Worldwide Brake Force Sensors Market — Strategic Preview for 2026 Decision-Makers

As PW Consulting’s Senior Strategy Advisor and Chief Industry Analyst, I present a focused preview of our newly published Worldwide Brake Force Sensors Market report. This briefing outlines the strategic value embedded in the full study for executives planning capital allocation, product roadmaps, partnerships, and compliance strategies in 2026. The analysis synthesizes market sizing, growth trajectories, competitive dynamics, regulatory inflection points, and executable go-to-market playbooks — while intentionally withholding detailed subsegment tables and split-level figures to preserve the commercial value of the full report and encourage engagement with our primary deliverable.

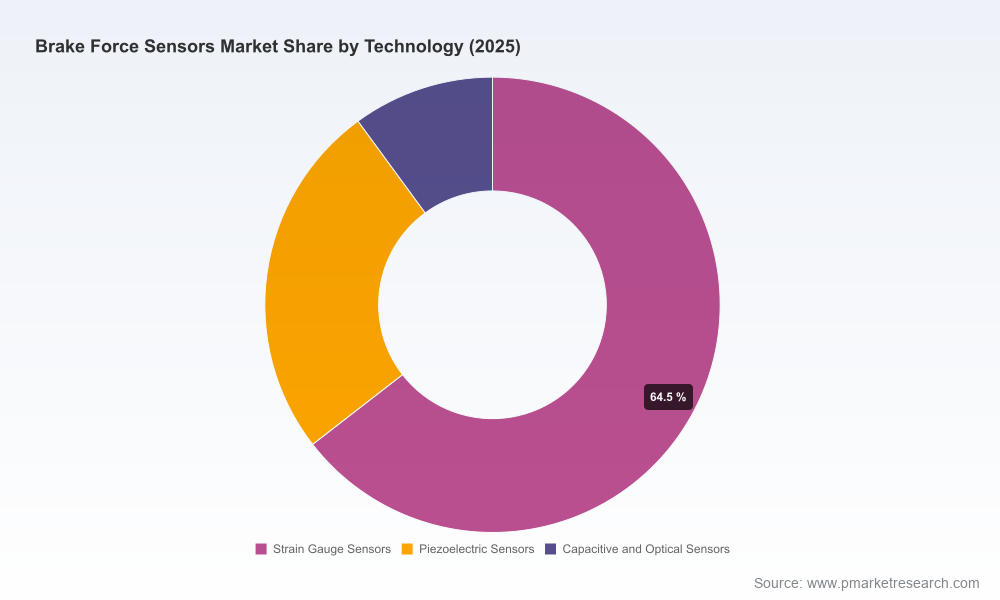

Worldwide Brake Force Sensors Market

Why this market matters in 2026

The brake force sensors market has evolved from a niche testing and validation tool into a mission-critical component of modern braking architectures — spanning hydraulic systems, electromechanical platforms, and the emergent x-by-wire and brake-by-wire designs underpinning next-generation EVs and advanced driver assistance systems (ADAS). Our analysis shows the market has expanded strongly during the 2020–2025 base period and is projected to sustain high-single-digit compounded annual growth through the 2026–2032 forecast horizon, driven by regulatory mandates, EV adoption, and the migration from open-loop to closed-loop brake control.

Worldwide Brake Force Sensors Market

Key macro takeaways you need for 2026 planning:

Worldwide Brake Force Sensors Market

- The market demonstrates robust expansion from the 2020 baseline through the 2025 base year and continues to accelerate across our forecast window; our modeling yields a compound annual growth rate (CAGR) of 9.2% for the forecast period.

- Concentration metrics indicate a market where a small group of established suppliers exerts meaningful influence but does not yet create insurmountable entry barriers: CR3 and CR5 metrics in the mid-range reflect a sector with focused incumbency and room for specialty/playbook-driven entrants.

- Regulation and functional safety are primary demand drivers: forthcoming regulatory requirements for automated emergency braking, combined with ISO 26262 FuSa expectations and heavy-vehicle brake performance standards, materially raise the bar for supplier qualification and product certification.

How the report supports 2026 enterprise decisions

Executives use PW Consulting’s market studies to move from strategic ambiguity to executable plans. For 2026 decisions — where budget cycles, product development timelines, and certification programs converge — our report provides the precise inputs teams need:

- Actionable market sizing and forecast models (historical 2020–2025 base and 2026–2032 forward-looking projections) to underwrite revenue assumptions, capital expenditure, and break-even timelines.

- Techno-commercial playbooks that connect sensor technology choices to cost, reliability, and integration complexity across braking architectures — enabling product managers to prioritize R&D and platform bets.

- Regulatory impact matrices that translate FMVSS updates and ISO 26262 implications into project milestones and certification cost estimates, reducing surprise risk during vehicle type-approval cycles.

- Supplier and OEM decision frameworks (make vs. buy models, sourcing risk heatmaps, qualification checklists) to accelerate procurement cycles while maintaining FuSa compliance.

- Mergers & acquisitions and partnership diagnostics that identify target profiles (technology depth, production readiness, application domain) and valuation levers for strategic consolidation or capability access.

Competitive landscape — who matters and why

The brake force sensor space is shaped by component specialists with strong automotive relationships, test-and-measurement providers, and firms that combine sensing with systems-level capabilities. Our report profiles the leading players and evaluates strategic positioning, technological differentiation, and production-readiness considerations. Representative company profiles included in the study (summarized here to show the depth of our competitive workstream) include:

- Sensata Technologies (Attleboro, MA): A significant strategic player with Micro Strain Gauge (MSG) solutions purpose-built for direct clamping-force measurement in electromechanical and dry brake calipers. Sensata’s MSG-based approach is optimized for closed-loop control in EMB systems — and its production nominations with major brake-system manufacturers position it to capture volume as EMB deployments accelerate.

