Market Trends Driving Adoption of Advanced Thyroid Function Tests

Health |

2026-06-19 13:13:56

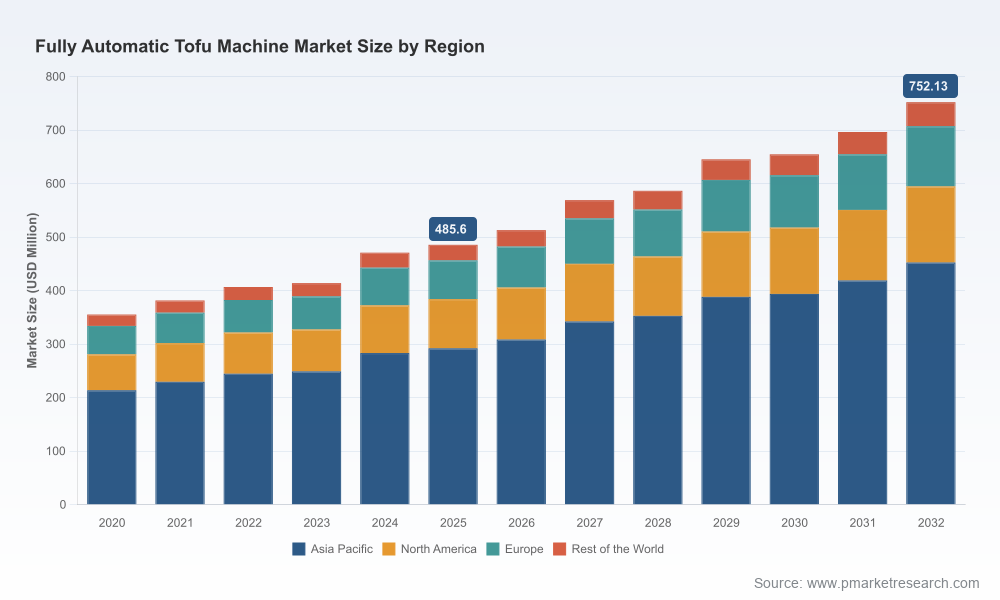

PW Consulting’s latest market research report on the Worldwide Fully Automatic Tofu Machine Market delivers an operationally focused, decision-grade perspective tailored for executives, plant managers, and investors preparing plans for 2026 and beyond. The market is poised to expand at a compound annual growth rate (CAGR) of 6.45% over the 2026–2032 forecast period. In monetary terms, the global market reached approximately USD 485.6 Million in 2025 and is forecast to grow toward the USD 750–760 Million range by 2032 under the baseline scenario. This growth trajectory is driven by a convergence of demand for plant-based proteins, rising automation to mitigate labor constraints, and incremental advances in energy- and water-efficiency in processing equipment.

Worldwide Fully Automatic Tofu Machine Market

For manufacturers, processors, and equipment investors, 2026 is an inflection year: macro demand trends remain supportive, while operational pressures (raw material cost volatility, energy, and labor) are converging to raise the premium on process efficiency, compliance, and supply flexibility. Our report is structured to help decision-makers translate market-scale forecasts into executable priorities — from plant-level return-on-investment (ROI) calculus to procurement negotiation playbooks and regulatory readiness checklists. We intentionally provide deep, methodical guidance in the report while withholding granular proprietary segment tables in this public preview to protect the competitive value of our primary research.

Worldwide Fully Automatic Tofu Machine Market

The headline CAGR (6.45%) and the market’s uplift between 2025 and 2032 quantify the opportunity — but they do not replace a layered, operational understanding required for capital allocation. Behind the aggregated growth lie three practical realities that change how capital should be deployed:

Worldwide Fully Automatic Tofu Machine Market

Our full report breaks these realities into decision-making modules: CAPEX/OPEX scenarios, break-even analyses at multiple utilization rates, and sensitivity matrices showing where price, yield, or downtime swings have the largest financial consequences.

