Clearcoat Automotive Performance in Modern Multilayer Systems

Networking |

2026-02-02 07:09:02

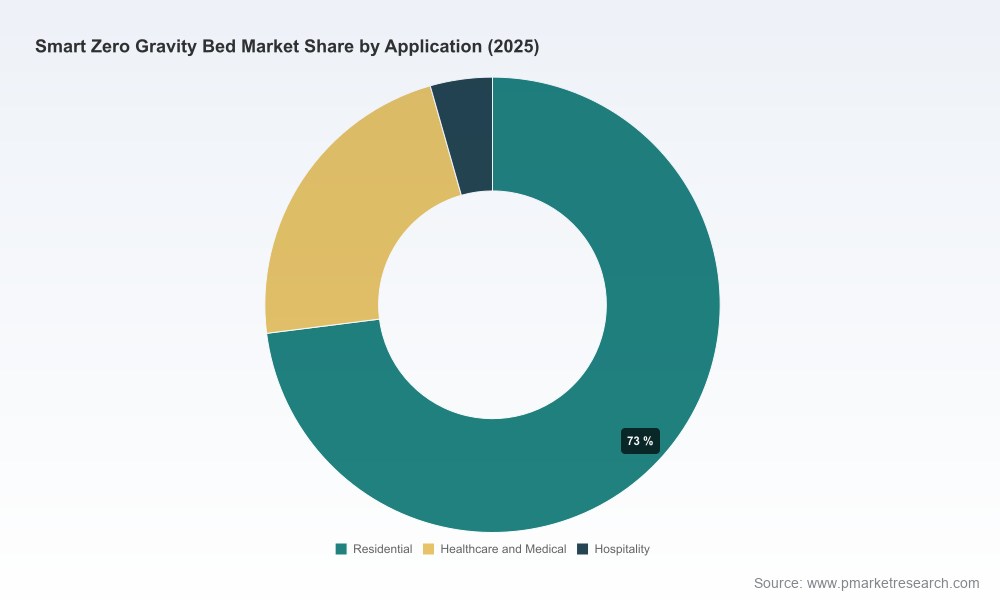

PW Consulting’s latest market intelligence on the Worldwide Smart Zero Gravity Bed Market serves as a near‑term strategic guide for executives planning investments, partnerships, and new product programs in 2026. Built on a base year of 2025 and projecting across 2026–2032, the study combines proprietary market-sizing, competitive forensics, regulatory mapping and scenario modeling. The headline economics are unambiguous: the market is on a sustained expansion path with a compound annual growth rate of 11.85% and a trajectory that moves from a mid‑market valuation in 2025 to a near doubling by the end of the forecast window. This briefing highlights the report’s value to decision‑makers while preserving the granular datasets and proprietary segment outputs for report subscribers.

Worldwide Smart Zero Gravity Bed Market

Capital allocation clarity: The report translates growth rates into investable hypotheses—where to scale manufacturing, where to defer, and where to consolidate through M&A.

Worldwide Smart Zero Gravity Bed Market

Regulatory and reimbursement playbook: We map the practical steps to optimize Medicare and private payer coverage pathways, a critical lever for commercial adoption in home‑based and clinical channels.

Worldwide Smart Zero Gravity Bed Market

Channel and partner prioritization: Evidence‑backed recommendations for whether to pursue retail, direct‑to‑consumer subscriptions, institutional tendering or hybrid models.

Product and technology roadmap: Actionable guidance on embedding sensor suites, sleep analytics, and software monetization into zero‑gravity platforms without undermining medical compliance.

Risk‑adjusted scenario planning: Multi‑scenario P&L and cash‑flow models that stress test supply chain, tariff, and reimbursement shocks for 2026 planning cycles.

Market sizing and growth mapping (historical 2020–2025; forecast 2026–2032) with top‑line checks and sensitivity bands to support capex and revenue targets.

Channel economics and route‑to‑market playbooks covering retail OEMs, mattress integrators, hospital procurement, and home‑health vendors.

Competitive benchmarking and capability maps for design, manufacturing scale, software integration, and go‑to‑market execution.

Regulatory & reimbursement dossier including CMS coding implications, documentation workflows, and evidence requirements to accelerate durable medical equipment approvals.

Supply‑chain & sourcing analysis with supplier risk scores, lead‑time stress tests, and near‑shoring opportunity matrices.

Commercial playbooks—pricing architecture, aftercare subscriptions, service margins and bundled offerings tailored for consumer and institutional buyers.

M&A and partnership screening tools including target profiles, integration risk checklists and five‑year accretion scenarios.

