Strategic Preview: Worldwide Shape Memory Alloys for Civil Engineering Market — PW Consulting 2026 Outlook

Executive summary

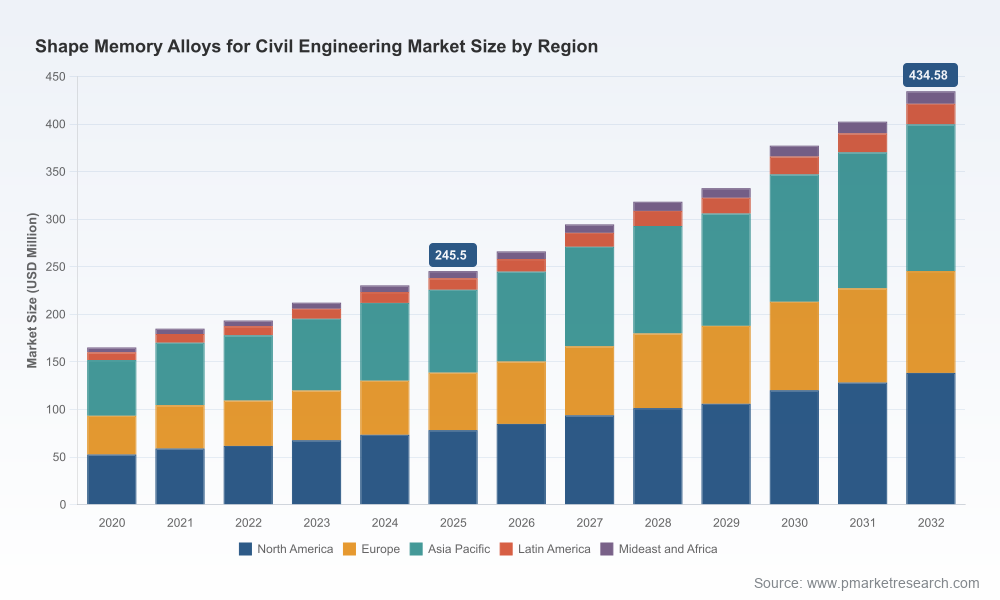

Shape memory alloys (SMAs) are moving from niche demonstrations to repeatable engineering solutions in civil infrastructure. Our new market study — base year 2025, forecasting 2026–2032 — shows a clear, investable expansion: the global SMA for civil engineering market grows from USD 245.5 Million in 2025 to an expected USD 434.6 Million by 2032, at a compound annual growth rate (CAGR) of 8.5% across the forecast horizon. For boards, infrastructure owners, and engineering firms making strategic decisions in 2026, the question is not whether SMAs will matter, but how to position procurement, R&D and execution models to capture disproportionately large value as applications scale.

Worldwide Shape Memory Alloys for Civil Engineering Market

Why 2026 is a strategic inflection point

Several interlocking dynamics elevate 2026 from pilot season to early-adoption. First, maturation of iron-based SMAs (Fe-SMA) and the practical demonstrations of heat-activated strengthening on real bridge decks are reducing implementation risk for large structural retrofits. Second, advances in actuator-grade nickel-titanium (NiTi) alloy manufacturing and vertically integrated supply capabilities are lowering the threshold for deploying SMA-based dampers, prestressing elements, and sensing/repair systems at building and bridge scale. Third, standards and test methods, including ASTM-led initiatives relevant to SMA characterization, are providing the quality framework that procurement and design teams require to specify SMAs at scale.

Worldwide Shape Memory Alloys for Civil Engineering Market

These technical and regulatory improvements coincide with continuing global drivers: aging transportation and building stock, rising interest in resilience and seismic retrofit, and growing appetite among infrastructure agencies for low-disruption refurbishment techniques. Taken together, they create a window in 2026 for strategic action: pilot-to-scale pathways will yield first-mover advantages in supply-chain control, productized retrofit services, and intellectual property around application-specific assemblies.

Worldwide Shape Memory Alloys for Civil Engineering Market

Strategic implications for 2026 decision-makers

- Prioritise demonstration-to-deployment pipelines: Fund full life-cycle pilots (design, installation, monitoring, O&M) rather than one-off lab trials. Data from in-situ performance will shorten procurement cycles and reduce insurance/framing risk.

- Adopt a multi-source procurement stance: Nickel and titanium price volatility, combined with geopolitical supply risks, means reliance on a single NiTi supplier exposes projects to margin and delivery shocks. Incorporate Fe-SMA options where appropriate to manage raw-material exposure and scale considerations.

- Engage with standards and certification bodies: Active participation in ASTM and national standards working groups translates to earlier influence over acceptance criteria — and faster approvals for pilot projects.

- Lock in service and warranties: Winning commercial advantage will be as much about guarantees and integrated services as it is about alloy chemistry. Look for suppliers that offer retrofit engineering, monitoring, and performance guarantees.

- Invest in digital twins and monitoring: Embedding sensing and post-installation analytics into SMA projects will create defensible datasets that accelerate specification acceptance and justify premium pricing for performance-based contracts.

What the PW Consulting report delivers — practical, ready-to-use intelligence

Our report is designed for executives and program leads who must convert opportunity into contracts and profitable deployments. It contains:

- Top-down and bottom-up market models that reconcile historical 2020–2025 performance with scenario-based forecasts for 2026–2032 (including sensitivity to commodity prices and adoption timelines).

- Decision-grade playbooks for procurement, pilot design, and scale-up — templates include specification checklists, risk transfer structures, and sample contract language for performance warranties.

