Worldwide Pigment-grade Titanium Dioxide Market — Strategic Outlook for 2026 Decision-Makers

Executive teaser

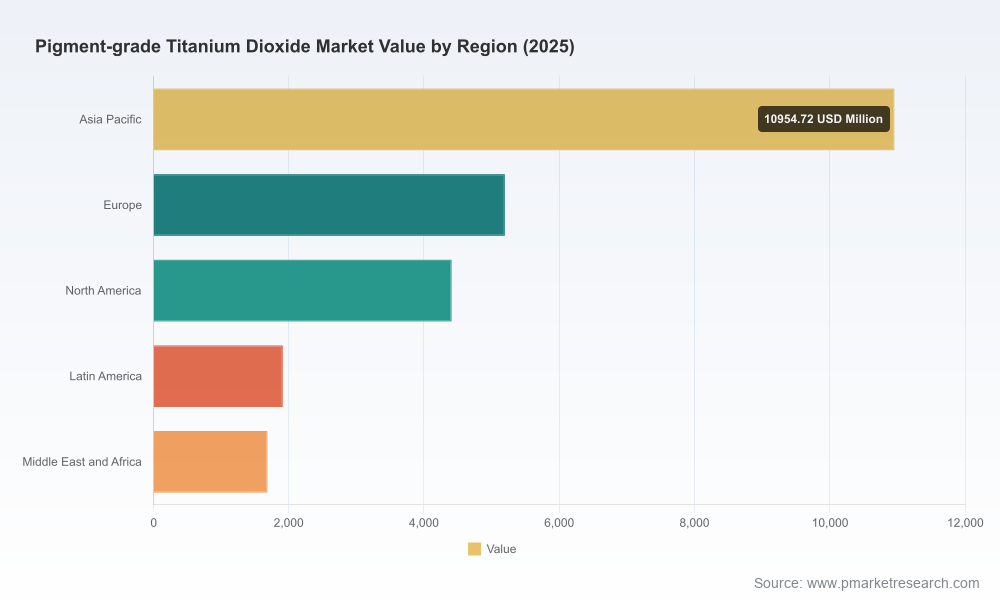

PW Consulting’s new market study on the worldwide pigment‑grade titanium dioxide (TiO2) market, anchored on a 2025 base year and covering 2026–2032 forecasts, is designed as a decision‑grade toolkit for executives preparing strategy in 2026. The market is projected to expand from an estimated USD 24,157.8 Million in 2025 to roughly USD 32,914.2 Million by 2032, at a compound annual growth rate (CAGR) of 4.52%. This briefing highlights the report’s high‑value takeaways and the strategic imperatives we believe boards, CFOs and commercial leaders must internalize—while reserving the detailed segment-level matrices for purchasers of the full report.

Worldwide Pigment-grade Titanium Dioxide Market

Why 2026 is a pivotal year

- Demand momentum vs. supply reshaping: After a recovery period in 2021–2025, the market enters a phase where modest volume growth meets meaningful structural change on the supply side. The result is a tighter margin environment for undifferentiated product and premium opportunities for specialty grades.

- Cost inflation and raw-material pressure: Ilmenite and other feedstock markets tightened in late 2024, causing double‑digit percentage increases in input cost in many sourcing basins. Energy and electricity surcharges have also risen materially, compressing margins where producers cannot pass through costs.

- Regulatory and trade friction: Recent regulatory moves—most notably China’s enforcement actions against older sulfate-process capacity and updated REACH restrictions in the EU—combined with standing trade measures such as US Section 301 tariffs, mean that access to supply and compliance costs will be core determinants of near‑term competitiveness.

- Selective capacity additions and logistics risks: Targeted capacity expansions by major players and episodic force majeure events continue to create regional shortages and price volatility. These trends make 2026 a year for active supply‑chain repositioning rather than passive purchasing.

What the PW Consulting report delivers (practical toolkit)

- Transparent market architecture: A reconciled market size and demand model (2020–2025 historical; 2026–2032 base-case and alternate scenarios) with unit and value flows that can be interrogated by users.

- Scenario-based supply-demand analytics: Four scenarios (base, constrained supply, rapid premiumization, and low-growth cost shock) that link policy, raw material and energy variables to pricing and availability outcomes.

- Cost‑of‑supply curves and process comparison: Comparative economics for sulfate vs. chloride routes, including sensitivity to ore, sulfuric acid and power costs—presented as decision levers rather than proprietary price tables.

- Commercial playbooks and pricing frameworks: Actionable templates for dynamic pricing, indexation clauses, and commercial contingency playbooks for downstream buyers and distributors.

- Regulatory and compliance matrix: Impact assessment for key jurisdictional changes (EU REACH updates, Chinese capacity rationalization, US trade policy), and step‑by‑step compliance pathways that save time and capital for product registration and market access.

- Supplier benchmarking and M&A screeners: Qualitative and quantitative dossiers on leading producers (technology mix, geographic footprints, product positioning, strategic moves), together with an M&A heat map to identify attractive targets by capability and risk profile.

- Interactive models and board decks: Editable Excel models and a ready-to-use board presentation that translate scenarios into balance‑sheet and free‑cash‑flow impacts for 2026 planning cycles.

Data-driven highlights (select, non‑proprietary)

- Market trajectory: Our modelling shows steady growth through the forecast period, underpinned by underlying end‑market demand in coatings, plastics and specialty applications; growth is sufficient to absorb rational, targeted capacity additions but not to eliminate price sensitivity for commodity grades.