Two structural drivers underpin the market’s strong CAGR: an aging population with rising demand for home‑based clinical functionality and rapid adoption of smart sensors and connected sleep systems that add recurring revenue potential. Equally important are payer and regulatory dynamics. In the U.S., Medicare Part B continues to provide coverage pathways for hospital beds prescribed as durable medical equipment when medical necessity is met—this is operationalized through HCPCS coding such as the total‑electric bed categories. The policy remains explicit about documentation and face‑to‑face practitioner assessments prior to ordering, and recent clarifications (2025–2026) reiterate medical necessity criteria tied to positioning and functional limitations.

Market structure today shows moderate concentration: leading manufacturers and system integrators capture a meaningful share of the addressable opportunity, but there remains room for specialist entrants and regional champions. That mix creates both scale advantages and tactical vulnerabilities—scale in manufacturing and distribution; vulnerability in legacy product design and slow digital monetization.

SonderCare (London, Ontario) — Positions itself at the premium home‑hospital segment with therapeutic positioning suites (Zero Gravity, Trendelenburg, Comfort Chair, Boost). Their strength is clinical positioning and care‑centred features that appeal to long‑term care and post‑op markets.

Ergomotion (Santa Barbara, CA) — A global leader in adjustable bases and high‑volume manufacturing for smart beds. Their long track record, retailer relationships and platform engineering make them a natural partner for mattress brands and large retailers. Notably, Ergomotion marked its 20th anniversary in October 2025 with a refreshed design showroom, signaling continued commitment to design and channel engagement.

Leggett & Platt (U.S.) — As the largest U.S. manufacturer of adjustable bases, they bring scale, distribution breadth and a dual consumer/medical playbook. Their capabilities include programmable positions, wall‑hugger designs and embedded massage/comfort features—advantages in both retail and institutional tenders.

Tempur‑Pedic (U.S.) — Competes at the premium consumer end by integrating zero‑gravity presets with sleep‑tracking AI and mattress systems. Their differentiator is software‑driven value extraction and brand strength in sleep health.

Hebei Chibang Medical Equipment (Hengshui, China) — Focused on electric hospital beds and medical features; their cost and manufacturing profile suits institutional procurement and export markets.

Zero‑G Beds (ZERO‑G BEDS LLP / D4 Surgicals) (Mumbai, India) — Regional manufacturer serving homecare and hospital segments with medical‑grade features and competitive price points for emerging markets.

For market entrants and incumbents alike, the competitive playbook is bifurcating: one axis is premium integrated systems (hardware + sensors + analytics + brand), and the other is scale‑driven modular platforms for institutional buyers. Companies that can span both—by combining a strong R&D pipeline with channel depth—will outpace peers.

Prioritize reimbursement engineering: Build or acquire clinical evidence packages and administrative workflows that reduce friction for Medicare and private payers. Winning coverage often becomes a market share multiplier in homecare segments.

Product modularity and software-first thinking: Design platforms with replaceable sensor modules and OTA update capabilities. This lowers upgrade costs and enables subscription services—sleep coaching, predictive maintenance and clinical alerts.

Channel segmentation with clear GTM plays: Separate playbooks for consumer retail, premium D2C, and institutional procurement. Each requires different sales KPIs, pilot durations and warranty/service economics.

Manufacturing agility & dual sourcing: Implement short‑run flexibility and secondary suppliers for critical components (actuators, motor assemblies, control boards) to manage lead‑time volatility and tariff exposures.

M&A: tuck‑in and capability buys: Target acquisitions that fill specific capability gaps—clinical evidence firms, sensor/software boutiques, or regionally dominant distributors—to accelerate market entry without lengthy organic ramp‑up.

Value pricing and bundling: Test subscription models that bundle hardware, monitoring and home‑care services; structure revenue recognition and margin waterfall to demonstrate predictable, recurring revenue to investors.

Custom scenario modeling and cash‑flow stress tests tied to your product roadmaps and channel plans.

M&A target screening and diligence playbooks focused on technology, regulatory fit and cultural integration risk.

Commercial pilots: design, KPI definition and rapid‑cycle A/B testing templates for pricing and subscription bundles.

Regulatory & reimbursement fast‑tracks: payer engagement templates, clinical evidence roadmaps and documentation packages aligned to HCPCS pathways.

Supply‑chain resilience programs: dual‑sourcing strategies, near‑shoring opportunity assessments and inventory optimization models.

PW Consulting’s report is expressly built to convert market forecasts into executable plans for 2026. We provide the analytical spine—top‑line market sizing, growth rates and concentration metrics—together with the tactical toolkits required to act. The full report contains the proprietary segment matrices, dealer and supplier lists, and appendices that underpin the conclusions summarized here. To access the complete dataset, granular segmentation, and downloadable scenario models, please visit the official report page.

For detailed analysis of this topic, please visit the official page:Worldwide Smart Zero Gravity Bed Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com