Worldwide Essential Oil Blends Market — Strategic Briefing for 2026 Decision-Makers

Executive summary

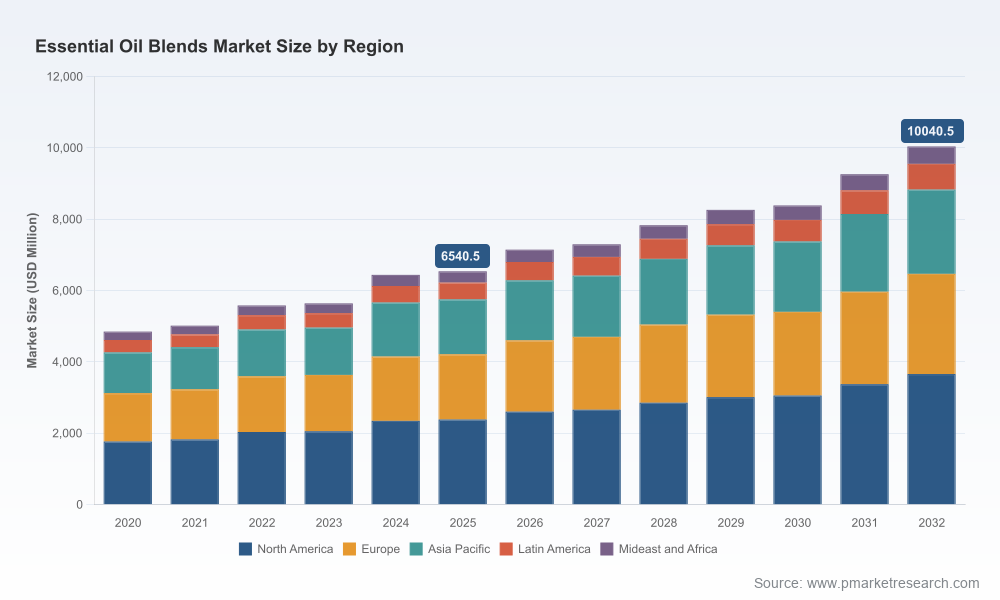

PW Consulting’s new market study on the Worldwide Essential Oil Blends Market (base year 2025; forecast 2026–2032) identifies a clear trajectory from a mid‑decade scale of roughly USD 6.5 billion toward a market expected to exceed USD 10.0 billion by 2032, reflecting a compound annual growth rate of 6.31%. This growth trajectory, underpinned by accelerating consumer wellness adoption, premiumization in personal care, and expanding B2B demand from fragrance and flavor houses, creates a narrow window in 2026 for strategic moves that will determine market leadership through the next business cycle.

Worldwide Essential Oil Blends Market

Why this report matters for 2026 decisions

2026 will not be "business as usual" for producers, ingredient suppliers, retailers or brand owners that source or commercialize essential oil blends. Converging forces — regulatory tightening, rising quality and traceability expectations, rapid product innovation in home wellness and cosmeceuticals, and shifts in sourcing risk profiles — mean that tactical responses taken this year will compound in value over the forecast period. PW Consulting’s study translates those forces into executable priorities for commercial, sourcing and regulatory teams.

Worldwide Essential Oil Blends Market

- Market momentum: The market scale and mid‑single digit CAGR signal sustained opportunity across premium and mainstream segments, but the shape of value capture will be uneven.

- Regulatory inflection: Industry deadlines and standards through 2025–26 change formulation constraints and compliance costs — firms that anticipate and operationalize compliance early will avoid disruptive reformulation and can claim credibility with demanding buyers.

- Supply volatility: Dominant raw material categories (notably citrus oils) and geographic sourcing concentrations create both margin upside and risk exposure; the companies that manage traceability and supplier diversification will reduce volatility and unlock premium pricing.

What the report delivers — practical, transaction‑ready intelligence

This is not an academic exercise. The report is structured to convert market intelligence into decisions you can implement in 2026:

Worldwide Essential Oil Blends Market

- Top‑down and bottom‑up market sizing calibrated to company and category inputs, with scenario overlays for slower/higher demand and regulatory cost impacts.

- Go‑to‑market playbooks by route‑to‑market (DTC, retail private label, B2B fragrance & flavor), including channel economics and margin models.

- Product innovation roadmaps (formulation pivots to meet IFRA/SCCS thresholds, organic certification strategies, and differentiation through stability and delivery systems).

- Supply‑chain resilience toolkit: supplier risk matrix, traceability checklist, and a sourcing diversification prioritization framework tailored to essential‑oil raw material buckets.

- Commercial diligence and M&A scoring templates for buyers and investors, plus a shortlist of value-creation levers for targets (cost-to-serve, channel expansion, premium licensing).

- Operational templates: quality assurance KPIs tied to ISO and GC/MS testing practices, and a regulatory tracker aligned with IFRA, REACH/CLP and ISO 210:2023 implications.

Competitive landscape — what incumbents and challengers are signaling

The market is populated by a spectrum of players whose strategic postures define where value will accrue:

- Therapeutic and DTC leaders (e.g., Young Living, doTERRA, Rocky Mountain Oils): These players leverage brand trust, proprietary sourcing narratives, and community‑based distribution to command premium positioning. Their strengths lie in direct consumer engagement and education — assets that translate into steady ASPs but also higher marketing and regulatory scrutiny.

