New Projects in Narsingi Hyderabad – Brochure, Pros & Cons, PriceSheet with Detailed Floor Plans | Housiey

Home |

2026-06-23 09:46:10

PW Consulting’s new market study on the Worldwide Rubber Accelerator BZ (ZDBC) Market is designed as an executive-grade strategic tool for companies making procurement, product and M&A decisions in 2026 and beyond. Built on a 2020–2025 historical base and a 2026–2032 forecast horizon, the report frames a clear growth trajectory for ZDBC-based accelerators: the market is estimated at approximately USD 425 million in 2025, and PW projects a compound annual growth rate (CAGR) of 5.12% through the forecast window, taking the industry to the USD 600‑plus million range by the early 2030s. This release is intended to help senior leaders convert macro momentum into defensible, high‑impact actions — while preserving the proprietary segment-level intelligence contained in the full report.

Worldwide Rubber Accelerator BZ (ZDBC) Market

Performance and process advantages: ZDBC (commonly referenced as BZ) continues to be prized for rapid cure characteristics at relatively low temperatures, a performance profile that drives adoption across tire, latex and a wide spectrum of industrial rubber applications where cycle time and energy intensity are commercial constraints.

Worldwide Rubber Accelerator BZ (ZDBC) Market

Regulatory and safety tailwinds: The shift toward low‑nitrosamine accelerators and heightened workplace emissions controls — particularly in tire and latex manufacturing — creates both compliance pressure and opportunity. Chemical registration regimes such as REACH remain a gating factor for market access in key markets, shaping sourcing and product positioning strategies.

Worldwide Rubber Accelerator BZ (ZDBC) Market

Input‑cost and supply chain vulnerability: ZDBC manufacture is materially linked to inputs such as zinc oxide and downstream intermediates. Volatility in those feedstocks and concentrated manufacturing geography for some upstream materials means procurement strategies must factor supply security and cost pass‑through scenarios.

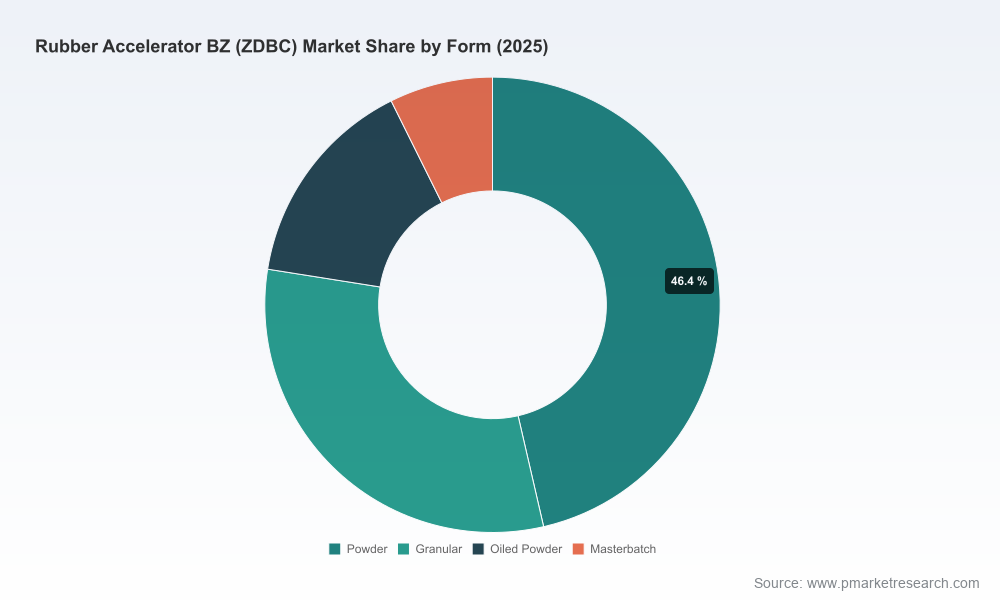

Industry structure: The market displays moderate concentration — the top three and five suppliers account for a meaningful share of demand — which simultaneously lowers the bar for scale advantages and increases the strategic value of distribution, formulation and masterbatch capabilities.

Procurement resilience: With steady mid‑single‑digit market growth and periodic feedstock cycles expected, procurement teams should establish multi‑sourcing playbooks, qualify polymer‑bound masterbatches and secure conditional supply agreements that include escalation and force‑majeure clauses aligned to zinc oxide market scenarios.

Product and process R&D: Manufacturers should invest in formulation work that exploits ZDBC’s fast‑cure traits while addressing nitrosamine reduction and worker exposure. The companies that pair accelerator chemistry with process optimization will capture cost and quality advantages.

Commercial positioning: Sales teams should map value to customer pain points (throughput, energy, safety) rather than price alone. Account‑level propositions that couple technical service, quality assurance and regulatory support outperform commodity approaches in this market.

