ferrovanadium demand, but exposure to regional geopolitics requires counterparties to scrutinize supply risk clauses and compliance due diligence.

Panzhihua Iron and Steel Group Vanadium Titanium New Material Technology Co., Ltd. (Panzhihua) — vertically integrated from vanadium-titanium magnetite feedstocks, this group benefits from feedstock capture and scale advantages. For strategic partners, their model underscores the value of upstream integration in managing margin volatility.

Chengde Xinhua Hebei Vanadium Products Co., Ltd. (Chengde) — specializes in converting vanadium slag to ammonium polyvanadate with a focus on chemical and metallurgical applications. Their expertise highlights opportunities in value-added processing of secondary feedstocks.

Hebei Jianlong Vanadium Products Co., Ltd. (Qian'an) — an established intermediate supplier driving high-purity vanadium pentoxide feedstreams; their positioning is a bellwether for purity-driven product strategies targeting specialty applications.

Treibacher Industrie AG (Althofen) — a Western European supplier oriented towards catalysts, specialty chemicals, and commercial grades; represents an archetype for diversified, premium-focused suppliers in regulated markets.

Across these profiles, common strategic levers emerge: feedstock security, product differentiation by purity and particle engineering, geographic diversification of conversion capacity, and contractual frameworks that shift price/quality risk.

For 2026, PW Consulting highlights three high-impact risk scenarios decision-makers must monitor:

Concentrated supply shock: A material disruption in a major producing country triggers short-term tightness, accelerating contract renegotiations and spot premiums. Pre‑emptive actions include expanding strategic inventory and activating alternate processing routes.

Policy-driven reshoring: Accelerated Critical Raw Materials programs lead to subsidies for local processing and stricter import controls. This changes the cost calculus for globally integrated producers and calls for early engagement with policymakers.

Technology substitution or standardization: Rapid uptake of VRFBs and higher-spec catalyst formulations increases demand for high‑purity APV, while standardization of grades could compress margins for commodity suppliers. Firms should evaluate premium product roadmaps and certification programs.

Concrete steps that should be actionable for stakeholders as they set 2026 budgets and strategies:

Producers: Accelerate projects that secure feedstock continuity (long-term mineral rights, tolling agreements), implement modular purification capacity that can be ramped with demand, and pursue selective partnerships in demand centers to de-risk offtake.

Buyers (steel, chemicals, battery OEMs): Structure multi-year, index-linked contracts with quality tiers, invest in supplier development programs that prioritize traceability, and develop contingency inventories tied to rolling price‑risk metrics.

Financial sponsors and investors: Use the report’s cash-flow sensitivity templates to stress-test project returns under volatility scenarios, and favor assets with integrated value chains or proprietary purification technologies.

Policy makers: Consider targeted incentives for secondary feedstock recycling, support R&D for lower‑impact extraction, and design critical‑minerals frameworks that balance domestic security with global trade obligations.

Beyond strategic recommendations, the report equips teams with operational tools needed for execution in 2026:

Supplier scorecards and a procurement negotiation checklist focused on quality imperatives, transit risk, and regulatory compliance.

CapEx prioritization matrices that align purity upgrades and debottlenecking investments with expected margin expansion under different demand scenarios.

M&A and JV playbooks including valuation adjustments for feedstock security and stranded-asset risk under decarbonization pathways.

Technical annexes mapping APV grades to downstream process requirements, enabling engineering and procurement to translate material specs into measurable procurement KPIs.

The APV market is entering a period where strategic foresight, supplier governance, and product differentiation will materially influence competitive position. PW Consulting’s study quantifies the growth runway and lays out the practical steps companies must take to convert macro trends into commercial advantage. With the market projected to nearly double from the 2025 base by the end of the forecast window and a mid‑market structure that favors integrated and quality‑focused players, the window for decisive action in 2026 is narrow but navigable for well-prepared organizations.

This briefing is a distillation designed to orient decision-making. The full PW Consulting Worldwide Ammonium Polyvanadate (APV) Market report contains the granular regional and application splits, price-model datasets, producer capacity tables, and company-level financial impact analyses that we intentionally omit here to preserve the actionable edge for subscribers. Stakeholders preparing 2026 strategies should obtain the complete report and the accompanying scenario toolset to operationalize the insights summarized above.

For detailed analysis of this topic, please visit the official page:Worldwide Ammonium Polyvanadate (APV) Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com