- Methode Electronics (Chicago, IL): Provider of magnetoelastic brake pedal force sensors that measure driver-applied force using non-contact technology. Methode’s solutions are particularly relevant to emergency brake booster and pedal force measurement domains where reliability and signal integrity under long service cycles are essential.

- TE Connectivity (Schaffhausen, Switzerland HQ): Supplies an array of force, pressure, position, and speed sensing elements that can be integrated into hydraulic, electromechanical, and x-by-wire architectures. TE’s strength is the ability to align sensor hardware with Functional Safety (FuSa) engineering and system-level integration assurance — a critical requirement for OEMs.

- FUTEK Advanced Sensor Technology (Irvine, CA): Specialist load-cell and pedal-force sensor manufacturer with products tailored for testing and measurement use-cases and validation labs. FUTEK addresses the high-precision end of the market where repeatability and calibration workflows are non-negotiable.

- Strainsert (West Conshohocken, PA): Offers both custom and standardized force sensors for R&D, durability testing, and OEM validation — making them a familiar partner for development programs that require bespoke sensor form factors and rapid prototyping.

- Althen Sensors (Leiden, Netherlands): Focuses on automotive force sensors including pedal and hand-brake force measurement devices, serving dynamic testing and safety validation requirements in European programs.

Collectively, these firms illustrate the dual competitive axes in the market: (1) deep, automotive-grade sensor hardware and FuSa integration; and (2) precision test-and-measurement solutions for R&D and validation ecosystems. Our competitive heatmaps and supplier-selection frameworks in the full report translate these axes into procurement and partnership choices for OEMs and Tier-1 suppliers.

Regulation and safety — near-term inflection points

Regulatory developments materially accelerate demand and raise technical thresholds. Notable dynamics our clients must budget for in 2026 planning include the regulatory push for standardized AEB functionality on light vehicles and evolving heavy-vehicle brake performance requirements — all of which presuppose reliable brake actuation sensing, traceable measurement data, and FuSa-compliant integration. ISO 26262 remains the backbone of functional safety in automotive sensor deployments; early alignment with ASIL mapping and safety-case construction reduces time-to-production and limits costly redesign cycles.

We also track specific rulemaking that intersects with sensor demand. For example, recent regulatory updates requiring broader AEB coverage on light vehicles create an additional vector of aftermarket and retrofit opportunity — while simultaneously increasing the certification burden for OEMs integrating new brake-by-wire subsystems.

Technology and product strategy implications

For technology strategy leaders, the report identifies three pragmatic avenues to capture 2026 upside:

- Prioritize FuSa-first product architectures. Sensor suppliers that can demonstrate ISO 26262-aligned development processes, traceability, and fail-operational design earn preferred-supplier status with OEMs implementing closed-loop brake control.

- Design for system co-validation. Brake force sensing is most valuable when paired with pressure, position, and speed inputs; offering validated sensor fusions and diagnostic routines shortens OEM integration timelines.

- Modularize product families. Standardized sensor platforms with configurable interfaces (signal conditioning, diagnostics, and mechanical footprints) reduce NRE and increase cross-platform uptake across passenger, commercial, and off-highway applications.

Commercial playbooks for 2026

Our commercial recommendations — shaped by supplier concentration analysis, OEM procurement behavior, and regulatory timelines — focus on three executable plays for 2026:

- Fast-follower co-development with Tier-1s: Engage in limited-risk, high-visibility pilots that place your sensor into an EMB or brake-by-wire demonstrator, backed by a clear qualification timeline and safety artifacts.

- Systems-enabled differentiation: Bundle sensing elements with diagnostic software and FuSa documentation to convert product sales into platform agreements and longer-term integration contracts.

- Targeted M&A or strategic alliances: Acquire or partner with specialty test-and-measurement firms to offer end-to-end validation services — a value proposition that addresses OEMs’ need for certified measurement evidence during homologation.

What the full report contains (practical detail, without the splits)

PW Consulting’s full Worldwide Brake Force Sensors report delivers the end-to-end intelligence practitioners need to act in 2026:

- Granular time-series market sizing and scenario-based forecasts (2020–2032) calibrated to adoption curves, regulatory milestones, and EV penetration scenarios.

- Proprietary channel and supplier maps, production readiness assessments, and supplier scorecards keyed to FuSa maturity and volume manufacturing capability.

- Techno-economic models that quantify total cost of ownership, manufacturing cost curves, and sourcing sensitivity to raw material and labor cost swings.

- Playbooks for regulatory compliance, including actionable checklists for ISO 26262 alignment and FMVSS-related testing and documentation requirements.

- Acquisition screening criteria, synergy frameworks, and valuation benchmarks for targets in sensing, signal conditioning, and test-equipment sectors.

Next steps for executive teams

For 2026 strategy cycles, prioritize three near-term activities: (1) align product roadmaps to FuSa and AEB timelines; (2) validate supplier shortlists against production nomination readiness; and (3) initiate targeted pilot programs that can be converted to production contracts contingent on certification milestones. The full PW Consulting report supplies the models, supplier assessments, and regulatory translation tools needed to operationalize each activity without reinventing the analytics.

PW Consulting’s market intelligence is built to be actionable: if you are planning product launches, capital investments, or M&A activity in brake sensing and brake system integration for 2026, our complete study provides the datasets, scenario tools, and supplier diagnostics to accelerate decision cycles with confidence. To access the complete report, datasets, and tailored advisory support, please visit PW Consulting’s report page or contact our advisory team for a briefing and license options.

For detailed analysis of this topic, please visit the official page:Worldwide Brake Force Sensors Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com