RF Power MOSFET Market 2026 to Reach High Growth with 5G Expansion

Games |

2026-07-09 12:48:40

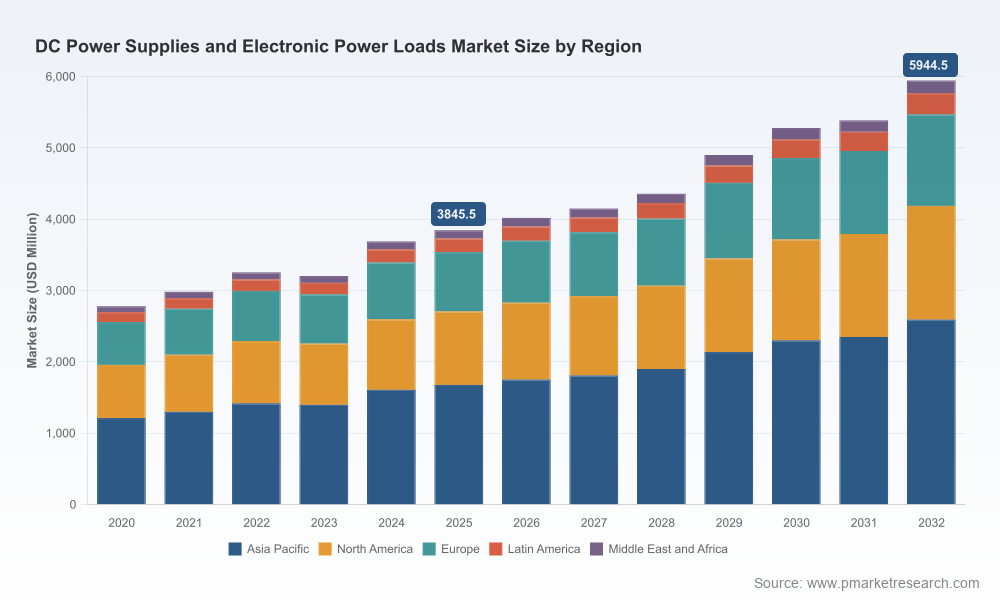

PW Consulting’s latest market study, Worldwide DC Power Supplies and Electronic Power Loads Market (base year 2025), synthesizes five years of historical performance and a seven‑year forecast to deliver a practical, board‑level playbook for executives making capital, product, and M&A decisions in 2026. The market demonstrated resilience and structural growth: after a brief cyclical softening in 2023, total industry revenues recovered to an estimated USD 3.85 billion in 2025 and are projected to grow at a compound annual growth rate (CAGR) of approximately 6.42% through our forecast window, reaching roughly USD 5.94 billion by 2032. Concentration metrics show a market that is neither fragmented nor monopolized — the top three firms account for about 38.4% of market share and the top five for roughly 52.2% — creating clear competitive tiers that reward scale and specialization.

Worldwide DC Power Supplies and Electronic Power Loads Market

Timing. 2026 is a pivot year: component cost inflation, shifting raw‑material controls, and an acceleration of high‑density power needs (EV traction, AI datacenters) are converging. Companies that align product roadmaps and supply strategies now will avoid margin erosion and delivery bottlenecks later in the decade.

Worldwide DC Power Supplies and Electronic Power Loads Market

Decision focus. Our analysis isolates actionable choices across product engineering (SiC/GaN adoption, regenerative load development), procurement (long‑cycle buys, dual sourcing), and commercial strategy (service monetization, automated test equipment integration).

Worldwide DC Power Supplies and Electronic Power Loads Market

Risk management. The report translates macro policy and commodity moves into probability‑weighted scenarios so leaders can quantify downside and rapidly trigger mitigation playbooks.

The market’s trajectory over 2020–2025 shows a technology market responsive to macro cycles and demand shifts in mobility, data infrastructure, and industrial electrification. The modest contraction observed in 2023 was followed by a renewed expansion driven by higher‑power and higher‑precision applications. Our forecast to 2032 reflects steady growth underpinned by three durable trends:

Power density and efficiency demands pushing adoption of SiC and GaN topologies and tighter thermal/power management.

Proliferation of bidirectional and regenerative capabilities as battery charging/discharging and energy recovery become mainstream in EV and renewable sectors.

Consolidation and tiering among suppliers where scale enables investment in R&D, custom ATE integrations, and global service footprints.

Our scenario work identifies several near‑term shocks that materially affect cost, lead time and strategic sourcing:

Export control and trade policy risk. Recent export controls on rare earths and related materials, together with trade actions tied to critical minerals, are elevating regional sourcing risks for magnetics and specialized components. These policy moves increase the value of geographically diversified supplier networks and in some cases encourage near‑shoring of critical subassemblies.

Component pricing pressure. In Q1 2026, key passives and capacitors saw price increases—tantalum and multi‑layer ceramic capacitors rose in the mid‑teens to 30% range—while power MOSFETs and IGBTs experienced price increases of roughly 10–20% alongside lengthening lead times. These input cost dynamics should be incorporated into BOM sensitivity models and product margin floors.

