Worldwide Embedded System Market 2026 Strategic Preview — A PW Consulting Intelligence Brief

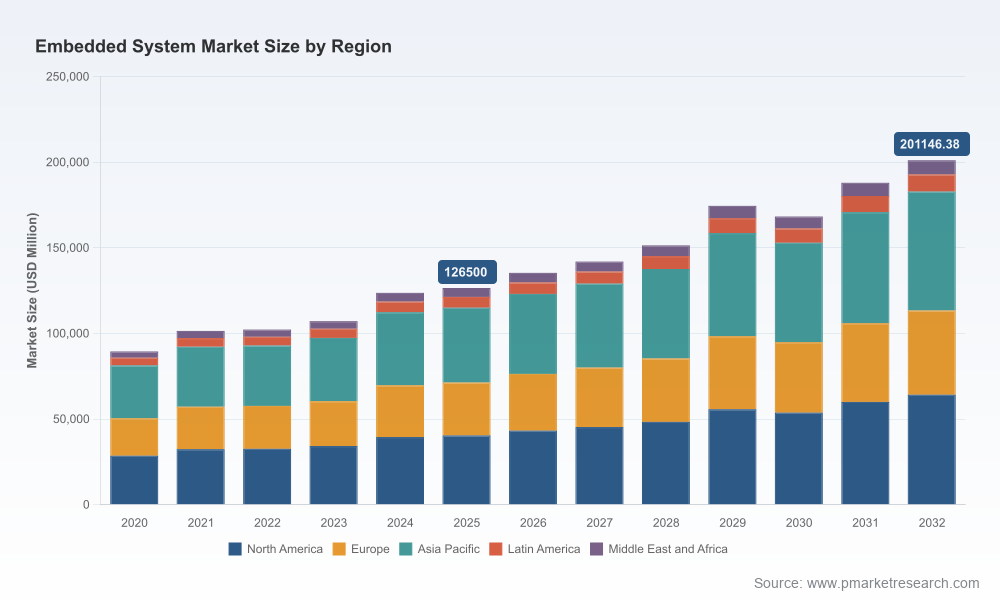

PW Consulting’s latest market intelligence — the Worldwide Embedded System Market Report (base year 2025, historical series 2020–2025, forecast 2026–2032) — delivers an operationally focused briefing designed to inform capital allocation, product roadmaps, and procurement strategy in 2026. The embedded systems market reached an estimated USD 126,500 Million in 2025 and is modeled to expand to roughly USD 201,146 Million by 2032, reflecting a compound annual growth rate (CAGR) of 6.85% over the forecast interval. This preview explains why that trajectory matters for enterprise decision-makers this year, what forces will shape winners and losers, and how the full report converts market math into executable workplans.

Worldwide Embedded System Market

Why this report is strategically valuable for 2026 planning

- Transforms macro forecasts into decision-ready insights: the report translates top-line growth into scenario-based revenue and supply needs for product lines, procurement bands, and engineering headcount over 18–36 month horizons.

- Aligns compliance and product timelines: it maps regulatory inflection points to development milestones so embedded platforms meet incoming requirements without derailing launch schedules.

- De-risks sourcing and BOM decisions: the report’s supply-chain stress tests and component-price sensitivity models let procurement teams quantify exposure to memory and semiconductor tightness.

- Shapes M&A and partnership playbooks: it identifies capability gaps and the archetypes of attractive targets or integration partners across silicon, middleware, and systems integrators.

Key market dynamics shaping 2026 strategy

- Regulatory acceleration: The EU’s Cyber Resilience Act (with its transition timeline) and new system/software process standards such as ISO/IEC/IEEE 12207:2026 create a dual compliance and productization imperative. Companies must embed secure development lifecycles, SBOM practices, and vulnerability handling into product definitions now to avoid late-stage redesigns.

- Standards and functional safety remain determinative: Established safety regimes (e.g., automotive and industrial standards) continue to govern design choices in safety-critical segments; certification timelines must be incorporated into product roadmaps and cost forecasts.

- Component supply and cost volatility: Memory and RAM pricing for embedded-grade LPDDR4X/LPDDR5X has risen as capacity is reallocated toward high-volume AI applications. Procurement teams must assume constrained availability into 2027 and adopt hedging, alternative BOMs, and long-lead contracts as default practices.

- Talent and tooling shift: A constrained pool of experienced embedded engineers is accelerating adoption of AI-assisted coding, model-based design, and higher-level development frameworks — changing hiring profiles and reducing time-to-market when integrated correctly.

- Edge AI and compute differentiation: The competitive battleground is moving from raw silicon performance to integrated edge stacks (processors + optimized frameworks + lifecycle management). Firms that master software abstraction, security, and long-life availability will command pricing premiums.

- Recent industry moves underscore consolidation and cross-stack play: Examples such as acquisitions that link microcontroller SDKs to cloud platforms and product announcements for automotive ADAS I/O illustrate a trend toward vertically integrated offerings that reduce integration risk for OEMs.

Competitive landscape — who to watch and why

The embedded systems ecosystem remains diversified: specialist silicon vendors, mainstream SoC suppliers, analog and power leaders, and platform software providers each occupy distinct strategic positions. The report’s vendor analysis synthesizes product portfolios, go-to-market positions, and partnership dynamics for leading firms including:

Worldwide Embedded System Market

- Intel Corporation (Santa Clara) — Leverages broad processor platforms and edge AI stacks with an emphasis on long-life availability and industrial-grade roadmaps; strategic for customers prioritizing compute-density and manageability across fleet deployments.