- Quality‑and‑value challengers (e.g., Edens Garden, Plant Therapy, Aura Cacia): Positioning focuses on transparency (GC/MS testing, kid‑safe lines) and competitive pricing. These brands are the primary pathway to scale in mainstream retail and mass DTC; their agility in pricing and assortment management makes them natural buyers of private label and co‑packed capacities.

- Organic and sustainability specialists (e.g., Mountain Rose Herbs, Florihana, Biolandes, Aromaaz): Specialist suppliers defend margins through certification, traceability, and sustainable sourcing claims. They are logical partners for premium personal care brands and for B2B customers seeking verified organic inputs.

- Ingredient and fragrance majors (e.g., Givaudan, IFF, Symrise, The Lebermuth Company): These incumbents integrate essential oil blends into complex flavor/fragrance systems and large CPG ingredient programs. Their R&D and formulation scale gives them an advantage in regulatory reformulation, and they are likely to consolidate higher‑margin B2B opportunities.

- Large diversified ingredient manufacturers (e.g., NOW Foods): Offer cost leadership and broad distribution; they play a critical role in supplying baseline volumes for wellness and cleaning verticals.

For corporate strategists the implication is clear: competition is multi‑dimensional. Winning requires aligning brand equity, formulation capability, supply traceability and channel economics. The market is not tightly concentrated: leadership requires focused execution rather than simply scale.

Regulatory and raw‑material dynamics to watch in 2026

Regulatory developments that matured through 2024–25 reshape formulation ceilings and compliance timelines. The IFRA amendment cycle introduced ingredient obligations that impacted many legacy blends; the SCCS opinions — for example, confirmed safe concentration bounds for specific actives in cosmetics — mean formulators must build conservative safety buffers into personal care SKUs. ISO standards such as ISO 210:2023 set cross‑border quality and storage benchmarks that are now baseline expectations for procurement and trading partners.

From a raw‑material perspective, citrus oils remain a dominant component of the essential oils value pool and a key driver of blend formulation economics. That dominance amplifies exposure to weather, crop cycles and geopolitical sourcing shifts; companies that aggregate supplier intelligence and secure long‑term sourcing arrangements will realize a double benefit — reduced cost volatility and a marketing narrative for sustainability.

Strategic imperatives for 2026 — five actions that change your trajectory

- Operationalize compliance early: Convert IFRA/SCCS/REACH implications into SKU‑level action plans. Prioritize reformulation where required and deploy consumer communications to protect brand trust.

- Secure traceable supply lines: Invest in supplier mapping and third‑party verification (GC/MS, farm‑level audits). Pursue blended sourcing contracts and consider de‑risking via geographic diversification or contract farming.

- Segment by value capture, not just volume: Separate portfolios into “high‑trust therapeutic” offerings, organic/sustainability premium lines, and mainstream value SKUs — and apply differentiated go‑to‑market economics to each.

- Partner up the value chain: For brands seeking faster scale, co‑development with fragrance and flavor majors or private label partnerships can unlock distribution while preserving R&D control over therapeutic claims.

- Prepare for consolidation: With attractive mid‑market M&A opportunities, establish a playbook now for target screening, integration planning and post‑deal margin enhancement.

Tools and timelines — what PW Consulting provides to clients

Clients receive a practical deliverable set designed for immediate deployment in 2026: an interactive financial model (USD, revenue unit: Million), scenario dashboards (regulatory shock, raw‑material price spike, demand acceleration), supplier due diligence templates, SKU reformulation checklists, and a 90‑day commercialization playbook for launch or relaunch of blends.

Who should read this report

- CEOs and corporate development teams evaluating M&A or portfolio realignment.

- Product and R&D leaders responsible for formulation and compliance.

- Sourcing and procurement executives managing supplier risk and certification programs.

- Retail and private‑label managers planning assortment strategies for 2026–27.

Final perspective — why act in 2026

The essential oil blends market is neither ephemeral nor commoditized; it is an evolving, quality‑conscious ecosystem where brand narratives, formulation science and supply integrity intersect. Our analysis shows a substantive growth runway; but success will be determined by how quickly organizations translate regulatory signals and raw‑material realities into defensible commercial strategies.

PW Consulting’s Worldwide Essential Oil Blends Market report is designed as a catalyst for decision‑grade action. We intentionally present high‑level market sizing and strategic direction here while withholding detailed segment breakdowns and granular financial tables to preserve competitive integrity and to encourage direct engagement with the full dataset and models. For clients planning M&A, product launches, or supply chain redesign in 2026, the complete report and associated modeling toolkit are essential.

Next step

To access the full report, interactive model and a tailored briefing for your executive team, visit our publication page or contact PW Consulting to schedule a 60‑minute strategy session. In a market where timing and precision matter, 2026 will reward those who pair decisive strategy with operational rigor.

For detailed analysis of this topic, please visit the official page:Worldwide Essential Oil Blends Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com