Cold Email Platform - Emareach: The Smarter Way to Scale B2B Email Outreach

Other |

2026-07-04 07:08:31

PW Consulting’s latest market intelligence note on the Worldwide Elapegademase-lvlr Drugs Market offers senior executives, corporate strategists, investors, and payer-affairs teams a compact but sharply actionable vantage point to orient 2026 decisions. Built on a five-year historical baseline (2020–2025) with a forward-looking 2026–2032 forecast, the study synthesizes commercial dynamics, regulatory events, and operational risks into an executable set of options — without trading the proprietary depth reserved for full subscribers.

Worldwide Elapegademase-lvlr Drugs Market

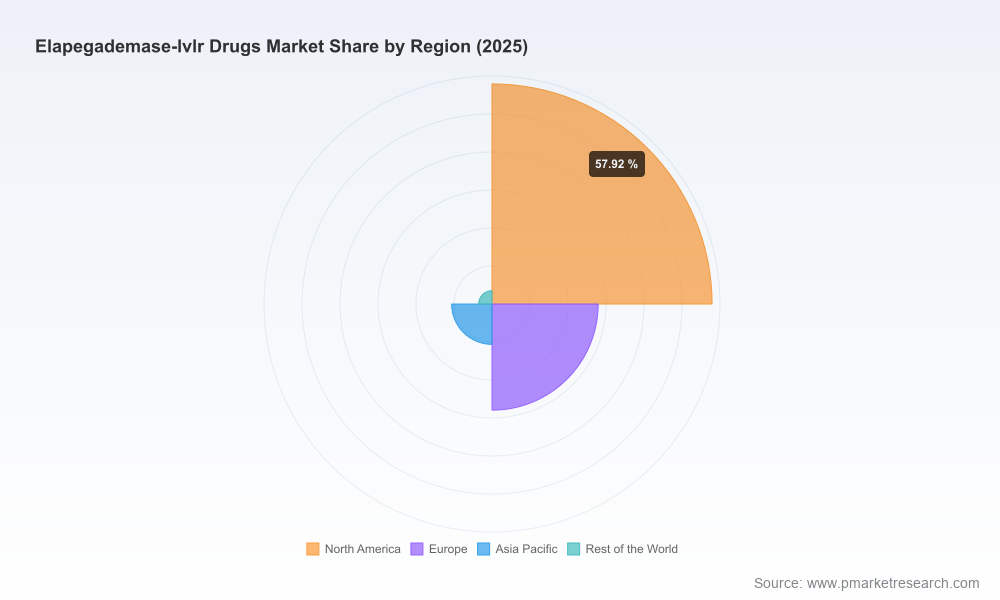

Elapegademase-lvlr (Revcovi) occupies a distinctive commercial niche as a PEGylated recombinant human adenosine deaminase enzyme replacement therapy for ADA-SCID. The market has expanded steadily through the recent historical period and, based on our modelling, transitions into the medium term with a compound annual growth rate (CAGR) of 8.5% across the 2026–2032 forecast window. In absolute terms at the report’s base year (2025) the global market is measured in the tens of millions (USD, revenue unit: Million), and our projections show a clear growth path through the end of the forecast period as treatment access, reimbursement clarity, and supply stability evolve.

Worldwide Elapegademase-lvlr Drugs Market

Importantly, competitive concentration is very high: the top three suppliers together account for the overwhelming majority of market revenues (CR3 ~98.8%), and the top five effectively saturate the market (CR5 ~100%). This concentration has direct implications for market access, bargaining leverage with payers, and the fragility of supply chains — all issues that will be central to strategic choices in 2026.

Worldwide Elapegademase-lvlr Drugs Market

Elapegademase-lvlr benefited from orphan-designation protections that shaped its early commercial runway. As we move into 2026, the changing exclusivity landscape alters the competitive calculus: potential entry pathways, lifecycle-management strategies, and medico-legal considerations need to be re-evaluated by market participants.

Documented manufacturing delays and a period of product shortage underscore a central operational risk. Firms must reconcile the dual objectives of expanding patient access while hardening supply chains against demand surges, single-source manufacturing constraints, and cold‑chain complexities.

Reimbursement frameworks — including orphan-drug reimbursement pathways under programs such as Medicare Part B in the United States — materially influence uptake and revenue realization. Payer expectations around clinical evidence, cost-effectiveness, and post-authorization data will become more exacting in 2026.

Clinical contraindications linked to PEG hypersensitivity are non-trivial for patient selection and risk management. These clinical boundaries affect market sizing, patient pathways, and the design of substitution strategies for patients who cannot tolerate PEGylated products.