Technology adoption speed. SiC MOSFETs are rapidly displacing silicon in high‑voltage traction and DC‑DC converter roles; firms that delay architectural shifts risk higher lifecycle costs and competitive disadvantages in power density and efficiency.

The competitive topology is comprised of legacy power specialists, test & measurement leaders, and modular‑power innovators. Our company benchmarking section goes beyond logos to assess technical depth, route‑to‑market, and strategic intent. Representative players include Precision test OEMs and industrial power houses; notable examples (profiled in the report) include global firms offering programmable supplies, high‑power regenerative loads, and high‑density converter modules.

Test & measurement leaders: Companies with deep R&D in precision programmable supplies and electronic loads are positioned to capture higher margin R&D and production test business, especially in semiconductor and power‑device validation.

Industrial and modular specialists: Firms focused on compact, high‑efficiency AC/DC and DC/DC platforms (including early adopters of SiC/GaN) are carving durable niches in datacom, medical and industrial equipment.

Cost leaders: Vendors offering reliable, high‑volume enclosed units remain critical in automation and consumer‑electronics manufacturing where price/performance is the primary purchase criterion.

Recent vendor activity further sharpens competitive dynamics: new high‑voltage 1U DC supplies, SOSA‑aligned VPX DC/DC modules for aerospace, and new programmable bench units launched in early 2026 illustrate both the pace of product innovation and the segmentation between high‑value test equipment and volume industrial supplies. The report includes rolling competitor intelligence and product tracking to help buyers and investors anticipate next moves.

Packed with practical outputs, the study is designed to be directly operationalized by product managers, procurement leads and corporate strategists. Key components include:

Top‑down market sizing with historical validation and a granular bottom‑up forecast engine (scenario‑driven) through 2032.

Risk‑adjusted scenario analyses (policy shock, component inflation, demand surges) with trigger points and playbooks.

Vendor benchmarking across technology, product breadth, manufacturability, service network and pricing power; strategic positioning maps highlight acquisition and partnership targets.

BOM sensitivity and margin stress models to simulate the impact of component price swings and adoption of SiC/GaN on unit economics.

Commercial roadmaps and GTM templates for launching new programmable supplies and regenerative loads into automotive, data center and industrial segments.

Procurement and inventory tactics — from hedging approaches to long‑lead component contracts and near‑shoring criteria that minimize disruption risks.

An M&A playbook identifying capability gaps, valuation heuristics for strategic bolt‑ons, and integration checklists.

Immediate (0–90 days): run BOM sensitivity runs for next two major products using reported Q1 2026 component inflation metrics; secure strategic long‑lead buys where payback is under 12 months.

Near term (3–9 months): fast‑track design reviews to evaluate SiC/GaN substitution for medium‑to‑high voltage platforms; begin qualification of at least two alternative suppliers for critical magnetics and passives.

Medium term (9–18 months): develop regenerative load capability (or partner) for EV and stationary storage product testing; evaluate M&A targets that fill gaps in high‑density DC‑DC modules or automated test equipment.

The report frames three common tradeoffs with quantitative guidance:

Performance vs. cost. When to adopt SiC/GaN depends on total cost of ownership and speed‑to‑market; we provide a break‑even matrix by application class and projected component price paths.

Vertical integration vs. flexible sourcing. We quantify the payback horizon for internalizing magnetics and assembly versus securing long‑term supply contracts and multi‑region sourcing.

Service vs. product revenue mix. For test equipment vendors, the economics of adding lifecycle services (calibration, remote diagnostics, managed test capacity) often yields higher long‑term margins than incremental product sales — the report supplies LTV/CAC heuristics for this decision.

Use the findings to align capital allocation and product roadmaps to the market’s growth pockets and to harden your supply chain against policy and commodity shocks. Product leaders should convert the report’s BOM stress outputs into engineering change orders and prioritize features that reduce BOM sensitivity (modular power stages, software‑defined controls). Procurement and operations should implement the report’s supplier scoreboard and trigger arrangements for inventory thresholds. Corporate development teams should use the vendor bench‑marks to screen M&A targets and accelerate due diligence.

This release is designed as a strategic preview: it surfaces the critical directional signals, risk scenarios, and executable playbooks that matter for 2026 decisions while reserving the full segmentation matrices, granular regional/application splits, and vendor‑level financials for the full report. For teams preparing budgets, R&D roadmaps, or M&A pipelines this quarter, the full report includes downloadable models, scenario sliders and the vendor benchmarking database used for the concentration and competitive analysis.

To access the complete dataset, interactive models, and PW Consulting’s recommended implementation templates, please visit PW Consulting’s report page and request the Worldwide DC Power Supplies and Electronic Power Loads Market study for a comprehensive, actionable briefing.

For detailed analysis of this topic, please visit the official page:Worldwide DC Power Supplies and Electronic Power Loads Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com