Worldwide Industrial Wiping Cloth Market — Strategic Outlook for 2026

PW Consulting’s latest market research, Worldwide Industrial Wiping Cloth Market (base year 2025; forecast 2026–2032), delivers a pragmatic, decision-focused view of a market that has quietly expanded from the periphery of industrial procurement to a strategic lever for cost, quality, and sustainability outcomes. With the global market valued at USD 4,520.0 Million in 2025 and modeled to grow at a compound annual growth rate (CAGR) of 5.15% through the forecast window, this study is designed to inform the critical commercial, operational, and M&A choices companies must make in 2026.

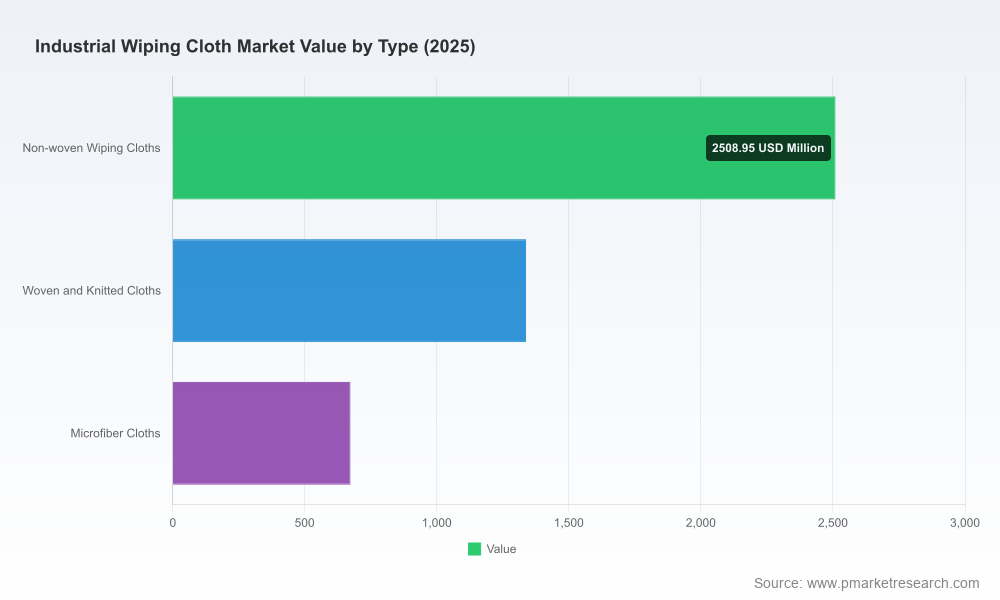

Worldwide Industrial Wiping Cloth Market

Why this report matters for 2026 decision-making

Industrial wiping cloths are no longer a commoditized line item; they sit at the intersection of maintenance efficiency, contamination control, regulatory compliance, and circular-economy commitments. Over 2020–2025 the market demonstrated steady expansion as manufacturing activity recovered and end-users reconfigured cleaning protocols to meet higher quality and sustainability expectations. Our forecast through 2032 captures both the near-term implications of raw-material and supply-chain dynamics and the mid-term structural shifts—such as service-based rental models and increased adoption of engineered nonwovens—that will determine winners and laggards.

Worldwide Industrial Wiping Cloth Market

Executives evaluating capital allocation, procurement strategy, or M&A targets in 2026 will use this report to: (1) quantify market scale and trajectory in USD Million terms; (2) benchmark competitive intensity (the market remains fragmented, offering roll-up and differentiation opportunities); and (3) stress-test supply chains and product roadmaps against plausible scenarios for raw-material availability, regulatory change, and sustainability commitments.

Worldwide Industrial Wiping Cloth Market

What’s in the report — practical, actionable deliverables

- Market model and forecast (2026–2032) in USD Million, with scenario sensitivity to commodity and demand shocks.

- Demand-driver analysis that links macro manufacturing trends to end‑use consumption patterns across automotive, general industrial, electronics, healthcare, food & beverage, and other key applications.

- Raw-material mapping: cotton rags, polyester blends, spunlace and other nonwovens, recycled textiles — cost drivers, sourcing risk, and substitution pathways.

- Supply-chain and procurement playbook: supplier scorecards, negotiation levers, inventory strategies, and nearshoring/dual‑sourcing frameworks tailored to wiping consumables.

- Sustainability and circular-economy roadmaps: carbon opportunity mapping, recycled-content strategies, end-of-life solutions (rental/refurbish/recycle), and compliance checklists aligned with evolving standards.

- Competitive landscape dossiers: profiles and strategic positioning for leading and regional producers, plus capability maps for manufacturing, distribution, and service delivery.

- M&A and partnership heatmap: targets, valuation multiples range, integration risk checklists, and post-merger playbooks focused on margin accretion and service expansion.

- Commercial tools: price-index series, cost-per-use comparators, and pilot-spec templates for laboratory and in-field validation.

