Worldwide Copper Hollow Conductors Market — Strategic Outlook for 2026

Executive summary

As we enter 2026, copper hollow conductors sit at the intersection of two durable secular trends: electrification of infrastructure and the continued intensification of high-field electromagnetics across medical, industrial and scientific applications. PW Consulting’s new report establishes that the global market has moved from roughly USD 212 million in 2020 to an estimated USD 277.65 million in 2025, and is projected to expand to just over USD 403 million by 2032 — a compound annual growth rate of 5.49% across the forecast horizon. For corporate leaders making capital allocation, procurement, and product strategy decisions in 2026, these high-level dynamics are a starting point; the value lies in translating them into targeted actions that manage price volatility, secure capacity, and align product roadmaps with evolving cooling, profile and conductivity requirements.

Worldwide Copper Hollow Conductors Market

Why this matters for 2026 decision-makers

- Market momentum is clear and sustained. The reported CAGR underscores a predictable growth envelope, creating a time window for measured investments in capacity and technology upgrades.

- Supply-side fragility and raw-material shocks now materially influence cost and availability. Procurement strategies that were merely “best practice” in 2023 are tactical imperatives in 2026.

- Application-led differentiation is sharpening supplier-buyer relationships. OEMs and integrators are increasingly sourcing conductors not as commodity copper, but as engineered subsystems demanding tighter tolerances, internal cooling channels, and materials traceability.

Market trajectory and macro headwinds

The market’s historical expansion and the forecast to 2032 reflect a balanced mix of replacement cycles in medical imaging, step-change demand from power generation/transmission projects, and bespoke needs in research and industrial induction heating. These drivers are amplified by broader macro factors: electrification programs, data-center expansion, and strategic public investments in power infrastructure.

Worldwide Copper Hollow Conductors Market

However, 2026 presents distinct headwinds and tailwinds. Copper price volatility — including a peak above USD 14,500 per metric tonne in January 2026 and ongoing spot fluctuations through spring — raises both procurement risk and margin pressure. Strategic buyers must assume periodic price shocks as a baseline planning assumption. At the same time, refiners and smelters are operating in an environment of compressed treatment and refining charges, which shifts margin and working-capital dynamics across the midstream.

Worldwide Copper Hollow Conductors Market

Raw material and cost dynamics: practical implications

- Hedging and contract design: Given elevated short-term volatility and differing forecasts across major houses, we recommend layered procurement contracts with blended indexation and optionality to capture upside while protecting against extreme spikes.

- Supplier risk profiling: Low TC/RCs at smelters and geographically concentrated refining can create pinch points. Buyers must incorporate upstream concentration metrics and contingency capacity into sourcing scorecards.

- Cost-to-serve analysis: When copper is a dominant cost driver, even small differences in manufacturing yield, scrap rates, and downstream processing can swing product economics. Investment cases for process improvements (e.g., reduced scrap in extrusion/drawing) often deliver superior ROI relative to short-term commodity hedges.

Structural demand pockets and product evolution

Demand is increasingly differentiated by conductor geometry, surface finish, and internal cooling capability rather than by raw cross-sectional area alone. Key trends we observed include:

- Rising specification intensity for internally cooled profiles supporting direct cooling of EV stators and high-field coils.

- Greater emphasis on tight-tolerance, custom-profile manufacturing for medical imaging and scientific magnets, which elevates technical barriers to entry and lengthens qualification lead times.

- Selective growth in circular and complex-profile demand where coilability and thermal performance are premium attributes.

These product-level nuances mean that strategic decisions on automation, tooling, and QC systems are not mere operational improvements — they are market-positioning moves that determine which customer segments a supplier can serve profitably.

Competitive landscape — what the leading players signal

The market is characterized by an active set of specialized producers and traditional copper fabricators who have adapted their capabilities to serve high-margin engineering applications. Leading companies in our coverage provide a useful lens into strategic playbooks:

- Luvata (Pori, Finland) leverages a breadth of tooling and short lead times to serve MRI and other high-field applications. Their focus on custom shapes and fast delivery highlights the premium value of flexible tooling and close OEM partnerships.

- KME (Germany) illustrates how large-scale copper manufacturers can translate upstream capabilities into engineered profiles and engage in digitalization projects along the value chain — an indicator that data-driven production monitoring is an emerging competitive differentiator.

- Proterial Metals (Japan) demonstrates the importance of material-grade control and established formulations (e.g., tough pitch copper) for legacy and high-reliability uses such as generators and particle accelerators.

- Mid-sized specialists — including cunova, Fabmann, Oriental Copper, Extube, S&W Wire, and Channel Metal — bridge commodity and engineered niches. Their differentiation rests on manufacturing precision, specific process routes (extrusion vs drawing), and geographic footprint.

Recent corporate developments reinforce these strategic directions. For example, KME’s research on digital data collection along the production chain points to an industry-wide push for traceability and process optimization, while product updates from other players emphasize shapes, tolerances and thermal management features for demanding applications.