The market is currently centered on a small set of established suppliers. Notably, Chiesi Farmaceutici S.p.A. markets Revcovi globally and has been the focal point for supply-chain developments in recent years. Publicly recorded events include supply interruptions and subsequent resupply actions, which illustrate how production bottlenecks by a key provider can ripple across treatment centres, specialty pharmacies, and national programs.

For potential entrants, investors, or partners, the lessons are clear: therapeutic complexity (an enzyme replacement therapy with PEGylation), concentrated incumbency, and orphan-drug economics create both barriers and windows of opportunity. Commercial entry will require careful orchestration of regulatory strategy, manufacturing fidelity, and differentiated value communication to payers and clinicians.

A validated historical series (2020–2025) and a probabilistic forecast (2026–2032) by treatment segment, distribution channel, and patient cohort — modelled in USD (Million). Note: this briefing deliberately omits the detailed cell values; the full report contains the comprehensive segmented tables and interactive charts you will need for diligence.

Market share matrices, CRx profiles, and supplier positioning benchmarks that quantify bargaining leverage and concentration risk.

Time-lined analysis of orphan exclusivity, label constraints, and conditional reimbursement mechanisms across major jurisdictions, with strategic implications for 2026 market entry and lifecycle planning.

Supplier-by-supplier vulnerability scoring, scenario-driven shortage impact models, and mitigation roadmaps (including dual-sourcing feasibility, toll-manufacturing options, and contingency inventory strategies).

Negotiation frameworks tailored to orphan therapy reimbursement channels, recommended evidence packages, and costing templates for value dossiers submission to public and private payers.

Go-to-market options for hospital pharmacy versus specialty pharmacy channels, patient support program blueprints, and launch sequencing recommendations optimized for constrained supply contexts.

Risk-adjusted patient population estimates, contraindication handling protocols (e.g., PEG hypersensitivity), and opportunities for real‑world data generation to shore up payer confidence.

Given historical shortages and the market’s concentration metrics, organizations should implement multi-layered supply strategies in 2026: secure staggered supply contracts with incumbent manufacturers, expand qualified secondary suppliers where technically feasible, and design buffer-inventory policies for critical geographies and sites of care.

With orphan-drug reimbursement pathways in play, a proactive payer engagement program that pairs value-based contracting pilots with robust RWD commitments will increase contracting success. Scenario modelling in our report helps quantify margin levers under alternative reimbursement outcomes.

As exclusivity frameworks evolve, firms should prepare modular regulatory submissions, bridge trials for manufacturing changes, and targeted label expansions. Where exclusivity limitations create windows for competition, strengthen defensible elements such as patient support services and manufacturing traceability.

Payers will increasingly demand longitudinal outcomes and comparative-effectiveness data. Investment in prospective registries, payer‑aligned end points, and burden‑of‑illness studies will materially improve access and willingness-to-pay in 2026 negotiations.

Patient support and adherence programs, coupled with tailored distribution (hospital vs specialty pharmacy), will be decisive. Our scenario work quantifies the impact of channel mixes on time-to-treatment and payer acceptance.

PEG hypersensitivity constraints require alternate care pathways and informed consent protocols; these should be embedded into provider training and reimbursement submissions to avoid treatment delays and denials.

Given the high concentration and technical complexity of the therapy, strategic partnerships (manufacturing, distribution, evidence-generation alliances) or targeted asset acquisitions may be the least risky route to expand presence without the full burden of in-house upstream scale-up.

This market brief is intended as a decision-enabling trailer: it surfaces the levers, the risks, and the high-probability scenarios that will shape value capture for elapegademase-lvlr in 2026. If you are preparing a go/no-go decision, negotiating supplier contracts, or refreshing a payer-engagement plan, the full PW Consulting report includes the quantitative tables, sensitivity analyses, and downloadable models needed to run investment-grade scenarios.

For a pragmatic first step, convene a cross-functional 90-day working group to validate: (1) supply‑continuity exposure; (2) near-term reimbursement milestones for key markets; and (3) a prioritized list of evidence-generation activities that align with payer decision timelines. Use our report’s playbooks to convert those priorities into timed deliverables and budgeted milestones.

PW Consulting’s full Worldwide Elapegademase-lvlr Drugs Market report provides the confidential segment-level tables, regional and channel breakdowns, and operative models that underpin the strategic recommendations summarized here. To access the complete dataset, interactive forecast models, and our supplier‑by‑supplier risk scoring, please visit the report’s detail page or contact your PW Consulting representative.

For detailed analysis of this topic, please visit the official page:Worldwide Elapegademase-lvlr Drugs Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com