Raw material and energy dynamics are the most immediate levers affecting tofu and soymilk processors. Notably, soybean prices have shown meaningful year-over-year increases, and contemporary forecasts for the 2025/26 marketing year indicate continued pressure on season-average prices. For operators, that means raw-material cost management must be paired with yield optimization and waste reduction strategies.

Concurrently, labor availability is trending tighter in many geographies. Fully automatic systems, by design, reduce dependence on repetitive manual tasks — soaking, grinding, coagulation, pressing — but adoption shifts the labor profile toward higher-skilled technicians and shifts where operating risk accumulates (automation control, preventive maintenance, and spare parts logistics). Companies that plan for training, remote diagnostics, and documented maintenance regimes will extract more predictable uptime and faster payback.

Vendors are increasingly emphasizing energy-efficient heating modules, integrated water-recycling circuits, and modular process skids that minimize footprint and enable phased investment. These attributes matter not only for utility costs but for brand positioning in sustainability-conscious markets and for meeting emerging regional environmental and hygiene regulations.

From an equipment selection perspective, buyers must evaluate three technical axes:

The industry exhibits moderate concentration, with top-tier suppliers collectively accounting for a meaningful, but not overwhelming, share of global revenue. Market concentration metrics (CR3 and CR5) indicate an environment where leading brands set benchmarks for high-throughput industrial lines and turnkey solutions, while a diverse set of regional and niche equipment makers serve smaller commercial and bespoke needs. This balance creates opportunities for strategic partnerships, licensing, and geographic expansion for both incumbents and new entrants.

Representative supplier profiles (covered in our report) illustrate the spectrum of propositions:

Our report contains comparative vendor matrices, procurement negotiation red flags, and supplier due-diligence checklists tailored to different buyer profiles — from multi-site processors to standalone retailers planning in-house production.

PW Consulting designed the report as an execution toolkit rather than a descriptive paper. Key operational deliverables include:

Each tool is accompanied by annotated case studies and supplier negotiation scenarios to help procurement and operations teams move from strategic intent to execution with measurable milestones.

International certifications such as ISO and CE remain gating factors for cross-border equipment deployment and for processors aiming to export finished products. The report provides a compliance readiness matrix by market cluster and offers a pragmatic checklist to accelerate conformity, reduce audit friction, and avoid last-mile modifications that delay production ramp-up.

Supplier activities through 2024–2025 show continued investment in trade-show marketing and product showcasing — a proxy for demand generation and lead pipeline building. Suppliers that invested in exhibitions and demonstration lines have increased visibility among retail chains and co-manufacturing partners. Our analysis correlates these outreach efforts with shorter sales cycles for vendors offering documented commissioning and remote-training packages.

Meanwhile, raw-material market intelligence indicates persistent soybean price volatility and a tightening inventory backdrop in certain supply geographies. For buyers, that reinforces the importance of process yield optimization, alternative coagulant evaluation, and contract procurement strategies for upstream inputs.

Our findings are grounded in a triangulated research methodology combining supplier interviews, trade-show observations, industry financials, and primary plant-level surveys conducted from 2020 through 2025, with a base year of analysis set to 2025 and a forecast horizon of 2026–2032. The report’s scenario suite models sensitivity to raw-material prices, utilization rates, and technology adoption curves and is designed for rapid customization to client-specific throughput and location assumptions.

This public preview outlines the strategic contours and operational implications of a growing global market for fully automatic tofu machines. For procurement teams, plant operators, and investors ready to convert market opportunity into operational plans, the full PW Consulting report includes the proprietary segment matrices, detailed vendor scorecards, and editable financial models required for board-level approvals and tender processes. Access to the complete dataset, annex tables, and downloadable tools is available through the report landing page.

Contact PW Consulting to request the full Worldwide Fully Automatic Tofu Machine Market report and obtain a tailored briefing that applies the report’s models to your plant layouts, sourcing footprint, and growth ambitions for 2026.

For detailed analysis of this topic, please visit the official page:Worldwide Fully Automatic Tofu Machine Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com