Geostationary Earth Orbit (GEO) Satellite Payload Market Size, Share, Trends, Key Drivers, Demand and Opportunity Analysis

Other |

2026-06-02 14:15:33

PW Consulting’s latest market study on Packaging Outserts and Inserts offers an executive-grade, action‑oriented briefing designed to inform high‑stakes decisions across procurement, manufacturing, regulatory affairs, and corporate strategy in 2026. This article highlights the report’s strategic value, summarizes the macro trajectory and competitive drivers, and outlines concrete pathways executives should consider this year. In keeping with a “trailer” approach, we show the analytical depth and practical outputs of the study while preserving detailed segment breakdowns, driving readers to the full report for complete datasets and granular forecasts.

Packaging Outsert and Inserts Market

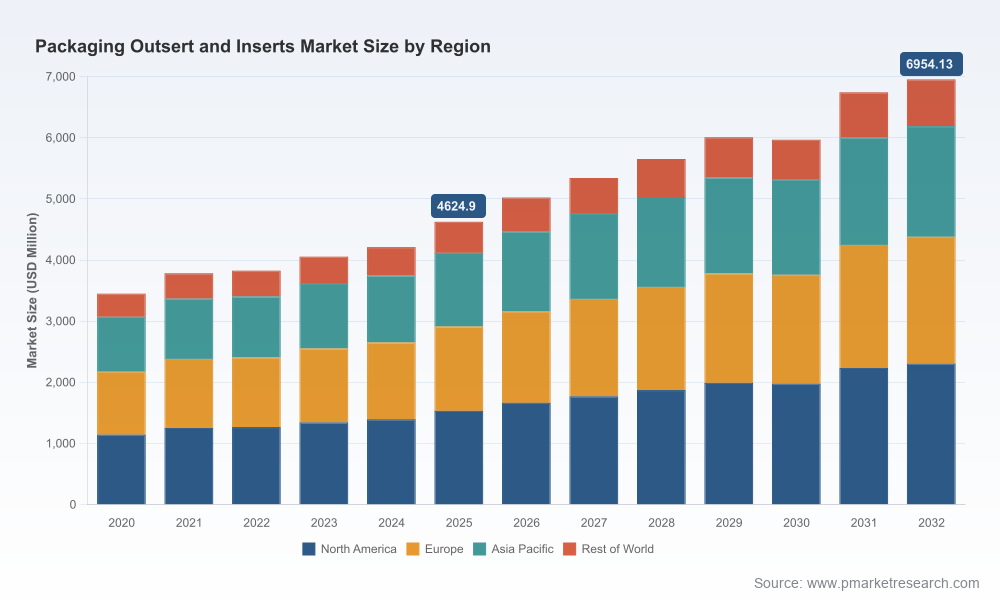

The market for packaging outserts and inserts has reached a scale that now commands boardroom attention. As of PW Consulting’s 2025 base year the market exceeded USD 4.6 billion (in Million‑USD terms) and is forecast to expand at a healthy mid‑single‑digit compound annual growth rate (CAGR 2026–2032: 6.0%), with a clear path to materially larger absolute scale by the end of the forecast window.

Packaging Outsert and Inserts Market

That growth is not uniform. It is driven by a confluence of secular forces — regulatory complexity in healthcare, expanding patient information requirements, sustainability regulation and EPR (Extended Producer Responsibility) programs, and the rising adoption of digitally printed, highly customized literature. For 2026 decision‑makers this means that the inserts and outserts category is transitioning from a low‑margin, tactical supply item to a strategic lever for regulatory compliance, patient safety, and brand differentiation.

Packaging Outsert and Inserts Market

Regulatory acceleration: New regulations and producer responsibility schemes are altering lifecycle economics for paper‑based packaging. The EU’s PPWR (Packaging and Packaging Waste Regulation) will come into force in stages beginning August 2026 and introduces design and recycled‑content obligations; several U.S. states have introduced or expanded EPR frameworks for packaging through 2025–2026. These changes shift total cost of ownership toward producers and increase the administrative burden on label and leaflet management.

Raw‑material and cost volatility: Paperboard and pulp markets are exhibiting elevated price volatility. U.S. producer price indices for folding paperboard boxes showed notable monthly movement in early 2026, while global wood pulp prices remain an input cost item that packaging buyers must actively manage. Procurement strategies in 2026 must therefore incorporate active index‑linked hedging and supplier risk sharing.

Technology and manufacturing shifts: Investment in digital printing, variable data capability, and high‑precision folding equipment is enabling shorter runs, multilingual customization, and late‑stage customization. Several tier‑1 suppliers have publicly announced capacity or technology investments designed to capture higher‑mix, lower‑volume demand patterns.

Fragmentation and specialization: Market concentration remains low relative to many other packaging subsegments — a small handful of global players coexist with a diverse set of regional specialists focused on precision folding, regulatory documentation and automation compatibility for pharmaceutical lines. This fragmentation creates opportunities for partnerships, roll‑up M&A, and selective vertical integration.

Our research is structured to be operationally useful the day it is downloaded. Key deliverables include:

Market sizing and scenario engine — base, upside and downside scenarios calibrated to regulatory shock, raw‑material stress and digital adoption curves. The engine is purpose‑built so procurement and corporate development teams can run “what‑if” cases tied to contract negotiations and M&A diligence.