- Vendor and technology evaluation frameworks: supplier scorecards, manufacturing-readiness assessments, and a comparative matrix of alloy families, production routes and integration complexity.

- Implementation case studies and techno-economic models that map installation cost, labour, and lifecycle benefit streams for typical retrofit and new-build use cases.

- Actionable go/no-go criteria and a six- to eighteen-month roadmap for infrastructure owners and contractors to move from pilot to first wave of deployments in 2026–2028.

To preserve strategic exclusivity and drive stakeholder engagement, the report intentionally reserves detailed segment and regional revenue splits for the full report package; the executive highlights in this release focus on directionality, drivers, and decision levers.

Competitive landscape — who matters and why

The supplier ecosystem is diverse: specialty metal manufacturers, component houses, system integrators, and application-focused engineering firms. Market concentration is moderate — the top three firms account for roughly one-third of commercial activity, with the top five nearing mid-forties — a structure that reflects both technical differentiation and rapid product innovation.

- re-fer AG (Brunnen, Switzerland): A leader in Fe-SMA structural strengthening, re-fer’s memory®-steel approach is engineered specifically for concrete and masonry retrofit — a strong strategic position for bridge and building rehabilitation programs. Their patented methods and early deployment record make them an attractive partner for owners seeking low-disruption prestressing and repair solutions.

- Ingpuls GmbH (Bochum, Germany): Offers end-to-end SMA solutions including actuators, dampers and crack-detection systems. Their vertical capability from alloy specification through assembly suits clients seeking integrated subsystems for building services (e.g., fire dampers, ventilation, shading) and vibration mitigation in tall structures.

- SMA CORES Inc. (Champaign, Illinois, USA): Focused on SMA-based structural technologies with emphasis on thermal prestressing and super-elasticity. Their technology is optimized to cut construction time and on-site labour, a selling point for contractors under schedule pressure.

- SAES Getters S.p.A. (Lainate, Italy): A high-volume NiTi producer with vertical integration from melting to components. Their scale and metallurgical breadth make them a plausible supply partner for OEMs and large integrators seeking consistent alloy performance and component supply assurance.

- Dynalloy Inc. (Irvine, California, USA) & Memry Corporation (Bethel, Connecticut, USA): Both are specialists in NiTi actuator wires and components — critical suppliers for actuation, damping, and sensing applications. Their product suites and component expertise are frequently embedded by systems integrators into engineered solutions.

Technology, regulation and supply dynamics to watch

Three dynamics will dominate procurement risk and opportunity in 2026:

- Raw-material volatility: Nickel and titanium supply constraints and price swings materially affect NiTi product economics. Procurement strategies must include commodity hedging, multi-sourcing and feasibility of substituting Fe-SMA where performance trade-offs are acceptable.

- Standards and testing: ASTM standards relevant to SMA evaluation and structural test methods are increasingly mature. Recognised test protocols reduce technical negotiation friction with owners and insurers — a prerequisite for broader procurement adoption.

- Manufacturing scale and producibility: Fe-SMA’s compatibility with conventional steelmaking equipment creates a pathway to scale that NiTi lacks today. For large infrastructure projects where volume matters, Fe-SMA can deliver cost and logistics advantages; for high-performance actuation and thin-section damping, NiTi remains superior.

Recent industry signals — why momentum is accelerating

- Early-2026 demonstrations of heat-activated Fe-SMA strengthening on bridge decks validated field viability and highlighted scalability pathways for iron-based approaches.

- Industry gatherings — including a planned international symposium on SMAs in infrastructure — are consolidating research, practice and procurement communities, shortening the time between demonstration and large-scale procurement decisions.

- Notable project-level adoptions, such as integration of memory®-steel into digitally fabricated structural components, underscore the practical synergy between digital construction methods and SMA-enabled design features.

Near-term catalysts and risk scenarios

Key catalysts for upside in our baseline forecast include accelerated public infrastructure programs that prioritise low-disruption retrofit methods, rapid standard adoption, and tier-one contractors offering SMA-enabled services. Risks that could slow adoption include prolonged nickel/titanium supply shocks, delays in certifying test methods for certain structural applications, and emergence of competitive retrofit technologies that capture owner budgets.

How PW Consulting can help in 2026

PW Consulting supports executive teams with tailored services to convert SMA market potential into profitable action:

- Custom market sizing and procurement modelling that embeds client-specific programme scale and risk appetite.

- Supplier due diligence and manufacturing readiness assessments to select partners with the right combination of metallurgy, capacity and system-integration capability.

- Pilot program design, bid packaging and performance guarantee structuring to accelerate adoption while protecting capital and schedule targets.

- Regulatory engagement planning to align pilots and specifications with ASTM and national standards, reducing approval lead times.

Conclusion — the strategic choice for 2026

By 2026, shape memory alloys will be a defined, actionable line item in many infrastructure owners’ toolkits. The market’s projected rise — from USD 245.5 Million in 2025 to USD 434.6 Million by 2032 at an 8.5% CAGR — reflects both technical maturation and growing application breadth. The immediate strategic question is not adoption per se, but how organisations will sequence investment: who pilots, who partners, and who captures the recurring service revenues that follow first-wave deployments.

PW Consulting’s full report contains the granular, transaction-ready datasets and playbooks needed to answer those questions with confidence. For access to detailed segment and regional breakdowns, company scorecards, and the scenario-based financial models that underpin our forecasts, visit the official report page and download the complete study.

For detailed analysis of this topic, please visit the official page:Worldwide Shape Memory Alloys for Civil Engineering Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com