Worldwide Insect Repellent Supplies Market — Strategic Outlook for 2026

As businesses prepare budgets, product roadmaps, and M&A pipelines for fiscal 2026, the insect repellent supplies sector is emerging as a resilient, innovation-led market that rewards precise strategic positioning. PW Consulting's new market study synthesizes five years of historical performance and seven years of forward-looking forecasts to equip executives with the judgement required to allocate capital, prioritize channels, and shape R&D investments in a market that is both consumer-driven and regulation-sensitive.

Worldwide Insect Repellent Supplies Market

Executive snapshot: why 2026 is a decision point

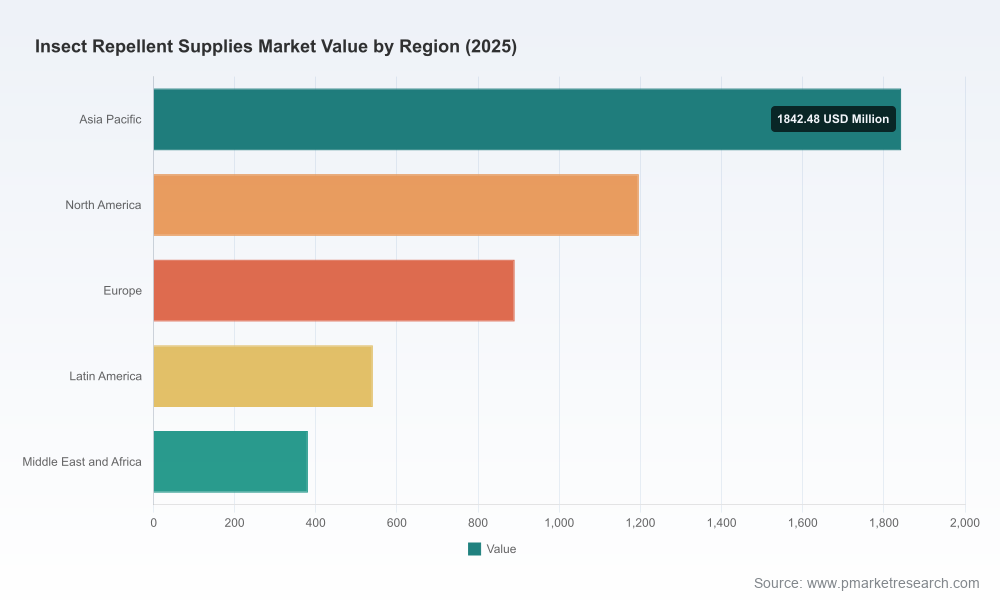

Global demand for insect repellent supplies has expanded steadily over the past half-decade and the underlying fundamentals point to continued growth. Our analysis shows the market reached approximately USD 4.85 billion in 2025 and is projected to accelerate in 2026 and beyond — with an average annual growth rate (CAGR) of roughly 6.3% across the 2026–2032 forecast window. That trajectory reflects a confluence of secular drivers: increased outdoor recreation post-pandemic, expanding vector-borne disease priorities in public health, rising consumer willingness to pay for premium and device-based protection, and sustained innovation in both synthetic and natural actives.

Worldwide Insect Repellent Supplies Market

What makes this report strategically valuable for 2026 planners

- Actionable, scenario-based forecasts calibrated to policy shifts and raw-material availability — not only point estimates, but downside and upside pathways that model regulatory action, ingredient shortages, and accelerated product adoption.

- A synthesis of go-to-market playbooks proven across territory types: how leading firms balance national brand strength, private label partnerships, e-commerce growth, and trade/retailer alliances to defend margin under price pressure.

- Decision-ready M&A and partnership matrices that highlight bolt-on and capability-building targets (actives, device platforms, and regional manufacturing footprints) — with integration checklists and a shortlist of high-impact moves for near-term value creation.

- Practical commercial tools: price-elasticity models, SKU rationalization frameworks, and channel-cost-to-serve benchmarks that let manufacturers and distributors test alternative investments and forecast margin impact.

Market trajectory and underlying demand drivers

The market’s mid-single-digit CAGR through 2032 masks important structural shifts. Growth is being underpinned by three durable trends: first, product diversification as consumers move beyond traditional sprays and coils toward device-based and fabric-treatment solutions; second, formulation bifurcation, with both proven synthetic actives and accelerating adoption of natural/plant-derived alternatives; and third, channel evolution driven by e-commerce, direct-to-consumer launches, and an uptick in institutional procurement for hospitality, tourism, and public-health programmes.

Worldwide Insect Repellent Supplies Market

For executives, the implication is simple: scale remains important, but sustainable margin expansion now requires product and channel differentiation, tighter control of active-ingredient sourcing, and a data-driven approach to SKU portfolios.

Regulatory and raw-material dynamics that will shape 2026 outcomes

- Regulatory testing and approvals increasingly influence market access and product claims. For example, contemporary EPA guidance establishes specific efficacy testing against Aedes, Anopheles, and Culex species for skin-applied repellents; this raises the bar for new entrants and increases time-to-market for claim-driven formulations.

- Age-and-label constraints for certain natural actives—such as some oil of lemon eucalyptus formulations—create differentiated market opportunities and constraints across demographics; product design and marketing strategies must internalize these label implications early in development.

