Power Tools market Size, Share, Trends, Key Drivers, Demand and Opportunity Analysis

Other |

2026-05-25 13:47:32

PW Consulting’s latest market study on the Worldwide Automotive Image Signal Processor (ISP) market frames 2026 as an inflection year for automotive vision systems. The market’s trajectory from a base of USD 2,150.4 Million in 2020 to an estimated USD 3,740.6 Million in 2025 highlights sustained momentum; our forecast projects that continued innovation and vehicle electrification will drive the market to roughly USD 8,800.2 Million by 2032 at a compound annual growth rate (CAGR) of 13.01% over the 2026–2032 period. For executives weighing investment, sourcing, and product roadmaps in 2026, the report converts these headline numbers into operationally useful guidance without surrendering competitive detail in this public summary.

Worldwide Automotive Image Signal Processor Market

Technology maturation meets regulatory and commercial acceleration: Advanced Driver Assistance Systems (ADAS), zonal vehicle architectures and the proliferation of AI accelerators within domain controllers are increasing the technical scope and commercial value of ISPs. Leading CMOS image sensor introductions and ISP IP certifications are shortening integration cycles and expanding safety-critical use cases.

Worldwide Automotive Image Signal Processor Market

Supply‑chain and trade policy volatility reshapes sourcing calculus: Recent policy actions and investigations around critical minerals and advanced computing products introduce new tariff and supply risks that alter total landed cost models and supplier selection criteria.

Worldwide Automotive Image Signal Processor Market

Consolidation and concentration create differentiated supplier dynamics: The market is moderately concentrated at the top, signaling that partnerships and Tier‑1 relationships will define access to engineering roadmaps and prioritized supply allocations.

Validated market sizing and forward scenarios: We present an audited historical series (2020–2025) and three demand scenarios for 2026–2032 informed by sensor roadmaps, software commoditization rates, and OEM platform strategies.

Integration playbook for platforms and OEMs: A structured decision framework to help system architects choose between integrated ISPs, standalone ISP modules, and hybrid SoC approaches; success metrics include time-to-market, functional safety path, and software scalability.

Supplier evaluation matrix: A multi-dimensional supplier scorecard combining technical capability (pixel throughput, HDR, NPU integration), safety certifications, manufacturing resilience, and commercial flexibility to support sourcing decisions under tariff and lead‑time uncertainty.

Cost and impact modeling templates: Scenario-based cost models that incorporate potential tariffs, freight volatility, and lead-time premia — modeled to help procurement teams quantify near-term risk vs. long-term total cost of ownership.

Integration & validation playbooks for Tier‑1s and semiconductors: Practical test plans and verification paths aligned to ISO 26262 functional safety expectations and camera system SW stacks, reducing integration cycle time by design.

Commercial roadmaps for ISVs and start‑ups: Route-to-market recommendations, go-to-partner strategies, and licensing vs. supply decisions mapped to varying OEM sourcing approaches and software monetization levers.

The ISP ecosystem is characterized by a mix of traditional analog/digital suppliers, camera‑sensor leaders, and SoC vendors expanding up the stack. Our report analyzes competitive positioning across technical capability, product timing, and channel access; below are high‑level strategic takeaways drawn from company trends and recent industry events.

Sensor-to-system incumbents and their ecosystem advantage: Sensor leaders who pair high‑performance CMOS image sensors with ISP pipelines are shaping reference architectures and interface standards. High‑bandwidth interfaces and sensor-level features (e.g., A‑PHY support) reduce integration friction and enable OEMs to compress development timelines.

IP vendors and safety certification as a market differentiator: Vendors who secure ISO 26262 certifications for ISP IP are becoming preferred partners for safety‑critical ADAS programs. Certification success reduces OEM test burdens and accelerates AV validation timelines.

SoC and platform providers compress the value chain: Companies that deliver integrated SoCs with high-performance ISPs and AI accelerators drive consolidation in module design, but OEMs and Tier‑1s retain leverage through software and system integration requirements.

Regional supply strategies will matter more than ever: Given trade policy shifts and growing emphasis on on‑shore or near‑shore supply, OEMs should treat geography as a strategic lever rather than an operational afterthought.

Representative players examined include established semiconductor and vision suppliers that span ISP IP, dedicated ISP devices, companion processors, and integrated SoCs. For each firm, the report maps product capability to use case stretch (e.g., ADAS perception, surround view, in‑cab monitoring), catalogues recent product and certification milestones, and assesses commercial implications for sourcing and co‑development in 2026. The market’s top three and top five suppliers account for a material share of industry revenues — a concentration that favors strategic partnerships for access to capacity and roadmap influence.

Sensor interface modernization: The industry’s move toward standardized, high‑speed interfaces at the sensor level reduces integration costs and enables longer cable lengths and zonal architectures; this materially affects camera placement strategies on vehicles.

Safety certifications accelerate adoption in critical stacks: The recent ISO 26262 certifications for advanced ISP IP validate migration paths into safety‑relevant systems and shorten OEM qualification windows.

