Bubble Tea Market: Size, Share, and Future Growth

Networking |

2026-05-25 06:00:18

PW Consulting’s Whetstones Market — Whetstones Market (base year 2025) — delivers a focused, executable view of an often-overlooked specialty abrasives category. The global whetstones market reached USD 148.5 Million in 2025 and, guided by structural demand and product innovation, is forecast to grow to roughly USD 198.7 Million by 2032. Our modelling shows a compound annual growth rate of 4.25% for the 2026–2032 forecast window. For corporate leaders planning capital, product, channel, and M&A moves in 2026, this report converts market momentum into clear, prioritized choices.

Whetstones Market

Small absolute scale, disproportionate strategic impact: Whetstones are low-ticket individually, but they are critical touchpoints in premium foodservice, precision manufacturing, and specialty hobby markets — categories that drive brand loyalty and high-margin accessory sales.

Whetstones Market

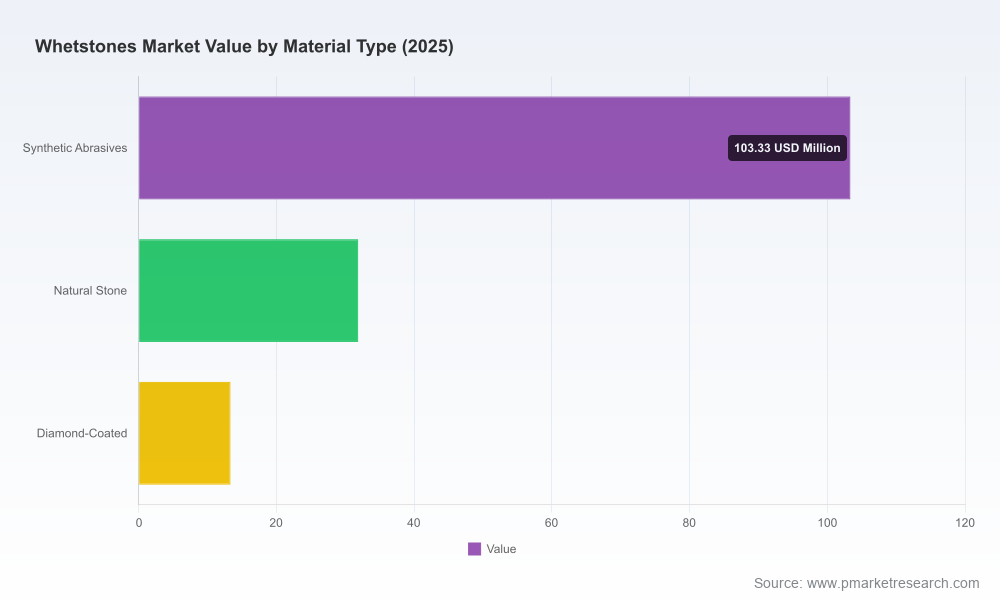

Technology and materials shift: advancements in ceramic and bonded abrasives are shifting value from commodity stones to performance-led premium offerings, creating margin expansion opportunities.

Whetstones Market

Supply and provenance risks: control of natural novaculite deposits, regulatory labeling (e.g., “Made in USA”), and raw-material sourcing are creating defensible advantages for vertically integrated producers.

Channel bifurcation: mass retail and e-commerce favor convenience and modular systems, while professional channels reward performance claims and certifications — each requires distinct go‑to‑market playbooks.

Top‑down market sizing and forward scenarios: base-year calibration (2025), historical trend analysis (2020–2025), and three demand scenarios through 2032 driven by demographic, professional, and industrial use-cases.

Value-chain and raw‑material risk mapping: quarry footprints, synthetic abrasive supply flows (aluminum oxide, silicon carbide), and contingency playbooks for constrained novaculite supplies.

Regulatory compliance and claims checklist: operational steps to substantiate country-of-origin claims and to manage FTC and export control exposures.

Go‑to‑market playbooks: differentiated strategies for direct-to-consumer premium bundles, subscription-based consumables, professional channel partnerships, and industrial OEM integration.

Competitive benchmarking toolkit: product-performance scorecards, pricing matrices, and a reproducible framework to evaluate technology partnerships and licensing opportunities.

M&A and partnership screening: proprietary criteria to identify tuck-in targets, industrial scale partners, and high-margin niche assets with defensible IP or raw‑material control.

Retail and digital activation templates: creative and performance KPIs informed by 2025–2026 media tests and product reviews in culinary and enthusiast channels.

Fragmented competitive landscape with consolidation upside. The market remains fairly fragmented — our concentration metrics indicate limited dominance by top incumbents, leaving room for targeted consolidation and roll‑ups to extract operating synergies.