- EU biocidal regulation and dossier requirements continue to be a gating factor for both incumbents and newcomers. Suppliers of active ingredients that support formulators through licensing or dossier services retain outsized negotiating leverage.

- Supply-side specialization for key actives (e.g., plant-derived Citriodiol and synthetic picaridin) means procurement strategy is now a strategic capability. Firms that secure resilient, low-cost access to these actives — or develop substitutes — will protect margin and time-to-market.

Competitive landscape — who matters and why

The insect repellent supplies market exhibits moderate concentration but remains competitive: the top three firms control a meaningful slice of the market while top-five concentration approaches the majority of sales, leaving room for regional champions and specialist suppliers to prosper. Market participants fall into several strategic archetypes, and each archetype points to a different playbook for 2026.

- Global brand leaders (e.g., established consumer-goods multinationals) leverage scale across manufacturing, distribution, and trade partnerships to fund premiumization and large-scale promotional pushes. Their advantage is speed-to-shelf and trade influence, but they must continually defend relevance through product innovation.

- Regional champions and emerging-market specialists excel at portfolio breadth, local consumer insights, and cost-effective manufacturing. Their strategic focus is share gains where local incumbency and distribution networks are decisive.

- Technical and niche innovators (material science, device makers, active-ingredient suppliers) drive product differentiation through patented delivery systems, controlled-release technologies, and specialty actives — catalyzing new adjacencies in outdoor and professional markets.

- B2B and service-oriented players combine product sales with pest-management services, capturing higher lifetime value from institutional clients such as hospitality and municipal portfolios.

Representative companies across these archetypes include long-established consumer-packaged-goods firms, specialized ingredient manufacturers, device manufacturers, and outdoor-focused brands. Each has chosen distinct pathways: brand extension into new formats, premium natural lines, device-led area protection, or B2B service bundling. For competitive planners, the question is not whether to compete on product alone, but how to assemble capabilities (formulation, manufacturing, regulatory, channel management) to create a defensible proposition.

Recent catalytic developments and their implications

- M&A activity and technology tie-ups are reshaping supplier capabilities. Notably, strategic acquisitions that expand biological control capabilities or active-ingredient portfolios materially change the competitive calculus for formulators and device makers.

- Product innovations — including DEET-free natural formulations and rechargeable device launches with improved battery and usability profiles — are accelerating consumer trial and upcategory movement. This is widening the addressable market for premium devices and natural SKUs.

- Capacity expansions in select geographies demonstrate how supply-side investments can unlock faster regional growth. Localized manufacturing can be a competitive moat as tariff and logistics volatility remain.

Risks and near-term uncertainties

- Regulatory shocks or tightening of dossier requirements can impose step-function increases in compliance cost, delaying launches and raising development budgets.

- Concentration of key active-ingredient supply chains creates vulnerability to shortages and price spikes; companies without hedging strategies or alternative sourcing will face margin pressure.

- Rapid product proliferation may push retailers to demand SKU rationalization or aggressive promotions, compressing margins for weaker brands.

What the PW Consulting report contains — practical chapters and tools

- Market sizing and seven-year forecasts with scenario analysis and sensitivity testing to regulatory and raw-material shocks.

- Competitive profiling and a capability map that highlights which firms control critical patents, dossier support, and regional distribution.

- Commercial playbooks for premiumization, private-label strategy, e-commerce activation, and institutional sales — each with ROI models and implementation checklists.

- Procurement and supply-chain playbooks for active ingredients, including supplier risk scoring and alternative sourcing options.

- M&A screening matrices and integration roadmaps tailored to acquisitions of actives, device platforms, and regional manufacturing capacity.

Strategic priorities for executives in 2026

- Prioritize a hedged procurement strategy for critical actives while evaluating backward-integration or long-term supply agreements with high-quality suppliers.

- Invest selectively in device-based solutions and fabric treatments that command higher price points and recurring revenue potential.

- Develop clear regulatory and claims roadmaps before product launch — incorporate efficacy testing against priority vector species to avoid late-stage modifications.

- Pursue portfolio simplification: eliminate low-velocity SKUs and reallocate promotional spend to high-growth, high-margin formats.

- Assess M&A targets for capability gaps (ingredient access, dossier ownership, device IP) rather than geographic coverage alone.

How to use this intelligence

For strategy teams and commercial leaders, this report functions as both a market compass and an operational playbook. Use the scenario forecasts to stress-test capital allocation decisions, apply the channel and pricing modules to refine P&L forecasts, and use the supplier risk frameworks to harden procurement plans before 2026 sourcing cycles. For investors and corporate development teams, the M&A and partnership mapping delivers a prioritized list of target archetypes and integration checklists that cut weeks from diligence.

Next steps — where to get the granular intelligence

This briefing provides the strategic highlights and practical implications drawn from PW Consulting’s deep-dive study. The full report contains the granular country- and channel-level forecasts, SKU-level pricing models, and the detailed segmentation tables that are essential for execution planning. For a tailored briefing, scenario walk-through, or to license the full dataset and slide-deck, please contact PW Consulting through our corporate channels; our analysts will guide you to the section of the report most relevant to your 2026 decisions.

PW Consulting’s Worldwide Insect Repellent Supplies Market study is designed for leaders who need reliable, implementable intelligence — not only to forecast market size, but to activate strategy and secure advantage as the market scales toward the end of the decade.

For detailed analysis of this topic, please visit the official page:Worldwide Insect Repellent Supplies Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com