Worldwide Barrel Compressor Market — Strategic Imperatives for 2026 Decision-Makers

PW Consulting’s latest market study on the Worldwide Barrel Compressor Market (base year 2025, forecast period 2026–2032) provides a focused, decision-grade perspective for executives preparing multi-year capital plans, supply-chain contracts, and technology roadmaps. The global market reached approximately USD 5,420 Million in 2025 and is forecast to expand at a compound annual growth rate (CAGR) of 4.69% over the 2026–2032 period, reaching a materially larger market by the end of the horizon. This research is purpose-built to convert turbomachinery complexity into strategic options — highlighting where value will accrue, which capability sets will prove decisive, and how participants can de-risk projects in an environment of rising technical and regulatory complexity.

Worldwide Barrel Compressor Market

What this report delivers — practical intelligence, not hypotheses

- Transparent market sizing and baseline forecast (2020–2032) with scenario sensitivity for high/low demand and commodity-price paths.

- Actionable procurement and project-execution playbooks: tender design, lead-time reduction levers, alloy-hedging templates and recommended guaranteed-performance clauses.

- Supplier capability maps and vendor scorecards built from primary interviews, project delivery evidence and service-capacity audits.

- Commercial models for CAPEX/OPEX trade-offs, total cost of ownership (TCO) calculators, and aftermarket revenue projections tied to maintenance models and digital service adoption.

- Regulatory and standards primer (including the continuing relevance of API 617 and emerging revisions), with a compliance-readiness checklist for high-pressure and corrosive-service installations.

- Risk and continuity heatmaps across raw material exposure, manufacturing lead times, and critical-path long-lead items.

- M&A and partnership playbook highlighting likely targets, consolidation drivers, and value-capture mechanisms (service ecosystems, modularization, and digital retrofit).

Why this matters for 2026 strategy

Three converging forces are reshaping capital and operating choices for barrel compressors: an ongoing energy transition that drives demand into CCS, hydrogen and electrified offshore platforms; regulatory and reliability pressures that raise technical standards and compliance costs; and supply-side realities — long lead times for specialized alloys and concentrated manufacturing expertise. With the market growing at ~4.7% CAGR from the 2025 baseline, organizations face a classic timing problem: delaying vendor selection or service strategy increases schedule and cost risk, while premature supplier lock-in can forfeit optionality to capture emerging hydrogen/CCS opportunities. PW Consulting’s study equips leaders with the analytical tools to calibrate timing, contract structure, and technical scope to 2026 capital cycles.

Worldwide Barrel Compressor Market

Key market dynamics and what they mean for buyers and OEMs

- Raw material volatility and lead-time sensitivity: Manufacturing of barrel compressors depends on specialized steels and high-performance alloys for casings and impellers. Price swings and allocation constraints can materially affect quoted delivery dates and contingency costs. Our report models several raw-material shock scenarios and offers mitigation strategies, including shared-risk pricing mechanisms and strategic pre-purchase agreements.

- Standards and compliance: API 617 remains the industry cornerstone for centrifugal and barrel designs; a new edition is in development. Compliance-readiness now demands integration of regulatory checkpoints early in procurement and interface control documents. The report provides a compliance checkpoint matrix to reduce rework risk and schedule slippage.

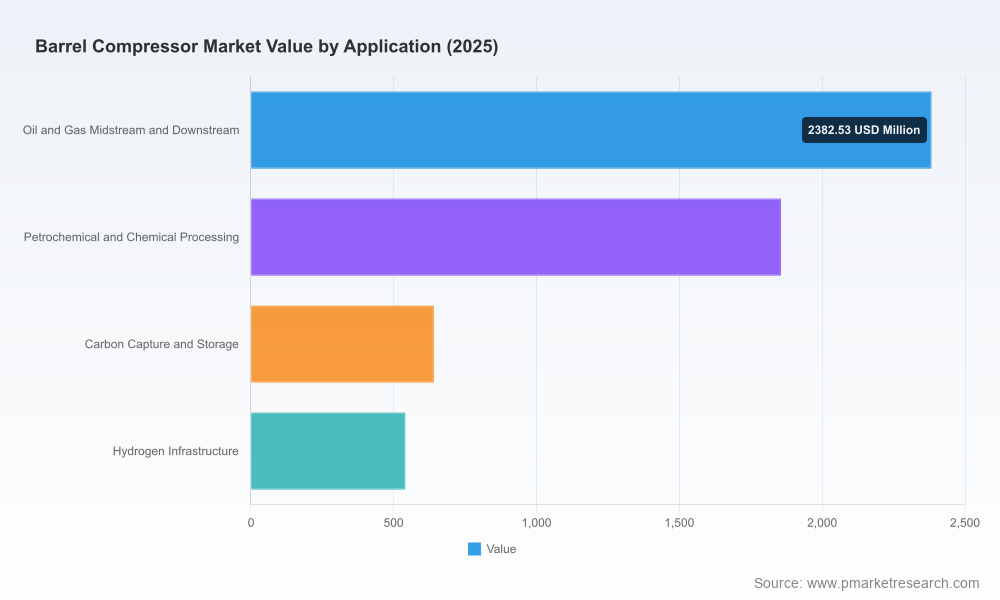

- Energy transition pull factors: Stricter emissions regimes and decarbonization programs are accelerating adoption of barrel-type compressors in CCS, hydrogen, and electrified offshore projects. These applications impose tighter tolerances, different materials, and enhanced sealing strategies. We map these technical requirements to supplier capabilities and aftermarket models — guiding engineering teams on specification choices that preserve retrofit flexibility.