Trade policy and tariff actions increase near‑term cost risk: New measures impacting certain advanced computing chips and possible tariffs on processed critical minerals introduce scenarios where component landed costs spike and force near‑term sourcing rebalancing.

Supply chain cadence adjustments: Lead times for automotive semiconductors lengthened in late 2025, underscoring the importance of inventory strategy and dual‑sourcing plans for programs that ramp in 2026–2028.

For OEMs, Tier‑1 suppliers, component vendors and private equity investors, the report translates market trends into clear, prioritized actions. Key recommendations include:

Adopt a two‑track integration strategy: For near‑term programs, prioritize suppliers that can deliver proven safety artifacts and shorter integration cycles; for mid‑term platforms, architect for ISP flexibility to capture future sensor performance gains and AI functions.

Quantify tariff and material risk into bid models: Incorporate tariff scenarios and resultant cost pass‑through into sourcing contracts and pricing negotiations; evaluate near‑shoring as a hedge for strategic programs.

Prioritize suppliers with certified IP or product roadmaps aligned to ISO 26262: Certification reduces program unforeseen expenses and accelerates validation timelines — an increasingly important commercial differentiator.

Lock in multi‑tier capacity agreements: Given market concentration dynamics, secure capacity with top suppliers and build architectural redundancy through carefully assessed second‑source partners.

Embed software portability and OTA readiness: ISPs are increasingly defined as much by their software pipelines as by raw pixel throughput; require vendors to deliver software abstraction layers that support OTA updates and feature differentiation.

0–90 days: Run a supplier rapid‑assessment using our scorecard to align current program needs with vendor certifications and lead‑time realities; update RFQ templates to include tariff and certification clauses.

3–6 months: Negotiate conditional allocation or priority capacity agreements with primary suppliers; begin parallel integration proofs for both integrated SoC and standalone ISP options on a representative vehicle platform.

6–18 months: Complete ISO‑aligned validation and functional safety documentation; finalize architecture choice for next platform and lock in multi‑year commercial terms with risk‑sharing milestones tied to certification and supply performance.

PW Consulting’s report turns a broad narrative of rapid technical change and policy uncertainty into a practical set of actions and tools you can apply immediately. The study’s integrated approach — combining market-sizing, risk modeling, supplier scorecards, and validation playbooks — delivers both the quantitative foundation and the qualitative judgment necessary to make defensible capital allocation and sourcing decisions in 2026.

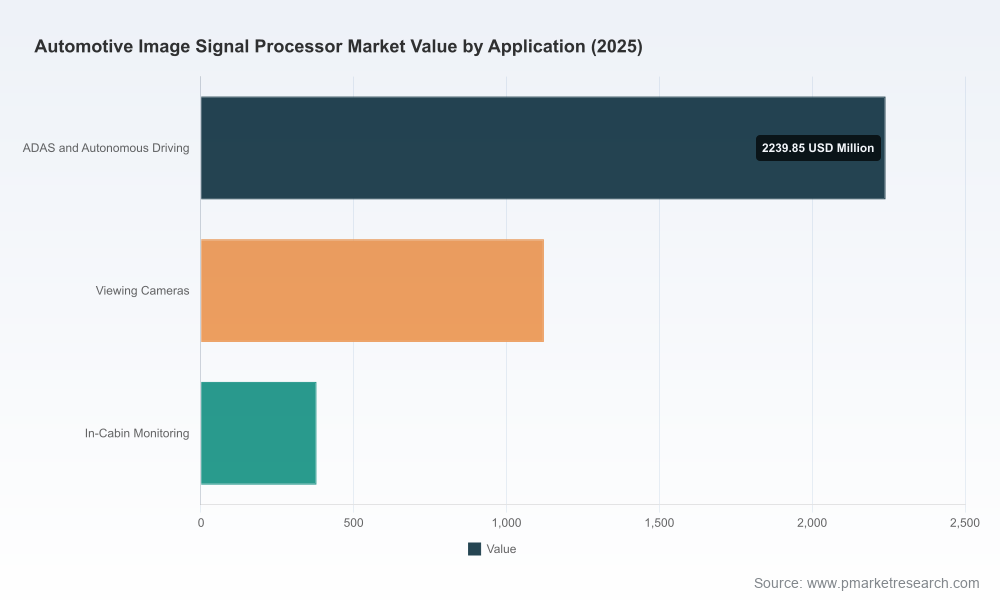

Note: This public summary intentionally highlights macro trends, key dynamics, and strategic recommendations to establish the report’s depth. Detailed sub‑segment performance, regional and application breakdowns, proprietary supplier scoring, and the full set of scenario models are available exclusively in the full report and interactive dataset. Those elements contain the granular inputs and sensitivities your product, procurement, and M&A teams will use to finalize 2026 budgets and program bids.

To access the complete dataset, vendor scorecards, and custom scenario modeling tools that underpin these conclusions, please visit the PW Consulting report landing page for the Worldwide Automotive Image Signal Processor Market or contact our advisory team for a briefing tailored to your program needs.

For detailed analysis of this topic, please visit the official page:Worldwide Automotive Image Signal Processor Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com