Micro and Nano Programmable Logic Control (PLC) Market Size, Share, Trends, Growth Opportunities, Key Drivers and Competitive Outlook

Other |

2026-06-18 12:05:21

PW Consulting today releases a focused strategic briefing drawn from our full market research report, Worldwide Canine Mammary Tumor Treatment Market (base year: 2025; historical window: 2020–2025; forecast: 2026–2032). The global market has expanded from an estimated USD 590.25 Million in 2020 to USD 845.5 Million in 2025 and is forecast to grow at a compound annual growth rate (CAGR) of 7.58% through 2032, reaching roughly USD 1,410.05 Million by the end of the forecast horizon. These macro dynamics reflect accelerating demand for integrated surgical, medical, diagnostic and technology-enabled care in veterinary oncology and build a compelling case for disciplined investment and portfolio repositioning in 2026.

Worldwide Canine Mammary Tumor Treatment Market

Market timing: With mid-single-digit to high-single-digit growth supported by advances in precision medicine, radiotherapy deployment and translational research, 2026 is a pivotal year for initiating proof-of-concept commercial strategies that can scale through the forecast period.

Worldwide Canine Mammary Tumor Treatment Market

Competitive posture: The sector exhibits moderate concentration (CR3 ≈ 38.5%; CR5 ≈ 52.2%), indicating dominant incumbents alongside meaningful opportunities for specialty entrants and technology providers to capture differentiated value.

Worldwide Canine Mammary Tumor Treatment Market

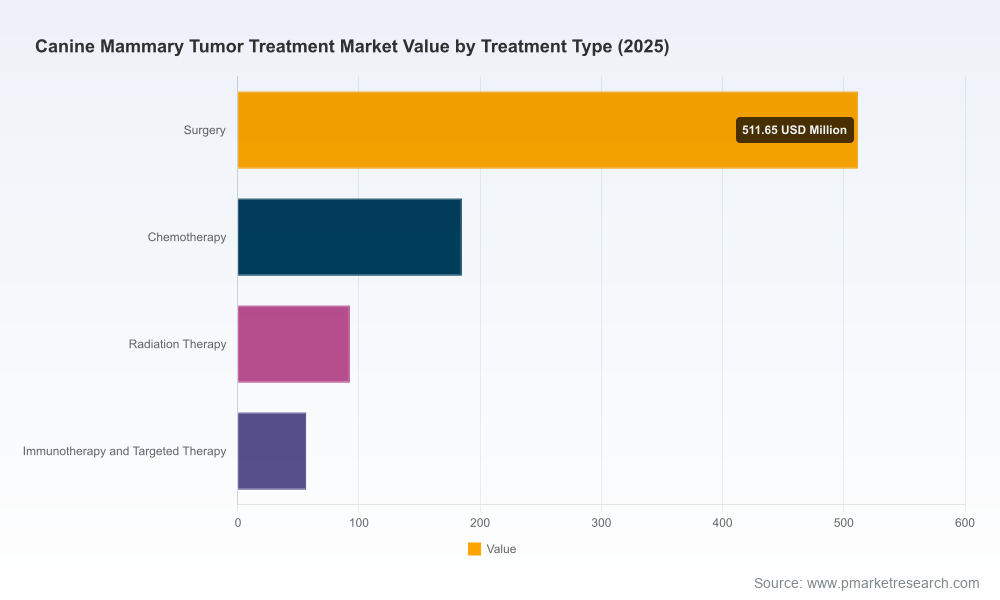

Clinical economics: Surgery remains the procedural backbone of treatment, and routine case economics (e.g., a single tumor resection commonly costing in the low-thousands of dollars range depending on clinical complexity) continue to define unit economics for veterinary providers—important when structuring pricing or bundled-service offerings.

Regulatory strategy: There is no full FDA approval specifically for canine mammary tumor indications; regulatory pathways such as MUMS (Minor Use in Major Species) and conditional approvals have emerged as pragmatic routes for accelerating access. Firms planning 2026 regulatory submissions must align evidence-generation with these specialized pathways.

Market-sizing and forecast models (2020–2032) calibrated to procedure volumes, treatment mix, and technology adoption scenarios—built to be linked directly to your internal financial models.

Scenario-driven revenue models that quantify upside from new diagnostics, targeted therapies, and expanded radiotherapy services under conservative, base, and aggressive adoption curves.

Clinical pathway maps and patient-flow analytics that show typical care sequences from presentation to long-term follow-up, highlighting intervention points where diagnostics, adjuvant therapies, and service innovations capture incremental value.

Commercial playbooks for veterinary hospitals, specialty oncology clinics and diagnostic labs, detailing go-to-market channels, pricing levers, training and vet adoption incentives.

Regulatory and reimbursement playbooks including MUMS/conditional approval routes, best-practice evidence packages, and recommended post-market surveillance protocols tailored to 2026 submissions.

