Worldwide SPECT Camera Market: Strategic Imperatives for 2026

Executive snapshot

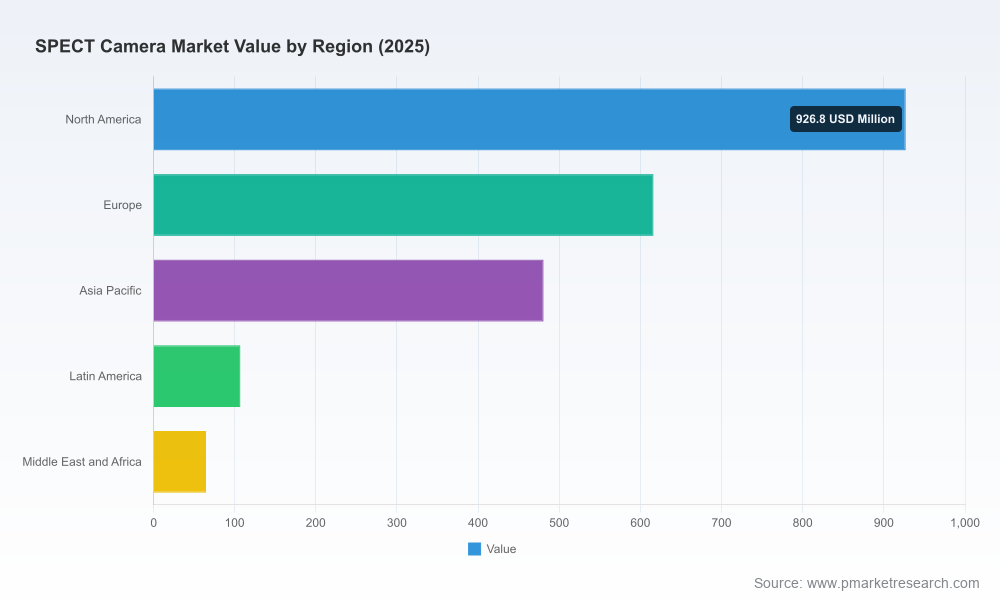

As healthcare providers and device manufacturers position themselves for the next cycle of capital allocation, the worldwide SPECT camera market has demonstrably moved from recovery to steady expansion. Total market revenue expanded from approximately USD 1.66 billion in 2020 to about USD 2.20 billion in 2025 and is forecast to continue growing at a mid-single-digit compound annual growth rate (CAGR) across the 2026–2032 horizon. Our base projections show continued upside as hybrid imaging, detector innovations and AI-enabled workflows accelerate clinical throughput and broaden clinical use-cases.

Worldwide SPECT Camera Market

Why this report matters to 2026 decision-makers

- Capital planning: Hospitals and imaging networks weighing refresh cycles can use the report’s procurement decision frameworks to prioritize investments that maximize utilization and margin in a constrained CAPEX environment.

- Product strategy: Device OEMs assessing R&D and commercialization priorities will find our roadmaps and technology adoption curves useful to time CZT, digital detector and AI investments.

- M&A and partnerships: Private equity and corporate development teams can apply our competitive heatmaps and valuation premia guidance to identify tuck-in targets, geographic expansion opportunities, and strategic alliances.

- Regulatory & reimbursement readiness: Our granular mapping of regulatory pathways and payer levers enables quicker market entry and revenue realization, particularly where 510(k) pathways and CPT/DRG dynamics influence economics.

- Service & lifecycle revenue optimization: Equipment-as-a-service, spare-parts logistics and remote service models are assessed to help service organizations lift annuity streams.

Market dynamics shaping 2026 choices

The SPECT market is being reshaped by three structural forces:

Worldwide SPECT Camera Market

- Technology convergence. Hybrid SPECT/CT platforms, compact solid-state detectors (CZT) and fully digital designs are converging with AI-driven reconstruction and workflow tools. The result: faster studies, improved diagnostic confidence, and an expanding set of indications beyond traditional cardiac applications.

- Concentrated competitive structure. The market displays high concentration at the top: the largest three suppliers account for roughly seven in ten dollars of global revenue, while the top five account for over eight in ten. That concentration creates both barriers and opportunities—scale advantages in service networks and manufacturing, alongside white-space pockets for specialized innovators.

- Regulatory and reimbursement friction points. SPECT devices remain regulated under well-established pathways (Class II devices under 21 CFR 892.1570 with prevalent 510(k) routes). Reimbursement remains patchwork: myocardial perfusion CPT codes, DRG bundles for inpatient cardiac procedures, and evolving payer expectations for claimed clinical utility all shape adoption velocity.

Competitive landscape — leaders, challengers, and what to watch

- GE HealthCare (Chicago, IL) — Strong installed base and a broad SPECT/CT portfolio focused on cardiac and oncology workflows. Recent clearances and AI-enabled quantification tools position GE as a leader in high-throughput cardiac imaging and enterprise-level deployment.

- Siemens Healthineers (Erlangen, Germany) — A portfolio approach that couples hybrid scanners with AI-driven workflow assistants. Recent regulatory milestones have validated its intelligent imaging play, offering customers demonstrable gains in exam consistency and staff productivity.

- Philips Healthcare (Amsterdam, Netherlands) — Emphasizes low-dose protocols and ergonomics, particularly for cardiac and oncology applications. Its strength lies in dose-optimization narratives and integration into broader imaging ecosystems.

