Why Is Photoacoustic Imaging Market Emerging as a Breakthrough in Advanced Medical Diagnostics?

Networking |

2026-06-03 10:38:28

PW Consulting’s new market study, Worldwide Nuclear-Grade LED Lighting Market (base year 2025, forecast 2026–2032), frames a moment of strategic choice for utilities, vendors, EPC contractors, and investors. The nuclear-grade LED lighting market has matured from a niche safety component into a measurable industrial category: after growing from a 2020 baseline of USD 302.15 Million to USD 385.5 Million in 2025, the market is projected to expand at a 5.85% CAGR over the 2026–2032 forecast window to reach an estimated USD 573.94 Million by 2032.

Worldwide Nuclear Grade LED Lighting Market

Procurement cadence and plant modernizations converge in 2026. Many operators who deferred large-scale retrofit programs during the early 2020s are aligning capex cycles with extended operational life programs and small modular reactor (SMR) initiatives. Lighting—once regarded as a low-risk, low-value systems item—now carries outsized operational and safety value because of regulatory scrutiny, decontamination requirements, and interoperability with safety-monitoring systems.

Worldwide Nuclear Grade LED Lighting Market

Qualification timelines drive lead-time risk: gamma testing, LOCA compatibility validation, seismic qualification (IEEE-344), and 10CFR50 Appendix B quality program compliance require long lead times and specialized test facilities. Decisions initiated in 2026 will determine vendor qualification and installation schedules for multiple projects through the end of the decade.

Worldwide Nuclear Grade LED Lighting Market

Supplier consolidation and specialization are accelerating. The market shows moderate concentration: the top three suppliers account for roughly 38.5% of reported revenue, while the top five represent about 52.4%. This structure leaves room for niche specialists with unique test credentials or integrated manufacturing advantages and also signals that larger incumbents are actively defending share via product upgrades and certification investments.

Regulatory alignment is non-negotiable. Nuclear-grade lighting must satisfy seismic qualification (IEEE-344), extended emergency illumination requirements connected to 10CFR50 Appendix R, and standards such as IEC 62954 for environment control in emergency facilities. In practice, this constraint turns lighting procurement into a cross-discipline engineering and compliance exercise rather than a commodity purchase.

Radiation tolerance and LOCA compatibility remain gating factors. Industry test practices include gamma irradiation trials (e.g., testing to levels like 156 kGy) and LOCA-compatible designs that avoid external driver shielding. Achieving and documenting these capabilities in supplier dossiers materially reduces operational risk but raises sourcing costs and qualification timelines.

Materials and maintainability matter. Stainless steel housings, decontaminable finishes, and component selection to tolerate radiation doses (up to accelerator and pool-tolerant levels in select products) are differentiators that affect total cost of ownership (TCO) through maintenance, worker exposure time, and lifecycle replacement cadence.

The competitive field is composed of global specialty manufacturers, regional specialists, and OEMs that have adopted nuclear qualification pathways. PW Consulting’s analysis highlights a set of companies whose strategic moves and product capabilities are shaping the market.

DITO Lighting d.o.o. (Gorica pri Slivnici, Slovenia) — A vertically integrated developer with ultra radiation-resistant portfolios (H-, N-, and L-Series) for air and underwater nuclear applications. Recent product upgrades (e.g., the U-50 model’s custom CoB LEDs, enhanced mechanical and thermal architecture, and integrated safety features such as Safe Mode and thermal protection) demonstrate how incremental R&D and platform consolidation reduce qualification complexity for buyers. DITO’s integration of A-Series technology into the L-Series (now L-25) reflects a push toward platform unification that simplifies spare parts and qualification matrices for utilities.

Luminos Nuclear / Nanocut d.o.o. (Hrastnik, Slovenia) — Noted for gamma-hardened luminaires and in-house mechanical, LED and driver production capabilities. Their documented gamma testing to high kilogray levels and LOCA compatibility positions them as a supplier of record for facilities demanding rigorous radiation qualifications.

BIRNS, Inc. (Oxnard, CA, USA) — Offers high-tolerance fixtures such as the Quantum floodlight and ELF-LED emergency units, with products designed for long-duration post-event illumination and seismic performance aligning to IEEE-344. Their emphasis on extreme radiation tolerance and emergency illumination duration addresses the upper bound of utility risk scenarios.

G&G Industrial Lighting (Malta, NY, USA) and other U.S.-based vendors (Homewood Energy Services, Martek Lighting, LED Lighting Supply) — These suppliers emphasize compliance with U.S. regulatory programs (10CFR50 Appendix B), seismic qualification, maintenance-free emergency power systems, and NRC/FERC-related documentation—attributes that appeal to North American nuclear operators and EPCs.

Specialist vendors in Europe and Russia (e.g., Ahlberg Cameras, AO Sosny R&D Company) — Focus on niche applications such as pool lighting, hot cells, and containment CCTV-integrated illumination, combining radiation tolerance with domain-specific engineering.

Across the vendor set, two themes recur: in-house manufacturing and vertical integration (drivers, LED engines, housings) shorten qualification paths and increase pricing power; and demonstrable test credentials (gamma testing, LOCA compatibility, seismic qualification) materially influence procurement shortlists.