Supplier scorecard and capability matrix — an independently validated evaluation framework covering GMP/compliance, digital print capability, folding precision, automation compatibility, geographic footprint, sustainability credentials and fill‑rate performance. This tool converts qualitative supplier strengths into a decision‑ready score for S2P and supplier rationalization programs.

Regulatory impact map — an implementation‑oriented taxonomy linking jurisdictional rules (including EPR and PPWR) to label/leaflet design requirements, traceability needs, and end‑of‑life obligations. Each regulatory node includes suggested compliance actions and estimated incremental cost buckets (high/medium/low) to support budgeting in 2026.

Cost sensitivity and input‑price dashboard — a modular model that quantifies margin compression across raw‑material, freight, and conversion scenarios; designed for procurement teams to evaluate contract structures (indexation, fixed‑price corridors, shared upside/downside).

Go‑to‑market & innovation playbooks — strategies for entering or expanding in pharmaceutical, medical device and consumer healthcare segments, including product architecture choices (folded outserts vs. glued booklets), late‑stage customization flows, and digital‑print proof‑of‑concept pathways.

M&A and partnership prioritization framework — a practical tool that aligns strategic intent (capability acquisition, geographic access, technology buy) with valuation heuristics and integration checklists.

The category is characterized by disciplined specialists and system suppliers. Market concentration metrics indicate a fragmented field (CR3 and CR5 values well below levels that would indicate tight oligopoly), which has three strategic implications: (1) buyers have leverage to source specialized capabilities, (2) scale advantages accrue to suppliers that combine precision folding with regulatory and digital printing capabilities, and (3) M&A remains a realistic path to consolidation and capability bundling.

Leading firms demonstrate complementary strengths that shape supplier selection strategies:

Global system suppliers with multiregional facilities provide integrated leaflet‑to‑carton solutions and are attractive to pharmaceutical customers seeking single‑vendor risk reduction and regulatory consistency.

Specialist converters focus on precision folding, ultra‑small fold formats, and complex multi‑panel outserts — capabilities critical for automated bottling lines and compliance with stringent dimensional tolerances required in biotech and Rx packaging.

Suppliers that have invested in digital printing and variable data are increasingly able to offer late‑stage language customisation, short runs, and serialization support — reducing obsolescence and enabling patient‑level information strategies.

Recent vendor actions reinforce these patterns: a North American converter announced capacity expansion in 2026 aimed at boosting blanking and die‑cut throughput; a European system supplier has expanded digital printing capacity to meet higher fidelity and shorter‑run leaflet demand; and another major vendor introduced a new component designed to integrate with pharmaceutical packaging lines, directly addressing the need for standardized, automation‑ready inserts. Taken together, these moves indicate supply‑side prioritization of capacity, digital capability and automation compatibility.

For leaders making resource allocation and sourcing decisions this year, PW Consulting recommends a prioritized, phased approach:

Immediate (0–6 months): Run a supply‑risk diagnostic against the report’s supplier scorecard; implement index‑linked clauses for paperboard inputs; establish an EPR compliance monitoring task force; pilot digital print runs for SKUs with high language or configuration variance.

Near term (6–18 months): Reconfigure supplier portfolios to reduce single‑point risks on critical folding and conversion technologies; evaluate bolt‑on M&A targets that fill capability gaps; design a sustainability roadmap aligned to anticipated PPWR and U.S. EPR requirements.

Medium term (18–36 months): Invest in modular production cells for late‑stage customization; formalize circularity programs with take‑back or recycling partners; integrate packaging‑compliance KPIs into product launch gates and regulatory submissions.

PW Consulting’s report is written to be pragmatic for multiple stakeholders:

CEOs & boards — concise scenario outputs and risk matrices for capital allocation and M&A prioritization.

Chief Procurement Officers — supplier scorecards, cost sensitivity models and contract‑language templates tailored to paper‑and‑folding markets.

Regulatory & compliance leads — the regulatory impact map with jurisdictional checklists and short‑form compliance playbooks.

Product & packaging engineers — design‑for‑compliance and manufacturability guidance, plus a decision tree for choosing digital vs. analog print and folding approaches.

2026 is a pivotal year for companies that rely on outserts and inserts. Evolving regulation, pricing volatility in key raw materials, and the accelerating commercial availability of digital production and precision folding create both risk and opportunity. Our analysis shows a market growing at an approximately 6% CAGR through the 2026–2032 forecast window, and one where strategic positioning — in procurement, manufacturing footprint, supplier partnerships and sustainability compliance — will determine margin performance and regulatory resilience.

PW Consulting’s full Packaging Outsert and Inserts Market report provides the complete datasets, regional and application breakdowns, and executable annexes that enable teams to translate these insights into procurement RFPs, capex business cases, and M&A diligence. For executives preparing budgets, negotiating supplier contracts, or shaping sustainability commitments in 2026, the report is designed to be the operational playbook that bridges market intelligence and implementable action.

To access the full report, including granular segmentation tables, interactive scenario tools, and vendor‑level assessments, please visit PW Consulting’s official report page.

For detailed analysis of this topic, please visit the official page:Packaging Outsert and Inserts Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com