M&A and partnerships: Given the market’s moderate concentration and the emergence of value‑added product forms (polymeric masterbatches, pre‑dispersed forms), bolt‑on acquisitions and strategic JV structures focused on masterbatch capabilities or downstream formulations are high‑value plays for mid‑sized suppliers seeking rapid scale.

The competitive map for ZDBC is a mix of global chemical majors, specialized regional producers and formulation specialists. Broadly, incumbent strengths reflect scale, regulatory compliance capability, and productization into masterbatches and pre‑dispersed forms. Key strategic profiles observed in the marketplace include:

Global specialty chemicals leaders — firms with international manufacturing footprints and established regulatory teams are advantaged in serving multinational tire and OEM customers. Their scale supports sustained investment in regulatory dossiers and supply chain redundancy.

Regional integrated suppliers — certain manufacturers combine local raw material integration, high‑volume production and cost competitiveness. These players are influential in price‑sensitive markets and can leverage export scale for selective global expansion.

Formulators and masterbatch specialists — companies that deliver polymer‑bound ZDBC masterbatches or pre‑dispersed products provide differentiated value to converters by reducing handling risk, improving dispersion and enabling easier dosing at production lines.

Selected competitive takeaways relevant for 2026 planning:

Technology differentiation remains centered on cure performance and occupational safety attributes. Companies that clearly demonstrate lower nitrosamine risk and provide validated processing gains will command a premium with strategic accounts.

Certification and quality systems are not optional. Recent developments in the industry include product line expansions targeting the U.S. market and formal quality system updates — signals that buyers now expect ISO‑level assurances plus technical documentation as a baseline.

China‑based and regional manufacturers continue to exert pricing and capacity influence, but premium specialty players retain the advantage in segments where regulatory compliance and technical service outweigh price considerations.

PW Consulting’s report is engineered for immediate application by strategy, procurement, R&D and business development teams. The full deliverable combines market sizing and a forward projection (2026–2032) with scenario analytics, supplier benchmarking and practical playbooks. Core components include:

Market model: A granular top‑down and bottom‑up demand model, with sensitivity runs incorporating feedstock shocks and regulatory scenarios, enabling rapid recalibration of internal forecasts.

Supply chain mapping: End‑to‑end mapping of raw material flows, geographic concentration points and logistics chokepoints, coupled with mitigations such as regional stocking and alternative chemistries.

Regulatory matrix: Country‑level compliance checklists (including REACH implications), occupational exposure guidance, and a timetable for anticipated regulatory milestones impacting accelerator use.

Commercial playbooks: Go‑to‑market strategies for premium versus commodity channels, distributor scorecards, and customer value propositions tailored to tire, latex and industrial rubber segments.

Deal support tools: A pre‑filtered M&A target list, valuation comparables, and integration checklists for acquisitions aimed at acquiring masterbatch or formulation capabilities.

Technical annex: Comparative performance summaries (lab method references), product specification checklists and quality protocol templates to accelerate supplier qualification.

Feedstock volatility: Monitor zinc oxide price and availability as an early‑warning indicator for margin compression and potential supply disruption.

Regulatory shifts: Track EU REACH updates and emerging nitrosamine standards in major consuming countries — these are likely to reshape qualifying criteria for high‑volume customers.

Product innovation: Observe new product launches and polymer‑bound masterbatches that reduce handling risk; early adopters may rewrite purchasing specifications at the converter level.

Consolidation activity: Given the market’s moderate concentration profile, keep an eye on bolt‑on acquisitions by regional champions and partnerships that extend distribution networks into new geographies.

CEOs and Business Unit Heads: Use the market growth trajectory and supplier landscape to align capital allocation — prioritize capacity or capability bets where projected returns exceed the underlying market CAGR and regulatory risk is manageable.

CPOs and Procurement Leads: Implement staged qualification of second‑source suppliers, and negotiate flexible contracts that include indexation to key feedstocks. Build scenario playbooks for supply disruption and price spikes.

R&D and Product Development: Accelerate validation programs that demonstrate both performance gains and reductions in nitrosamine formation; create modular masterbatch offerings to reduce customer friction.

Corporate Development: Use the report’s M&A screening and valuation framework to pursue acquisition targets that add masterbatch technologies, formulation IP or geographic distribution in under‑served markets.

PW Consulting’s Worldwide Rubber Accelerator BZ (ZDBC) Market study is intentionally positioned as a “trailer”: it demonstrates the depth of our proprietary modeling and strategic frameworks while reserving the detailed subsegment tables, supplier scorecards and downloadable data sheets for stakeholders who require full access. The macro picture is clear — a market expanding at a mid‑single‑digit pace with defined regulatory and supply risks — and the tactical pathways to capture value are executable today.

For access to the full dataset, supplier heatmaps, scenario models and tailored briefings for procurement, R&D or corporate development teams, please visit the report page linked in our release. PW Consulting can also deliver customized workshops that translate the study’s findings into a 90‑day action plan for your organization.

For detailed analysis of this topic, please visit the official page:Worldwide Rubber Accelerator BZ (ZDBC) Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com