Vertical integration as a defensible moat. Producers that control quarry reserves or long-term supply contracts for natural novaculite enjoy material advantages in provenance-driven premium positioning and in defending “Made in USA” claims under regulatory scrutiny.

Material innovation lifts price/worth. Ceramic and resin-bonded synthetic abrasives (notably aluminum oxide and silicon carbide formulations) are enabling faster cutting, longer-lasting surfaces, and convergence between hobbyist convenience and professional performance.

Channel polarization: convenience vs. performance. Retail and e-commerce favor “splash-and-go” or systemized solutions with strong content marketing; conversely, chefs and industrial users prioritize demonstrable edge metrics and certification.

Marketing and third‑party validation matter. Independent testing and editorial coverage in culinary media are primary demand drivers among premium consumers; notable 2026 product tests have already shifted consumer consideration sets.

Dan’s Whetstone Company — vertical integration and provenance. Owning quarry reserves and finishing operations provides a clear premium‑provenance play and protects supply. Opportunity: scale marketing to premium culinary and restoration segments while exploring licensing to expand reach without diluting origin claims.

Norton Abrasives (Saint‑Gobain) — scale and portfolio breadth. Large industrial aperture and diverse abrasive technologies enable cross‑sell into B2B and OEM channels. Vulnerability: positioning in consumer premium might be perceived as less authentic versus heritage makers; opportunity lies in leveraging R&D and distribution to offer hybrid solutions for professional users.

SHAPTON Co., Ltd. — high‑performance ceramic specialists. Strong brand equity among performance seekers and skilled markets. Advantage: premium pricing and technical differentiation. Consideration: expand consumable revenue through bundled systems and online education to convert enthusiasts.

Matsunaga (King brand) — heritage and household reach. Deep brand recognition among starter and mainstream users. Strategic path: preserve entry-level loyalty while introducing upgrade pathways to premium ceramic/diamond-coated offerings.

Work Sharp — systems and ergonomics. Value comes from system-based sharpening — attractive to DIY and workshop segments. Growth lever: integrate subscription abrasives and digital tutorials to increase lifetime value.

Specialty and niche players (Falcon, NORITAKE, Gesswein) — materials and channel specialization. These companies dominate specific value niches (ruby or precision jewelry stones, industrial abrasives supply) and are logical acquisition targets for players seeking manufacturing or channel fill‑ins.

Media testing and product reviews in 2026 are accelerating shopper conversion for specific brands and sets; editorial endorsements now move inventory in weeks rather than months.

Ongoing production and publicized quarry ownership highlight the tangible advantage of supply control for certain producers — an increasingly salient factor for premium positioning and regulatory compliance.

Secure supply and provenance: execute short-term hedges and evaluate minority stakes or offtake agreements in natural‑stone reserves to lock in premium raw material claims.

Segmented product strategy: design a two‑tier portfolio — entry systems for mass channels and a high‑performance line with traceability and certification for premium buyers and industrial customers.

Invest in demonstrable performance metrics: fund independent edge-performance testing and make standardized claims a central marketing pillar to win professional endorsements and media placements.

Explore bolt-on consolidation: target niche manufacturing or distribution assets that expand channel reach, create cross-sell opportunities, or add raw material control — capture synergies while preserving brand authenticity.

Operationalize sustainability and compliance: implement supply‑chain transparency and comply with country‑of‑origin regulations in product labeling to prevent reputational and regulatory risk.

We translate the macro trajectory and the 4.25% forecast CAGR into prioritized options that fit your risk appetite and capital bandwidth.

Engage us for a tailored “playbook sprint” (6–8 weeks) to convert the report’s hypotheses into a live implementation plan: supplier negotiations, product P&L modeling, channel pilots, and a short‑list of acquisition targets.

Our competitive due diligence combines proprietary benchmarking with on‑the‑ground material audits and independent product verification so you can make offers and go‑to‑market moves with confidence.

PW Consulting’s Whetstones Market is deliberately structured as a “trailer”: we surface the strategic levers, competitive dynamics, supply risks, and go‑to‑market options that matter for 2026 decisions while reserving the granular segmentation tables and target lists for the full report and client engagements. For executive teams planning product investment, channel shifts, or M&A activity in 2026, the full report is the operational playbook you’ll use to align board-level priorities with executable near‑term moves.

To access the full Whetstones Market report and receive a complementary briefing tailored to your company’s positioning, please contact PW Consulting or visit our Whetstones Market page to download the complete analysis and appendices.

For detailed analysis of this topic, please visit the official page:Whetstones Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com