PW Consulting’s report is designed for decision-makers who must move from compliance checklists to executable procurement and investment strategies. Key deliverables include:

Market sizing and scenario-driven forecasts (historical 2020–2025 baseline, 2026–2032 projection with quantified mid and downside pathways).

Supplier benchmarking dossiers: capability maps, test credentials, manufacturing footprints, and programmatic risk scores that convert vendor claims into procurement-ready decision criteria.

Regulatory and testing matrix detailing required standards (e.g., IEEE-344, IEC 62954, 10CFR50 Appendix B/R), typical test timelines, and mitigation strategies for facilities with mixed vintage systems.

Operational playbooks for procurement, including sample RFP language focused on qualification artifacts (gamma test reports, LOCA testing statements, seismic certificates), maintenance planning templates, and TCO models that incorporate radiation-driven obsolescence and decontamination costs.

M&A and partnership screening criteria—how to assess bolt-on opportunities (niche manufacturers with test labs) versus scale acquisitions (platform consolidation to capture service contracts and spares).

Start vendor qualification now. For projects commencing in late 2026 and beyond, initiate long-lead qualification activities this year. Gamma testing and LOCA compatibility validation are not optional; they are the gating items that dictate installation windows.

Prioritize suppliers with documented in-house testing and vertical integration. The premium paid for integrated suppliers is often offset by reduced qualification time, simplified spare-part inventories, and lower lifetime maintenance exposure.

Embed regulatory requirements into procurement scoring. Treat seismic qualification, post-fire safe shutdown illumination duration, EMC compatibility, and Appendix B compliance as pass/fail thresholds rather than weight-scored desiderata.

Design for decontaminability and worker exposure reduction. Choosing housings and finishes that minimize contamination adhesion reduces outage durations and lowers dose uptake for maintenance crews—an operational ROI that is frequently underestimated.

Use the market concentration profile to your advantage. Mid-tier specialists can offer differentiated capabilities and faster customization, while the top-tier vendors provide scale and service networks. Mix-and-match strategies—validated through two-stage qualification—often yield optimal TCO and resiliency.

PW Consulting’s assessment combines financial-grade market sizing (USD 385.5 Million in 2025, 5.85% CAGR through 2032 to an estimated USD 573.94 Million) with practical operational tools that translate standards and test reports into procurement outcomes. The report’s supplier dossiers, procurement playbooks, and risk-adjusted TCO models are focused on the real-world timelines and compliance constraints that will determine whether 2026 initiatives succeed or stall.

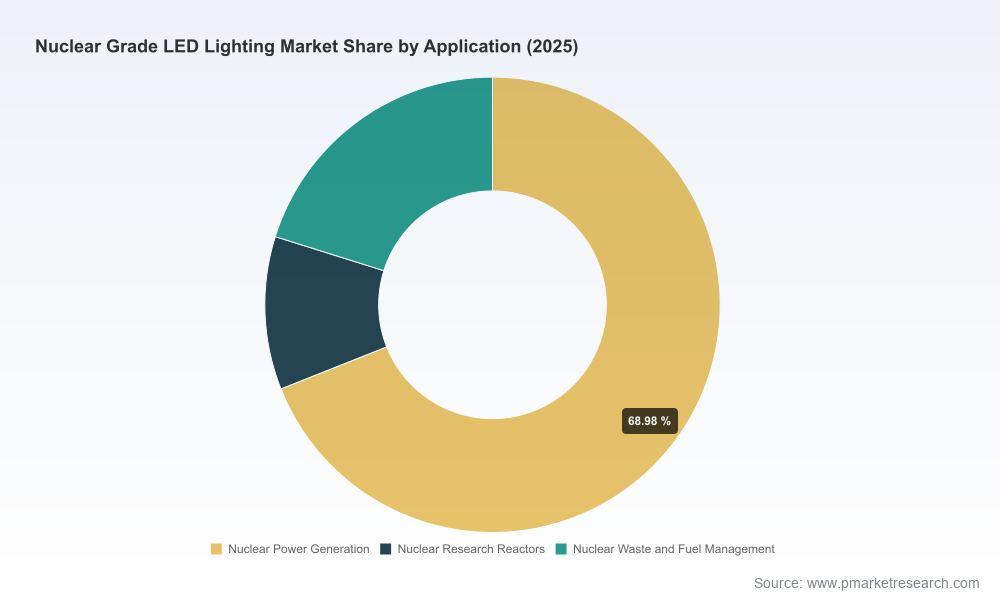

To preserve strategic advantage for our clients and to encourage direct engagement with source materials, the report intentionally omits public disclosure of the full segmentation tables and certain region/application share figures in this press summary. The full report contains those detailed splits, including granular regional and application forecasts, product-level unit economics, and downloadable vendor qualification templates.

Procurement teams: request the vendor qualification checklist and the RFP template to accelerate 2026 sourcing cycles.

Engineering and compliance leaders: obtain the regulatory matrix and test-timeline planner to align internal verification with vendor certification plans.

Investors and M&A teams: review the M&A screening annex to identify high-value targets where test-lab ownership or platform consolidation unlocks margin expansion.

For the full dataset, supplier dossiers, and the procurement playbook referenced here, access the PW Consulting report landing page where subscribers can download the complete Worldwide Nuclear-Grade LED Lighting Market study and supporting annexes.

For detailed analysis of this topic, please visit the official page:Worldwide Nuclear Grade LED Lighting Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com