Technology and capital investment appraisals for radiotherapy equipment, intraoperative imaging (e.g., Optical Coherence Tomography pilots), and precision-genomics platforms, complete with payback analyses and utilization thresholds.

Company-level competitive intelligence dossiers and partnership maps for the leading players in veterinary oncology, oncology diagnostics, and radiotherapy systems.

The competitive field blends large animal-health incumbents, human-oncology translational specialists, precision-diagnostics start-ups and capital-intensive radiotherapy providers. Our analysis in the report synthesizes company strengths and strategic vectors without disclosing confidential market-share allocations in this summary.

Zoetis Inc.: A clear leader in veterinary oncology pharmacotherapy, with a legacy product that has become a de facto reference for off-label targeted therapy use in canine cancers. Zoetis’ strength is a broad commercial footprint and established relationships with multi-specialty veterinary networks—critical assets for cross-selling adjunctive oncology support products and companion diagnostics.

Boehringer Ingelheim Animal Health and Elanco Animal Health: Large-platform players with scale in distribution, supportive-care portfolios, and a track record of growth via targeted acquisitions. Their strategic play is likely to focus on integrated care bundles and leveraging veterinary client networks to accelerate adoption of new adjuvant therapies.

Specialized biotech and translational firms (AB Science, Karyopharm, VetDC, CureLab): These companies drive the innovation frontier in small-molecule inhibitors, XPO1 modulators and immunotherapies. Recent regulatory progress—such as a MUMS designation for a tyrosine kinase inhibitor—illustrates how regulatory pathways can be used to de-risk veterinary oncology commercialization while clinical evidence is still being accrued.

Precision-medicine and service providers (FidoCure, PetCure Oncology, Accuray, Varian): Precision diagnostics and advanced radiotherapy are emerging as differentiators for specialty centers. Service-based models (genomics-guided therapy, stereotactic radiosurgery) present attractive margins and lock-in effects when bundled with ongoing patient management.

Regulatory advancement: A noted 2026 MUMS designation for a veterinary tyrosine kinase inhibitor underscores the strategic value of specialty regulatory pathways for companies seeking earlier market entry and payer visibility.

Technology-enabled surgery: Research into intraoperative Optical Coherence Tomography (OCT) is advancing as a mechanism to improve margin assessment and reduce recurrence—an operational lever that surgical centers and device incumbents should evaluate through 2026 pilot programs.

Comparative-oncology momentum: Canine mammary tumors continue to be an accepted model for human breast cancer research, creating partnership opportunities with human-biotech firms and opening translational funding and co-development channels.

Prioritize evidence-first commercialization: Allocate 2026 budgets to prospective, multi-site comparative trials that demonstrate survival or recurrence benefits for adjuvant therapies and adjunct imaging technologies. Early clinical differentiation will support regulatory filings (MUMS/conditional) and strengthen clinical guidelines uptake.

Invest in diagnostics-led go-to-market models: Genomics and actionable testing can accelerate targeted therapy adoption. Consider pilot partnerships with precision-medicine providers to bundle testing with real-world outcomes tracking.

Scale service offerings with capital-light models: Where capital expenditure is a barrier (e.g., radiotherapy systems), evaluate hub-and-spoke service centers or managed-service agreements to extend advanced treatment access without full asset ownership.

Leverage surgical economics: Because surgery remains the gold-standard primary treatment, design adjuvant products, education and reimbursement strategies that integrate with standard surgical workflows to minimize friction for veterinarians and pet owners.

Use targeted M&A and licensing as accelerants: Small-to-mid acquisitions of diagnostic platforms, specialty clinics or therapy candidates with clear comparative-oncology data can be an efficient route to fast-track market presence.

Design commercial KPIs aligned to clinical outcomes: Move beyond volume-based metrics and adopt recurrence rates, time-to-progression and treatment adherence as central commercial success indicators when contracting with specialty centers and third-party payers (where applicable).

Regulatory uncertainty — Mitigation: Early engagement with regulatory authorities and alignment on surrogate endpoints that reflect meaningful clinical benefit.

Adoption friction among practitioners — Mitigation: Invest in clinician education, decision-support tools and economic models that demonstrate comparative value at the clinic level.

Capital intensity for advanced radiotherapy — Mitigation: Explore service partnerships, revenue-share models and second-hand equipment upgrades combined with certification programs to accelerate deployment.

This summary is designed as a decision-ready primer for executives and business-unit leaders preparing budgets, R&D portfolios and commercial strategies for 2026. The full PW Consulting report contains the granular market segmentation, country-level forecasts, product-by-product revenue models, payer dynamics, and downloadable scenario models that underpin the insights summarized here. We intentionally withhold core sub-segment data in this press briefing to preserve the actionable intelligence available in the complete publication.

To access the full dataset, company profiles, and customizable financial models that support execution in 2026 and beyond, please refer to the report release on the PW Consulting website or contact our team to schedule a tailored briefing.

For detailed analysis of this topic, please visit the official page:Worldwide Canine Mammary Tumor Treatment Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com