Worldwide Heavy Truck Battery Swap Stations Market — Strategic Preview for 2026 Decision-Makers

PW Consulting presents a strategic preview of our forthcoming Worldwide Heavy Truck Battery Swap Stations Market report. As heavy-duty electrification accelerates, battery swap infrastructures are shifting from pilot projects to commercially viable networks. This preview synthesizes the report’s core insights, highlights the strategic choices facing stakeholders in 2026, and explains why the full report — with its granular models, deployment playbooks and proprietary datasets — will be essential for boards, corporate strategy teams and infrastructure investors preparing for the next wave of scale-up.

Worldwide Heavy Truck Battery Swap Stations Market

Executive snapshot: Why 2026 is a pivot year

Market momentum is clear. Our base-year analysis (2025) shows the heavy truck battery swap station market reaching approximately USD 1,250 million, up from USD 350 million in 2020. With a 2026–2032 compound annual growth rate (CAGR) of roughly 21.0%, the opportunity set expands rapidly: the market is forecast to surpass USD 1,470 million in 2026 and approach the multi-billion-dollar range by the early 2030s. These headline figures underscore an inflection point — where planning and early investments made in 2026 will determine market positioning for the next decade.

Worldwide Heavy Truck Battery Swap Stations Market

What the preview reveals (and deliberately omits)

- Revealed: macro trajectory, key industry dynamics, competitive standouts and actionable strategic recommendations targeted at OEMs, fleet operators, infrastructure developers, utilities and investors.

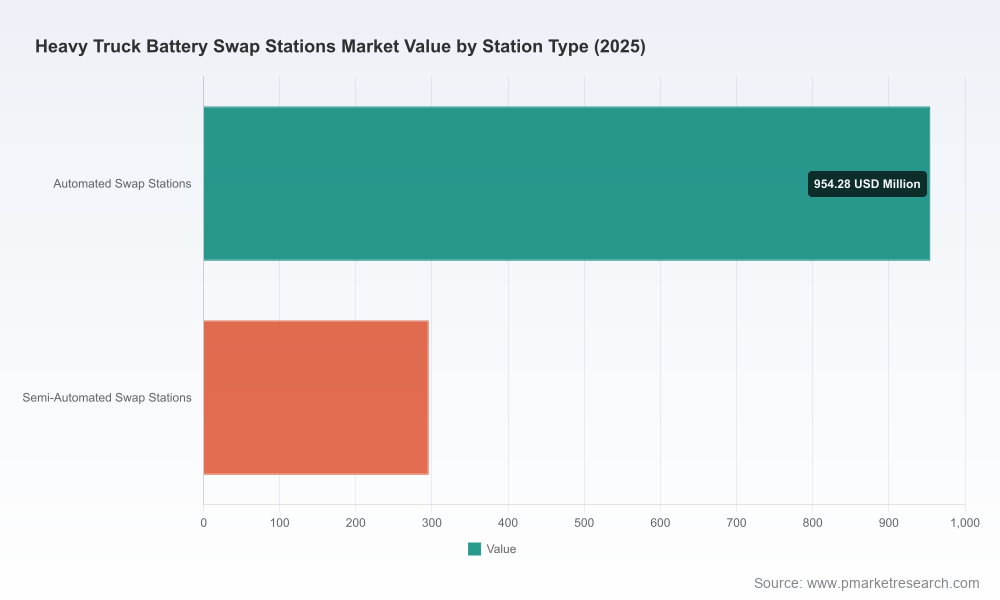

- Withheld: granular regional/application-level revenue percentages and line-item financials across station types. The full report contains the detailed segmentation, scenario-tested financial models and geospatial site-selection outputs required for deployment decisions.

Core drivers shaping demand and supply

Several converging forces are catalyzing investment and commercialization:

Worldwide Heavy Truck Battery Swap Stations Market

- Policy and standards: Recent national-level standards have clarified compatibility requirements for heavy-truck battery swapping, reducing technical ambiguity for integrators and OEMs and enabling platform-level interoperability planning.

- Fleet economics: Total cost of ownership (TCO) dynamics for long-haul and regional heavy trucks increasingly favor energy-as-a-service and swap-based uptime models, particularly where fast turnarounds and predictable duty cycles are essential.

- Infrastructure dynamics: Swap stations are capital- and grid-intensive assets. Deployers must plan for substantial site capex, significant on-site storage and high-capacity electrical connections. These infrastructure characteristics make site-selection, utility engagement and financing structures central to success.

- Technology and operations: Automated and semi-automated swap station designs are both progressing, and operators must balance automation capital against throughput, reliability and workforce requirements.

Competitive landscape — who to watch

Market concentration has already favored a small set of scale players. The top three incumbents account for a meaningful majority of the market by revenue and deployed station count, and the top five exhibit even greater combined share — an important datapoint for entrants and investors assessing competitive barriers.

Key players profiled in the full report include:

- CATL (Ningde, China) — Operator of a standardized heavy-duty swap network with stations engineered for rapid swaps of very high-capacity packs. CATL’s deployments and technical whitepapers are widely referenced across the industry for mechanical and electrical system baselines.

- Farizon Auto (Hangzhou, China) — Deploying modular, OEM-integrated swap stations that support a vehicle-first approach to network roll-out; notable for rapid network launches tied to captive fleets.

- TGOOD (Shenzhen, China) — A systems integrator delivering turnkey commercial swap stations and operations across multiple provinces, leveraging electric logistics demand corridors.