- Design preference for vertically split (barrel) configurations: For high-pressure, corrosive, and offshore contexts, barrel-type compressors retain a durability and maintainability advantage — particularly where internal bundle removal without disturbing piping is essential. Our engineering appendix contrasts barrel architectures with alternative compressor topologies and highlights serviceability differentials that drive lifecycle cost.

Competitive landscape — established OEMs and capability moves

The barrel compressor market continues to be shaped by a set of global OEMs and integrators that combine product portfolios, project execution track records, and rapidly expanding service ecosystems. Market concentration metrics indicate a mid‑to‑high degree of aggregation among the largest producers, creating both stability and procurement leverage points for major buyers.

Worldwide Barrel Compressor Market

- MAN Energy Solutions (Everllence) — Germany: Renowned for RB barrel-type centrifugal compressors, modular packages and rebundling solutions. Recent contract wins in CCS projects demonstrate the firm’s ability to deliver complex, package-integrated skids for offshore CO2 applications.

- Baker Hughes — United States: Offers robust vertically split barrel compressor lines engineered for high-pressure CO2 and corrosive services, with a history of FPSO and offshore project execution that positions it well for integrated-systems demands.

- Siemens Energy — Germany: Provides single-shaft vertically split barrel-type machines rated for very high-pressure process duties. Its strength lies in single-source engineering for process-integrated compression trains and electrification-ready designs.

- Hitachi Industrial Products, Mitsubishi Heavy Industries Compressor Corporation (MCO), Kobelco Compressors (Kobe Steel Group) — Japan: Deep installed bases in refining and petrochemical services, with particular advantage in retrofit and project-execution in APAC markets. MCO’s recent acquisition of a Swiss rotating-equipment maintenance firm enhances its aftermarket and global service footprint.

- ShenGu Group, Atlas Copco Gas & Process, Elliott Group — China/Europe/US: These vendors bring differentiated scale, application-specialist designs (e.g., reforming, hydrocracking, hydrogen-rich services), and varied go-to-market approaches from integrated OEM supply to aftermarket-focused service platforms.

Recent notable developments captured in the report include strategic contract awards supporting CCS and FPSO projects, and targeted acquisitions strengthening aftermarket and maintenance capabilities. These transactions underscore the dual pathways to value capture: winning greenfield project scope and building recurring service revenue.

Actionable playbook for 2026 — five priorities

- Engage vendors earlier and lock technical gateways: Move vendor technical adjudication into FEED and pre-FEED stages to reduce late-spec change risk and control long-lead item ordering.

- Negotiate smarter risk-sharing: Use hybrid contracting that combines firm pricing for hardware with indexed pass-through for specified high-risk alloy items and agreed escalation caps.

- Design for service and retrofit: Specify interfaces and digital instrumentation today to preserve options for hydrogen or CO2 service conversions without full-train replacement.

- Prioritize aftermarket capability and digital twins: Aftermarket margins and uptime guarantees will drive lifetime value. Evaluate vendors for spare-part localization, condition-based maintenance capability and digital diagnostic platforms.

- Target M&A and alliance opportunities in services: For investors and OEMs, service companies with proven rotating-equipment maintenance expertise represent asymmetric value — they shorten time-to-market for high-reliability offerings and secure aftermarket revenue streams.

How PW Consulting’s deliverables translate into immediate actions

Clients who adopt the report’s templates and models can expect to shorten procurement cycles, reduce schedule overruns through earlier alloy procurements, and increase lifecycle value capture through targeted aftermarket investments. The report includes downloadable financial models to test contracting permutations, a vendor short-listing workbook calibrated to performance and delivery metrics, and a regulatory checklist tailored to high-pressure and corrosive installations.

Conclusion — where this intelligence is indispensable

For capital planners, project developers, OEM strategy teams and investors, the coming 24 months are decisive. The market is expanding at a moderate CAGR, standards and materials pressures are intensifying, and OEMs are consolidating service capabilities. PW Consulting’s Worldwide Barrel Compressor Market report converts these trends into executable decisions — while intentionally holding back certain granular segmentation tables and proprietary vendor scores so that purchasers engage directly for the full dataset and customizable outputs.

Accessing the full intelligence

This article is a strategic preview. PW Consulting’s full report contains the detailed segmentation matrices, supplier scorecards, downloadable CAPEX/OPEX models and primary-source contract-tracking that senior teams need to finalize 2026 procurement and investment plans. For tailored briefings, bespoke scenario runs, or to license the underlying datasets and vendor heatmaps, contact PW Consulting to request the full report and supporting workshops.

For detailed analysis of this topic, please visit the official page:Worldwide Barrel Compressor Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com