What PW Consulting’s report delivers — operational, decision-ready intelligence

Our report is structured to be directly actionable for executives, investors and procurement teams preparing 2026 programs. Highlights include:

- Market sizing and scenario modeling: A base-case forecast (2026–2032) with upside and downside scenarios that explicitly map to copper-price, capacity and policy variables.

- Demand-driver dossiers: Application-level narratives (medical, induction, power, research) that translate technical requirements into procurement and product-spec decisions.

- Supplier benchmarking: Capability matrices that evaluate tooling breadth, lead times, material grades, tolerance capabilities, and geographic risk — enabling shortlists and supplier segmentation without divulging client-sensitive procurement heuristics.

- Unit-cost and margin sensitivity: A transparent cost-model (built on publicly available inputs and supplier-validated assumptions) that shows how margin responds to copper price movements, yield improvements, and automation investments.

- Supply-chain risk playbook: Tactical mitigations — alternative processing routes, dual-sourcing frameworks, inventory strategies, and contractual clauses — designed for three procurement archetypes (asset-light buyers, integrated OEMs, and upstream fabricators).

- M&A and partnership roadmaps: Go-to-play options for private equity and strategic acquirers, including integration checklists, break-even analytics and capability-closure frameworks.

Strategic recommendations for 2026

Based on our analysis, firms should prioritize a small set of coordinated actions this year rather than dispersing efforts across many fronts:

- Lock in strategic capacity where shape- and tolerance-specific tooling is scarce. For buyers, this may mean multi-year offtake agreements with staged price collars rather than spot purchases.

- Invest selectively in yield improvement and scrap reduction programs at the manufacturing edge. The payback on process upgrades is amplified when copper is expensive and TC/RC dynamics compress upstream margins.

- Differentiate on services: offer traceability, test-data packages, and rapid prototyping as part of the product bundle. These services shorten qualification cycles for OEMs and justify premium pricing.

- Adopt a portfolio approach to raw material risk: combine passive hedges (e.g., physical inventory buffers) with active instruments (layered forward purchases, options) and supplier-level contingencies.

- Use partnerships to enter higher-value segments. Where tooling and certification cycles are long, collaborative product-development agreements reduce time-to-market and distribute qualification costs.

How to use the report in your 2026 planning

Executives should treat the PW Consulting report as a decision-support toolkit: use the scenario models to stress-test capital projects, the supplier benchmarking to inform negotiation targets, and the cost-sensitivity work to set price-floor and price-ceiling triggers in contracts. Investors will find the M&A playbook and the supplier capability matrices useful for identifying consolidation targets and value-creation levers.

Next steps and access

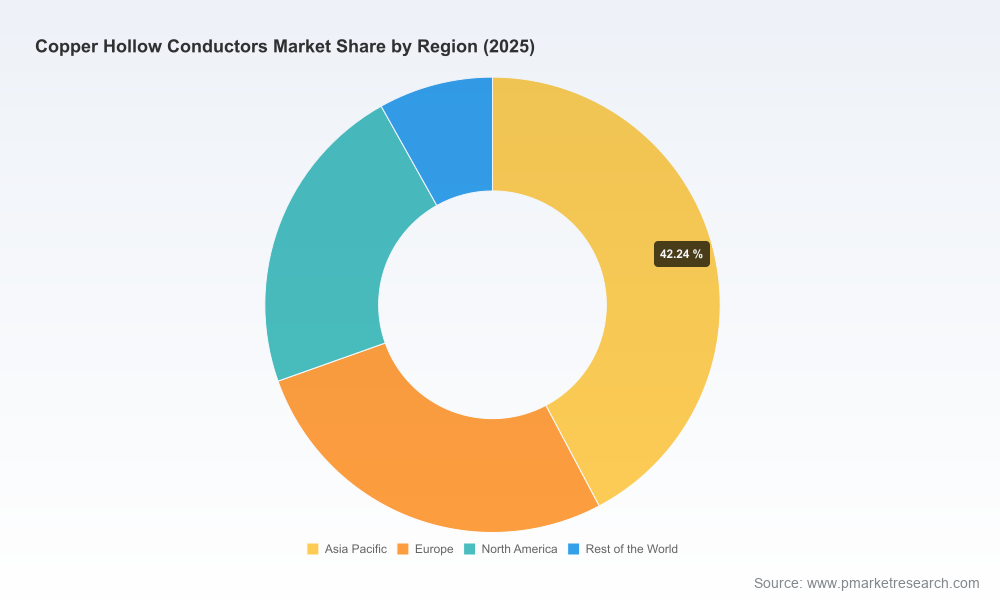

We have intentionally designed the public executive summary to surface the structural trends, risks and strategic responses that matter for 2026 without publishing detailed segment allocations and proprietary company-level shares. For procurement teams, OEMs and investors seeking the full datasets — including the granular segmentation, supplier scorecards, model inputs and downloadable scenario files — please visit the PW Consulting report page to obtain the complete report and associated annex materials.

PW Consulting remains available to brief executive teams and boards on bespoke implications of the report for specific corporate strategies, including tailored supply-chain stress tests, bid evaluations, and acquisition target assessments.

For detailed analysis of this topic, please visit the official page:Worldwide Copper Hollow Conductors Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com