- Concentration and competitive tension: The market exhibits moderate concentration—our CR3 and CR5 indicators signal that a small cohort of global players retain decisive influence on supply and price dynamics, but openings remain for regional and specialty challengers.

- Cost and price drivers: Energy and feedstock swings dominate short‑term margins; producers using more energy‑intensive routes face larger exposure to electricity surcharges and carbon‑related costs unless they accelerate mitigation measures.

Competitive landscape — what to watch (teaser)

The full report contains in‑depth profiles of the industry’s key producers and how their strategic choices shape market outcomes. Below are high‑level characterizations of the leading players and recent moves that will matter to 2026 planning:

Worldwide Pigment-grade Titanium Dioxide Market

- The Chemours Company (Wilmington, DE, USA) — A globally recognized brand focused on paint and water‑based coatings segments; recent launches of new grades optimized for modern coatings systems reflect a premiumization push and an effort to secure differentiated margin.

- Tronox Holdings plc (Stamford, CT, USA) — A major chloride‑process manufacturer that has been selectively expanding capacity; recent plant expansions highlight its strategy of scale in chosen geographies to serve coatings and plastics with chloride‑route advantages.

- Venator Materials PLC (London, UK) and Kronos Worldwide, Inc. (Dallas, TX, USA) — Players focused on performance pigments and industrial end uses, pursuing product innovation and targeted commercial partnerships rather than broad low‑cost volume plays.

- Large Chinese producers (e.g., Lomon Billions, CNNC Hua Yuan, Pangang Group) — These players combine scale with increasingly export‑oriented strategies, but are also navigating domestic policy actions that have forced closures of older sulfate capacity and prompted price adjustments in late 2024.

- Specialists from Japan and Europe (e.g., Ishihara Sangyo Kaisha, Tayca, Precheza) — Niche, high‑purity and specialty product portfolios, often insulated from commodity price cycles but exposed to OEM specification dynamics in automotive and high‑end coatings.

Recent headline events—global price adjustments by large Chinese suppliers, force majeure declarations at specific plants, targeted capacity additions in Africa, and new premium product launches—serve as early indicators of strategic direction for both suppliers and buyers.

Worldwide Pigment-grade Titanium Dioxide Market

Scenarios and strategic plays for 2026

- Integrated producers: Prioritize margin protection via premiumization—invest in grades optimized for waterborne coatings and plastics, and accelerate energy efficiency or fuel switching to reduce surcharge exposure.

- Specialty producers: Double down on R&D that ties TiO2 performance to system‑level benefits (e.g., dispersibility, opacity efficiency) and lock OEM qualification windows to create stickier demand.

- Downstream manufacturers and converters: Diversify supplier base across process routes and geographies, renegotiate indexing clauses to balance cost pass‑through, and consider dual‑sourcing longer lead‑time specialty grades.

- Buyers and procurement teams: Implement rolling 12‑month hedging and flexible contracting, stress‑test supply chains under the four scenarios in our model, and build trigger‑based contingency plans for force majeure or tariff shocks.

- Investors and M&A teams: Use our M&A heat map to prioritize targets that add premium capacity, value‑chain adjacency (e.g., surface treatment capabilities), or geographic access to growth markets with acceptable regulatory risk.

Implications for procurement, investment and risk management

- Price discipline and transparency: Buyers should move from single‑price negotiations to value‑based frameworks that reward formulaic performance gains (e.g., opacity per unit, dosing efficiency).

- CapEx prioritization: Producers must choose between brownfield debottlenecking, targeted chloride additions, and decarbonization projects; our scenario NPV models show which combinations preserve EBITDA under stress.

- Regulatory playbook: Companies must accelerate compliance workstreams (REACH, export controls) and treat regulatory change as a strategic hedge rather than a compliance afterthought.

- Supply‑chain resilience: Near‑term tactics include inventory rebalancing, long‑term offtake agreements with flexible take-or-pay terms, and closer collaboration with feedstock suppliers to mitigate ilmenite volatility.

How boards and executive teams should use the report

- Frame 2026 planning conversations around the four scenarios provided, and require commercial, procurement and capital allocation plans to pass scenario stress tests.

- Adopt the report’s interactive models in CFO planning cycles to quantify the profit impact of different process mixes, tariff exposures and regulatory compliance timelines.

- Use the supplier benchmarking and playbooks to redefine KPIs for procurement: not only price and lead time but qualification depth, product innovation pipeline and regulatory compliance scores.

Final note — the value proposition

This report is intentionally diagnostic and prescriptive: it reveals where value will be created or destroyed in the TiO2 value chain between 2026 and 2032, but it stops short of publishing the full split tables and proprietary supplier matrices that are the real operational leverage for incumbents and challengers. That curated discretion is purposeful—our aim is to give readers enough analytical depth to act, while encouraging hands‑on use of the proprietary models and supplier dossiers included in the full report.

Next steps

- For C‑suite teams preparing 2026 budgets: obtain the full report and Excel models to convert scenarios into capex and working‑capital commitments.

- For procurement and commercial leaders: use the pricing frameworks and supplier scorecards to renegotiate contracts expiring in 2026–2027.

- For investors and strategists: request the M&A heat map and target dossiers to identify immediate acquisition and partnership opportunities.

To download the full study, access the interactive models and receive the supplier‑level benchmarking that supports board‑ready decisions, please visit PW Consulting’s report page for the Worldwide Pigment‑grade Titanium Dioxide Market.

For detailed analysis of this topic, please visit the official page:Worldwide Pigment-grade Titanium Dioxide Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com