Worldwide Aircraft Load Control Solution Market — Strategic Outlook for 2026 Decisions

Executive snapshot

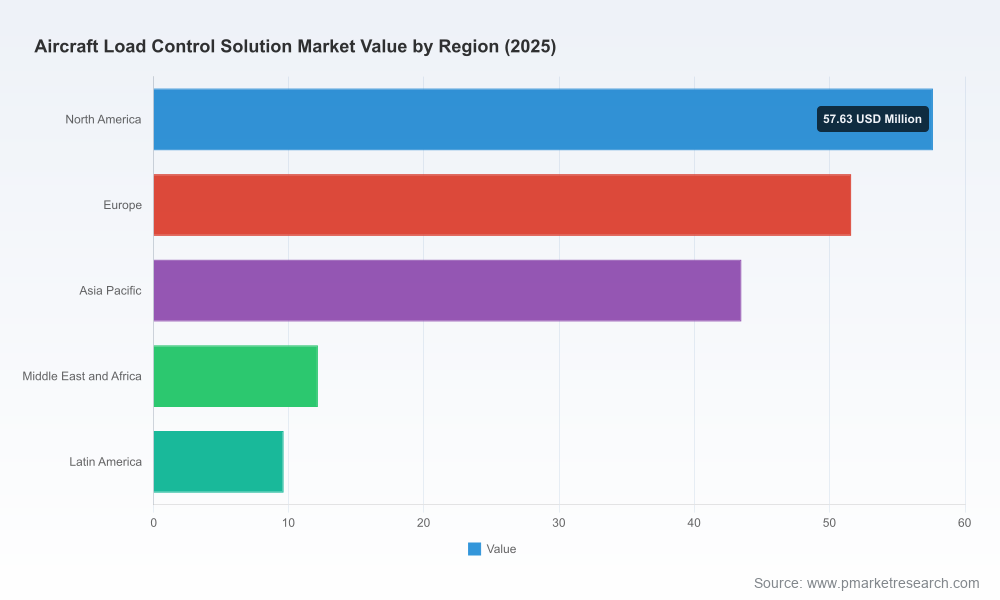

As airlines, ground handlers and aviation authorities accelerate digital transformation in operations, aircraft load control solutions have moved from niche safety tools to strategic enablers of operational efficiency, fuel optimisation and regulatory compliance. PW Consulting’s new market study — benchmarked to a 2025 base year and projecting through 2032 — shows a resilient growth trajectory led by software-driven automation: the global market is expected to continue expanding at a compound annual growth rate (CAGR) of 6.72% across the 2026–2032 forecast horizon. In absolute terms the market climbs from a mid‑hundreds million USD base in 2025 to a substantially larger valuation by 2032, underscoring the commercial imperative for aviation operators and suppliers to re-evaluate load control as a core component of their operational technology stack.

Worldwide Aircraft Load Control Solution Market

Why load control matters to 2026 strategy

- Safety-first regulation is tightening. Global regulatory drivers — including initiatives by ICAO, FAA and regional authorities — increasingly mandate precise, auditable weight and balance calculations and favour digital, verifiable workflows that reduce human error and ensure traceability.

- Operational economics are material. Optimised load distribution and accurate Estimated Zero Fuel Weight (EZFW) calculations translate into measurable fuel savings and payload improvements. For fleets operating at scale, even small percentage improvements compound into significant cost differentials.

- Digital integration is the new hygiene factor. Airlines seeking competitive advantage are demanding load control systems that integrate seamlessly with flight planning, Electronic Flight Bag (EFB) platforms, departure control, and enterprise IT. Offline/online resilience, API ecosystems and automation (including zero‑click loadsheet generation) are now purchase criteria, not optional features.

- Service model pluralism: CLC versus decentralised. Centralized Load Control (CLC) centres continue to deliver scale benefits and consistency for network operators and handling conglomerates, while station-level digitalisation and edge-capable solutions appeal to operators requiring redundancy and local autonomy. Strategic decisions in 2026 should reconcile these models within a clear cost‑benefit and risk framework.

Market dynamics — what the numbers tell us

Our study traces a clear evolution from manual, on‑premise workflows to predominantly cloud-enabled, automated operations. The overall market trajectory from 2020 through 2025 exhibits consistent growth driven by airline recovery, capacity rebuild, and accelerated IT spend on safety-critical function digitalisation. Looking forward, the 6.72% CAGR reflects a balance of continued modernization, regulatory pressure, and incremental adoption by cargo and third‑party ground handling sectors. Market concentration metrics indicate a landscape where several established vendors capture a meaningful share of value, yet opportunities remain for specialised providers and integrators to win discrete pockets of demand — especially where advanced automation, offline resilience, or bespoke services are required.