- Texas Instruments (Dallas) — Offers depth in microcontrollers, analog, and power management tailored to industrial and automotive controllers; a go-to for robust mixed-signal BOMs and long-term support contracts.

- NXP Semiconductors (Eindhoven) — Focused on secure MCUs and connectivity for automotive and edge compute; strong in secure boot and vehicle network domains where cryptographic and real-time requirements converge.

- STMicroelectronics (Geneva) — The STM32 ecosystem and sensor/power integration make ST a pragmatic choice for OEMs seeking broad developer support and rapid prototyping to production pathways.

- Renesas (Tokyo) — Addresses safety-critical automotive and industrial segments with specialized SoCs and an emphasis on functional safety compliance.

- Qualcomm (San Diego) — Competitive in wireless-enabled embedded platforms and edge AI acceleration for mobile-adjacent use cases.

- Infineon (Neubiberg) — Strength in power semiconductors and secure microcontrollers for electric powertrain and secure embedded platforms.

- Microchip (Chandler) — Broad portfolio across MCUs and analog, attractive for low-power and embedded control designs with predictable lifecycle policies.

- Analog Devices (Wilmington) — Strong in high-performance analog and DSP solutions for industrial sensing and high-fidelity embedded applications.

- Samsung Electronics (Suwon) — Memory and integration capabilities that matter for BOM optimization in consumer and industrial systems.

- Broadcom (San Jose) — Networking and wireless components that underpin infrastructure and IoT gateway platforms.

- NVIDIA (Santa Clara) — Leading edge for GPU-accelerated edge AI platforms and autonomy stacks — critical for high-performance inference and perception systems.

- AMD (Santa Clara) — Alternatives for embedded high-performance compute and adaptive SoC approaches in industrial and edge HPC environments.

Rather than ranking vendors by headline shares, PW Consulting’s vendor dossiers highlight capability adjacency maps, time-to-certify estimates, and risk/return profiles for collaborative sourcing.

Worldwide Embedded System Market

What the full report contains (practical deliverables)

- Executive summary and strategic implications for 2026 board cycles.

- Historical market analysis (2020–2025) and a granular forecast model (2026–2032) with scenario toggles for supply stress and regulation shifts. Top-line figures and growth trajectories are included.

- Segment and use-case playbooks (automotive, industrial, consumer, healthcare, telecom, aerospace/defense) that translate TAM into prioritized product features, safety requirements, and go-to-market motions.

- Component price-sensitivity models and supply-chain heatmaps, including memory risk scenarios and recommended procurement clauses.

- Vendor scorecards, partnership matrices, and integration complexity indices for leading silicon and platform providers.

- Regulatory compliance matrix aligning product lifecycle activities to Cyber Resilience Act obligations, SBOM production, and system engineering norms (ISO/IEC/IEEE 12207:2026).

- Technology radar and roadmap options for edge AI, secure boot, OTA management, and lifecycle tooling.

- M&A and investment target shortlist with diligence templates and valuation stress tests suited to strategic buyers and PE investors.

- Operational playbooks: procurement checklist, engineering staffing plans, certification timelines, and go-to-market launch sequences.

- Datasets, assumptions, and methodology appendix to reproduce forecasts within corporate planning tools.

Concrete recommendations for executives in 2026

- Embed regulatory compliance into product design now: finalize SBOM tools, vulnerability disclosure processes, and development lifecycle updates to align with the EU timeline and ISO/IEC/IEEE 12207:2026.

- Adopt BOM flexibility: qualify alternate memory and power IC suppliers, modularize designs to allow late-stage component substitution, and include price-escape and allocation clauses in multi-year contracts.

- Prioritize secure-by-design architectures: invest in cryptographic roots, secure update pipelines, and hardware-backed identity to reduce long-term field risk and warranty costs.

- Hedge talent constraints: combine selective hiring of senior embedded engineers with investments in AI-assisted tooling and model-based design to multiply engineering throughput.

- Stage investments in edge AI where value capture is highest (safety-critical inference, predictive maintenance, and latency-sensitive control); tie CapEx to clearly defined ROI triggers.

- Use vendor scorecards in procurement: require multi-year availability commitments from silicon suppliers and align penalties to certification/quality lapses.

- Set up an M&A scouting function calibrated to the report’s capability archetypes — look for IP-rich middleware and service businesses that shorten time-to-certify.

How executives should consume the report

Use the report as a planning anchor in Q2 2026: feed the forecast model into FY27 CapEx and hiring plans, apply the compliance matrix to product release cascades, and run two “stress-test” workshops with procurement and engineering to validate BOM and certification timelines. For corporate development teams, the vendor dossiers and M&A shortlists provide immediate targets for diligence and partnership pilots.

PW Consulting’s Worldwide Embedded System Market Report is structured as a decision support tool — not merely a data dump. It surfaces the levers executives can pull in 2026 to align architecture, supply strategy, and regulatory compliance with the market growth window represented by a mid-single-digit CAGR and a materially larger market by 2032. For organizations preparing to commit R&D budgets, negotiate supply agreements, or evaluate bolt-on acquisitions this year, the full report converts industry dynamics into prioritized, executable plans.

Next steps

Access to the complete report provides the full segmentation tables, vendor revenue breakdowns, regional opportunity maps, and downloadable forecast models that underpin these recommendations. PW Consulting’s advisory teams are available to run tailored briefings and scenario workshops that translate the intelligence into your 90–180 day action plan.

For detailed analysis of this topic, please visit the official page:Worldwide Embedded System Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com