Breaking: Hydropower Plant Equipment Repair Market Set for Steady Growth

Other |

2026-06-26 07:41:35

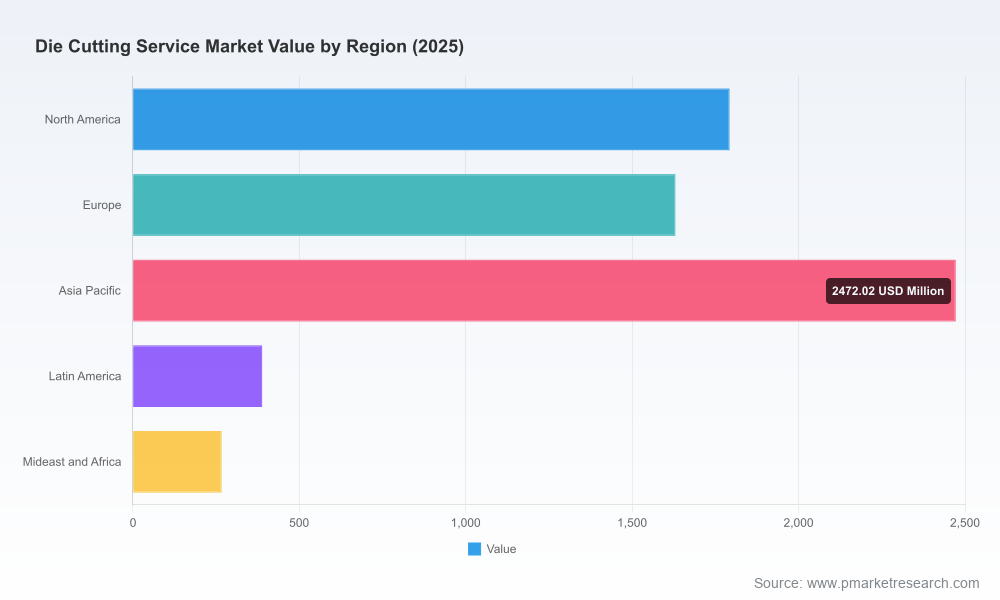

PW Consulting today publishes its authoritative market briefing accompanying the full Worldwide Die Cutting Service Market report (base year 2025, forecast period 2026–2032). The die cutting services sector — spanning converting, board and film cutting, and precision component trimming across packaging, medical, electronics and industrial applications — is entering a phase of measured expansion and structural realignment. Our base-year market model values the industry in 2025 and projects steady growth through 2032 at a 4.85% CAGR, reaching a materially larger market by the end of the forecast horizon. For executives planning capex, M&A, or supply-chain strategies in 2026, this release summarizes the strategic implications and the practical tools included in the full study to guide high-confidence decisions.

Worldwide Die Cutting Service Market

Stabilizing but persistent raw-material pressure. Paperboard and corrugated feedstocks have continued to reflect regional cost volatility, with input-cost dynamics contributing to both margin pressure and opportunity for converters that can lock-in favorable sourcing or improve material yield through precision die engineering.

Worldwide Die Cutting Service Market

Regulatory acceleration. Extended Producer Responsibility (EPR) programs are moving from proposal to implementation in multiple U.S. states and international markets. These policy shifts increase demand for design-for-recyclability, which directly affects substrate choices, die design specifications, and post-processing requirements.

Worldwide Die Cutting Service Market

Technology convergence. Equipment suppliers and converters are advancing automation, quick-change tooling and integrated digital platforms, altering the economics of short-run, high-mix production and enabling premium services (e.g., high-precision complex cuts, multi-layer laminates, and integrated flexo/converting lines).

Market trajectory: The sector is forecast to grow at a mid-single-digit CAGR over 2026–2032. This pace supports both organic capacity expansion and targeted consolidation strategies, while leaving room for specialist niche players to capture outsized margins.

Fragmentation remains high: Concentration metrics indicate that the top three and top five providers account for a modest share of total revenues, underscoring opportunities for roll-up strategies and regional consolidators to build scale.

Service differentiation is shifting from commodity pricing to engineered outcomes: Customers increasingly reward providers that combine die design expertise, quick-change capabilities, waste minimization and validated sustainability claims.

Proprietary market-size model and scenario generator — base-year calibrated to 2025 and extended through 2032 with alternate demand paths (high sustainability uptake, raw-material shock, and accelerated automation adoption). The model is provided in a downloadable, client-editable format so teams can stress-test assumptions against their own order books and supplier contracts.

Buy-side playbook — CAPEX/OPEX threshold analysis for equipment purchases (rotary, flatbed, laser) and a prioritized investment roadmap by production profile (high-volume board conversion, short-run premium packaging, specialty components).