- Spectrum Dynamics Medical (Caesarea, Israel) — A technology-led challenger leveraging CZT solid-state detectors to deliver markedly higher count sensitivity and faster scans. Its innovations create a premium niche in cardiac and targeted oncology imaging.

- United Imaging Healthcare (Shanghai, China) — An emergent full-stack provider with digital-detector whole-body SPECT/CT offerings. Its cost-competitive engineering and geographic expansion make it a focal point for developing-market growth strategies.

- Mediso (Budapest, Hungary) — Focused on both preclinical and clinical SPECT/CT solutions, Mediso is notable for applications in translational research and centers that bridge clinical and investigative imaging.

Recent regulatory developments further underscore the competitive dynamics: several vendors secured 510(k) clearances for AI-enhanced SPECT/CT systems across 2023–2024, signaling an FDA trend toward accepting intelligent imaging adjuncts that demonstrate workflow and analytic benefit. For incumbents, that means protecting installed bases by offering meaningful software upgrades; for newcomers, it lowers a technical barrier but raises the bar for clinical evidence.

Worldwide SPECT Camera Market

What the report delivers — practical, transaction-ready tools

Beyond market sizing and trend analysis, the report is structured for immediate operational use. Key deliverables include:

- Proprietary market model (Excel) with scenario toggles for pricing, utilization, and replacement cycles to stress-test investment cases.

- Regulatory pathway playbook mapping 510(k) requirements, key IEC testing standards for acceptance and QC, and a timeline of expected submissions across major jurisdictions.

- Reimbursement matrix linking CPT and DRG levers to revenue-per-study impacts and payer-specific nuance for high-value applications like myocardial perfusion imaging.

- Vendor benchmarking toolkit with scorecards across clinical performance, service footprint, upgradeability, and total cost of ownership.

- Go-to-market blueprints: channel strategy, tender and RFP templates, and service-commercialization models tailored for hospital systems and imaging chains.

- M&A screening filters and an integration checklist designed to accelerate diligence on targets with differentiated detector technology or strategic geography.

Three 2026 strategic scenarios and recommended plays

To turn insights into action we present scenario-driven roadmap options that reflect likely market inflection points in 2026–2028.

- Scenario A — Consolidation & Premiumization: If consolidation among top OEMs accelerates, pricing will bifurcate between premium hybrid platforms and commoditized standalone systems. Recommended play: prioritize retrofit programs and service annuities, negotiate enterprise-level agreements, and accelerate AI-based clinical value demonstrations to defend price points.

- Scenario B — Volume Growth in Emerging Markets: If adoption in emerging markets outpaces mature market upgrades, demand will skew toward cost-effective whole-body and digital-detector systems. Recommended play: deploy localized manufacturing or JV approaches, optimize pricing tiers, and design financing solutions for hospital CAPEX constraints.

- Scenario C — Technology Leap (CZT/Digital + AI): If CZT/digital detector penetration and validated AI reconstructions rapidly prove clinical and operational superiority, incumbents may face disruptive displacement in high-value cardiac and oncology niches. Recommended play: secure IP-light partnerships with detector specialists, accelerate clinical studies to support reimbursement, and pre-emptively structure trade-up pathways for existing customers.

Regulatory and reimbursement levers to prioritize now

- Design clinical evidence packages around the expectations of 510(k) reviewers and key professional societies (e.g., SNMMI) to reduce time-to-market and payer resistance.

- Map procedural reimbursement (including myocardial perfusion CPT codes and inpatient DRG implications) to revenue-per-study assumptions—this materially affects payback periods for high-cost equipment.

- Adopt IEC-based acceptance and QC protocols early in product and service rollouts to minimize post-sale friction with customer biomedical engineering teams.

Who should read this report

- CEOs and strategy leads at imaging OEMs planning R&D and M&A spend for the next 24 months.

- Hospital procurement and imaging service groups executing CAPEX and lifecycle refresh decisions in 2026.

- Private equity and corporate development teams evaluating buy-and-build or carve-out opportunities in molecular imaging.

- Regulatory affairs, reimbursement and clinical affairs teams preparing market-entry dossiers and payer evidence strategies.

How to act on these insights

This research is intentionally presented as a strategic trailer: it demonstrates the depth of methodology, proprietary scenario tools and competitive intelligence you need to act in 2026, while reserving the full segmentation matrices and raw numeric datasets for the complete report. Subscribers receive the interactive financial model, vendor scorecards and regulatory playbooks required to implement the scenarios above.

To drive 2026 decisions with confidence—whether that means prioritizing retrofit programs, accelerating a CZT partnership, or negotiating enterprise service contracts—use our market model to quantify outcomes under your specific assumptions. For access to the full dataset, downloadable models and vendor-by-vendor scorecards, visit the report landing page and request the executive data pack.

Conclusion

The SPECT camera market entering 2026 is mature but not static. A blend of technological innovation, concentrated competition and payer/regulatory dynamics means that well-timed decisions will deliver outsized returns. Our Worldwide SPECT Camera Market report equips leaders with the analytical scaffolding to make those calls—balancing clinical value, commercial defensibility and regulatory readiness in a market growing steadily into the next decade.

For detailed analysis of this topic, please visit the official page:Worldwide SPECT Camera Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com