- Aulton New Energy (Wuxi, China) — Bringing bus-swap heritage to heavy-truck applications with automated battery handling solutions and a focus on turnkey deployment.

Recent validated industry developments reinforce the competitive trajectory. Examples include the commissioning of large-scale standardized swap stations, the formal release of group standards enabling cross-vendor compatibility, and localized network launches by OEM-linked players. These events reduce technological uncertainty and accelerate the shift from pilots to networked operations.

Strategic implications by stakeholder

Our scenario and sensitivity analyses in the full report translate the macro forecasts into concrete decision outcomes. High-level implications for common stakeholder groups are:

- OEMs and powertrain suppliers: Early partnerships with station operators to define battery standards and charging/swap protocols will materially reduce market access friction. OEMs should prioritize modular battery platforms compatible with standardized swap interfaces.

- Fleet operators: For fleets with high-utilization vehicles, dedicated fleet-access swap facilities can unlock uptime advantages. Fleet operators must evaluate capex vs. opex models (ownership, lease and energy-as-a-service) under multiple utilization scenarios included in the report.

- Infrastructure developers and station operators: Site selection and utility engagement are the two highest levers to optimize economics. Developers should use granular demand-mapping (available in the full report) to prioritize corridors that yield rapid payback under conservative throughput assumptions.

- Utilities and grid planners: Swap facilities require multi-MVA level connections and intelligent energy management. Utilities that proactively design tariff structures and flexible connection offers will attract developers and reduce project lead times.

- Investors and financial sponsors: The sector shows early consolidation risk and technology concentration. Investment diligence should include rigorous station-level stress tests, battery lifecycle assumptions and counterparty credit risk assessments — elements we provide in the report’s financial model templates.

Operational realities and cost structure (qualitative)

Key operational levers impact unit economics and deployment sequencing. Station capex, battery asset costs and grid upgrades represent the largest contributors to upfront investment. Governments in some markets are offering substantial local incentives to accelerate deployments, which can change payback horizons materially. From an engineering standpoint, stations require robust electrical architectures, significant thermal management for high-capacity packs and operational designs that prioritize safety and reliability during high-frequency swaps.

We deliberately avoid publishing granular cost line-items in this preview. The full report discloses our validated capex and opex models (with regional sensitivity), supplier cost curves and battery life-cycle replacement schedules — all essential for accurate ROI modeling.

Risk map and mitigation priorities

Our risk assessment identifies five clusters that will determine the winners and losers as the market scales:

- Standards fragmentation risk — mitigated via early adoption of group standards and multi-stakeholder interoperability testing.

- Grid and utility connection delays — mitigated through staged agreements with utilities and demand aggregation strategies.

- Battery asset management and second-life value risk — mitigated through warranty structures, pooled asset models and secondary market planning.

- Concentration and counterparty risk — mitigated with diversified supplier panels and contractual protections.

- Adoption timing mismatch between OEMs and infrastructure providers — mitigated by co-investment models and anchor-customer fleet partnerships.

What the PW Consulting report delivers (operationally actionable)

The full Worldwide Heavy Truck Battery Swap Stations Market report includes:

- Historical market sizing 2020–2025 and forward-looking projections for 2026–2032, with scenario-tested outcomes and sensitivity matrices.

- Segment-level analytics (station types, operation models and regional overlays) with downloadable datasets and geospatial demand maps.

- Competitive benchmarking and technology readiness assessments for key vendors and integrators.

- Site-selection framework, utility-engagement playbook and permit/timeline checklists to compress deployment schedules.

- Financial templates and unit-economics models calibrated to multiple capex/opex permutations and subsidy environments.

- Regulatory tracker summarizing applicable standards, certification pathways and compliance timelines.

- A strategic roadmap for partnerships, investment prioritization and go-to-market sequencing tailored to OEMs, fleets and financial sponsors.

How to use this preview in 2026 planning cycles

Executives developing 2026 budgets and 3–5 year strategic plans should treat the forecast trajectory and concentration signals in this preview as directional imperatives. Specifically:

- Prioritize interoperability and standards alignment in technology roadmaps to avoid stranded assets as networks interconnect.

- Lock in anchor customers and utility agreements before full network roll-out to derisk connection lead-times and secure predictable throughput.

- Structure investment vehicles that reflect asset intensity and longevity — blending concessional financing where available with commercial capital to optimize weighted-average cost of capital.

- Use the full report’s scenario models to stress-test deployment phasing under conservative utilization assumptions, then overlay upside cases for rapid adoption corridors.

Final note — why download the full report

This preview establishes the macro trajectory and strategic priorities for the heavy truck swap station opportunity, but it intentionally omits the fine-grained segmentation and station-level financials that practitioners need to execute. PW Consulting’s full report contains the proprietary datasets, deployment playbooks and template models that translate the 21% CAGR macro story into site-level decisions, partnership agreements and board-ready investment cases.

For executives planning capital allocation, partnership strategies or national roll-outs in 2026, the difference between a first-mover advantage and a costly follow-on position will hinge on access to the detailed scenario outputs and validated unit-economics models contained in the full study.

Contact and next steps

PW Consulting will release the complete Worldwide Heavy Truck Battery Swap Stations Market report with datasets, templates and a companion executive briefing. Contact your PW Consulting account lead to schedule a tailored briefing that translates the report’s findings into your organization’s strategic playbook.

For detailed analysis of this topic, please visit the official page:Worldwide Heavy Truck Battery Swap Stations Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com