Competitive landscape — what executives need to know

The industrial wiping cloth market is characterized by a broad mix of legacy manufacturers, specialized engineered-wipe producers, regional wholesalers, and innovative service providers. Market concentration metrics show a low top-tier share, indicating fragmentation and fertile ground for consolidation by buyers and private equity alike.

- Established U.S. manufacturers (examples include firms known for long histories in cloth manufacturing and distribution) generally compete on product breadth, established distribution channels, and deep relationships in automotive and janitorial segments. Their strengths include logistics networks, private-label capabilities, and scale in commodity-grade textile processing.

- Engineered-wipe specialists (producers focused on high-specification wipes for controlled environments) differentiate through formulation expertise, cleanroom certifications, and managed-supply contracts for critical-manufacturing customers. These firms command pricing premia where contamination control is mission-critical.

- Asia-based manufacturers combine cost efficiency with growing engineering capability, supplying both OEM programs and private-label clients worldwide. Their export orientation creates global sourcing options for buyers but also introduces supplier-dependence and lead-time risk that must be actively managed.

- Service-centric providers (rental and managed-supply models) are reshaping value propositions by offering asset-light alternatives—regular pickup, laundering, and replenishment—appealing to customers focused on total-cost-of-ownership rather than unit price.

Recent industry events—such as successive World of Wipes conferences and major trade shows—have accelerated technology diffusion around advanced nonwovens, sustainable feedstocks, and process automation. For corporate strategists, these gatherings are a reliable signal: R&D and supplier innovation pipelines are aligning toward higher-performance and lower-footprint products.

Key market dynamics that will shape 2026 strategies

- Raw-material volatility: Prices and availability for cotton, polyester, and specialty nonwovens remain a short- to medium-term risk. Procurers must adopt hedge-and‑sourcing frameworks and evaluate material substitution without degrading performance.

- Sustainability pressure and circular flows: Recycled textiles are increasingly cascaded into wiping-cloth applications, creating reputational and regulatory opportunities for early movers that can verify recycled content and lifecycle benefits.

- Service model proliferation: Rental and managed-supply offerings reduce client exposure to variability in demand and disposal costs; they also create recurring-revenue pathways for suppliers that can execute logistics and quality control.

- Fragmentation and consolidation: With a low combined share among the top competitors, the sector is ripe for strategic M&A—buyers can rapidly boost scale and distribution by pursuing bolt-ons or platform investments.

- Regulatory and standards evolution: Industry conferences and standard-setting bodies are actively debating criteria around biodegradability, chemical safety, and recyclability—firms that pre-empt compliance will preserve access to high-value customers.

Five strategic moves for 2026

- Reframe procurement around cost-per-use, not unit price. Pilot trials that measure downtime reduction, contamination avoidance, and disposal cost impacts to secure superior supplier terms.

- Prioritize supplier segmentation and dual-sourcing for critical materials. Balance low-cost offshore supply with regional partners capable of fast replenishment and quality consistency.

- Invest in sustainability differentiation where it matters—validated recycled content, take-back programs, or rental models—then translate those investments into price premiums with targeted customers.

- Use M&A strategically to acquire complementary capabilities: engineered wipes, rental logistics, or regional distribution hubs. Given the market’s fragmentation, disciplined consolidation can drive margin lift and market access.

- Create an internal “wipes center of excellence” to standardize specifications across plants and business units, accelerate product substitution trials, and centralize spend to capture scale economics.

How to use this research — next steps

PW Consulting’s report is built for active decision processes. Practical ways to extract immediate value in 2026 include:

- Running a 90‑day procurement sprint using our supplier scorecards and cost-per-use templates to reduce TCO on wiping consumables.

- Commissioning a tailored M&A screening exercise anchored on our heatmap to identify regional roll-up targets and service-capability acquisitions.

- Executing a pilot of a sustainability pathway (e.g., increased recycled content or a rental program) using our lifecycle assessment framework and validation checklist.

- Scheduling a strategy workshop with PW Consulting to translate market scenarios into a prioritized 18‑month roadmap (sourcing, product, and investment decisions).

Note on data access: This communication intentionally demonstrates the analytical depth of our study while omitting specific segmented revenue breakdowns and regional/application values to preserve the exclusive utility of the full report. The complete market model, segmented tables, and interactive dashboards are available in the source report and provide the precise inputs needed to operationalize the strategies summarized here.

Conclusion

The industrial wiping cloth market—valued in the low billions of USD and growing at a mid-single-digit CAGR—presents a mix of defensive and offensive strategic plays for 2026. Whether your priority is securing resilient supply, capturing sustainability premiums, or pursuing acquisitive growth, the right combination of procurement rigor, product innovation, and service design will determine competitive advantage.

PW Consulting stands ready to translate this research into executable plans: from rapid procurement sprints to full M&A diligence and post-merger integration. For a guided walkthrough of the model, access to company dossiers, or a tailored scenario workshop, contact our industrial consumables practice to schedule a briefing.

For detailed analysis of this topic, please visit the official page:Worldwide Industrial Wiping Cloth Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com