M&A and partnership architecture — target screening criteria for roll-ups, JV structures for nearshoring, earn-out constructs aligned to throughput and quality KPIs, and an integration checklist focused on tooling libraries and changeover capabilities.

Supplier and technology heatmaps — evaluation grids for equipment vendors, tooling specialists, and digital-platform partners that include time-to-value and payback windows under multiple cost scenarios.

Regulatory impact assessment — granular timelines and compliance risk matrices for EPR and recycling mandates to support product-design and procurement decisions across North America and leading export markets.

Commercial playbooks — pricing architecture, contracting clauses to mitigate raw-material price pass-through, and go-to-market strategies to penetrate high-margin end uses without compromising capacity utilization.

The die cutting services market is characterized by a broad mix of specialized converters, global packaging groups, and equipment suppliers. Key profiles and strategic moves we examine in the report include:

Colvin-Friedman Company (United States) — A multi-decade provider of precision custom die cutting across diverse materials, leveraging material versatility and long-standing customer relationships to protect niche pricing.

Mills Industries (United States) — Focused on corrugated and protective solutions, Mills demonstrates how vertical expertise in inserts, dunnage and protective die-cut components can sustain margin resilience in periods of pricing pressure.

LMI Packaging (United States) — Concentrated on lids and labels where tight tolerances and quality control translate into repeatable commercial contracts with major CPG customers.

Janco, Inc. and MCL Industries — These providers showcase integrated capabilities across rotary, flatbed and steel-rule methods, offering turnkey converting solutions tailored to high-volume manufacturing.

DS Smith, Mondi and Smurfit Westrock — Major corrugated and carton providers are investing in advanced die-cutting lines and integrated converting to capture value higher up the packaging stack, supporting speed-to-market and sustainability claims.

BOBST, MM Packaging and specialist tooling suppliers — Equipment and tooling innovators are delivering faster changeovers, higher throughput and digital process controls — features that increasingly define competitive differentiation.

Notable recent industry developments underscore these dynamics: a leading corrugated converter made a significant capital investment in an advanced rotary die-cutting line in 2026, expanding precision capacity and reducing waste; a machinery group completed a strategic acquisition of a converting technologies firm in 2025 to broaden its rotary die-cutting and rewinding offering; and a major equipment manufacturer launched a next-generation flatbed die-cutter platform at a global trade show in 2025, emphasizing speed, quick-change tooling and digital performance monitoring. Each move signals the market’s twin focus on capacity scale and higher-value precision services.

Prioritize flexibility over single-dimensional scale. Given projected mid-single-digit growth, investments that enable rapid product changeover, multi-material handling and integrated quality validation deliver better risk-adjusted returns than commodity-volume bets.

Embed material-cost hedging into contract design. With feedstock costs remaining volatile, include indexed pass-throughs, minimum commitment corridors and collaborative waste-reduction incentives in long-term supply agreements.

Target bolt-on acquisitions and partnerships. Fragmentation creates attractive targets for regional consolidators; prioritize assets that add tooling libraries, quick-change capabilities or specialized clean-room die-cutting for medical applications.

Operationalize sustainability into product design and commercial terms. EPR developments in several U.S. states and similar policies globally mean early movers who can demonstrate recycled-content claims and closed-loop solutions will gain preferential access to large CPG customers.

Use digital twins and scenario modeling. Before committing to capital-intensive equipment, run demand scenarios using the report’s model to identify occupancy thresholds and breakeven horizons under different price and demand shocks.

The full report is designed as a working tool for boards, corporate strategy teams, private equity investors and operations leaders. It translates the latest market data and regulatory developments into executable initiatives with measurable KPIs and financial templates. We intentionally calibrate headline metrics in this release to convey macro momentum while preserving the full, granular segmentation, proprietary vendor scoring and deal-level comparables for authenticated report subscribers.

Executive teams seeking transaction support, capex prioritization or tailored market-entry analysis can license the full dataset and model from PW Consulting. The complete report includes downloadable scenario models, vendor heatmaps, an M&A playbook and a regulatory-compliance calendar tied to EPR timelines.

To schedule a briefing or request a sample chapter, visit PW Consulting’s report page or contact our strategy desk for a customized consultation. Our team will walk through the report’s scenario outputs and translate them into a 90-day action plan aligned to your commercial objectives.

PW Consulting’s Worldwide Die Cutting Service Market study is intended to be the strategic reference for 2026 planning cycles, helping leaders convert market visibility into decisive action while preserving optionality as the sector continues to evolve.

For detailed analysis of this topic, please visit the official page:Worldwide Die Cutting Service Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com