Worldwide Aircraft Load Control Solution Market

Competitive landscape — positioning and implications

- Established specialist vendors: Several long‑standing W&B and load planning specialists have evolved their products to support both centralised and distributed operational models. Their strengths typically include deep domain expertise, aircraft fleet coverage, and regulatory compliance support — attributes that buyers prioritise when risk aversion is high.

- Platform integrators and IT incumbents: Major airline IT platforms and flight planning vendors have folded load control capabilities into broader operational suites, offering the advantage of end‑to‑end workflow continuity and simplified vendor management. For airlines aiming to simplify vendor footprints, integrated platform offerings are increasingly attractive.

- Service providers and CLC operators: Outsourced centralized load control services are scaling via regional hubs and remote operations centres, delivering high throughput and consistent loadsheet quality for multi‑airline customers. Recent operator disclosures demonstrate the operational scale that CLC providers achieve, reinforcing the appeal of economies of scale and standardised processes.

- New‑wave automation vendors: A cohort of agile providers has differentiated through high automation, “zero‑click” loadsheet generation, real‑time reconciliation and offline/online hybrid capabilities. These solutions are particularly compelling for operators seeking rapid productivity gains and reduced headcount dependency in peak operations.

For procurement and strategy teams entering vendor selection cycles in 2026, the competitive topology implies that selection criteria must be multi-dimensional: compliance and safety certification; integration breadth and API maturity; automation level and exception management; business model fit (capex vs opex); and vendor operational scale or managed services capability.

Worldwide Aircraft Load Control Solution Market

Regulatory and standards context

Regulatory evolution is central to the market’s growth story. Continued emphasis by authorities and standards bodies on auditable, digitally‑traceable load control workflows is driving adoption of certified systems and formalised training pathways. Industry standards and certification programmes for load controllers and simulation systems are aligning with modern digital toolchains, creating a clearer compliance roadmap for buyers — and a higher bar for vendors on documentation, change‑management and feature governance.

What’s in the PW Consulting report — practical deliverables for 2026 decision‑makers

The report is built as an operational playbook for executives, program leads and procurement teams considering investments in load control technology or services in 2026. Key deliverables include:

- Market sizing and forward scenarios: macro projections by year (2020–2032) and sensitivity models that translate regulatory or fuel‑price shocks into adoption outcomes.

- Vendor profiling and capabilities matrix: structured assessments of incumbent and emergent suppliers covering product architecture, automation depth, offline resilience, integration modalities, delivery models (software, SaaS, CLC services), and implementation track record.

- Decision framework and RFP toolkit: procurement scorecards, standardised RFP language, evaluation weightings tailored to strategic priorities (safety, TCO, integration, time‑to‑value), and negotiating levers for SaaS and managed services contracts.

- Implementation blueprints: phased migration pathways for airlines and handlers that are shifting from on‑premise to cloud or hybrid models, including data migration playbooks, regression testing plans, and change management templates for load controller certification and retraining.

- ROI and TCO modelling: customizable financial models showing expected payback windows under varying automation levels and operational scale assumptions — intended to support CAPEX/OPEX trade‑off decisions without exposing proprietary vendor metrics.

- Regulatory compliance checklist: mapping product features and operational controls to ICAO/FAA/EASA/IATA expectations and NextGen initiatives, plus recommended audit trails and documentation for certification readiness.

- Case studies and best practices: anonymised operator case studies demonstrating fuel savings, throughput improvements and error‑rate reductions from both CLC and decentralized implementations.

Strategic recommendations for 2026

- Treat load control as a platform decision: Integrate W&B systems into broader flight operations and performance platforms to capture cross‑functional efficiencies. RFPs should require API‑first architectures and demonstrable integration with flight planning and EFB ecosystems.

- Prioritise automation plus exception management: Solutions that automate the routine but provide clear, visual exception workflows for human oversight deliver the best balance of safety and productivity.

- Design for hybrid ops: Balance centralisation benefits with resilience. For network carriers, centralised control coupled with edge‑capable stations provides operational continuity during regional disruptions.

- Negotiate outcome‑based SLAs: Shift commercial discussions toward measurable metrics (loadsheet accuracy, processing throughput, reconciliation timelines) and include change‑management milestones tied to adoption and training outcomes.

- Plan for regulatory traceability: Ensure any chosen solution produces immutable audit trails, role‑based access logs, and automated reporting to satisfy evolving authority requirements.

- Use pilots to de‑risk rollouts: Run focused pilot programmes targeting high‑volume routes or gateways with rigorous measurement of error rates, fuel impacts and processing times before enterprise scale‑up.

How to use the research in procurement and M&A

For buyers, the report’s vendor scorecards and procurement tools can accelerate selection cycles and reduce implementation risk. For investors and corporate development teams, the market maps and concentration measures illuminate pockets ripe for consolidation or partnership — particularly where integration assets or managed CLC capabilities can be combined with cloud software to create bundled offerings. The research highlights areas where scale and automation yield defensible margins, and where niche differentiation — such as offline resilience or ultra‑low latency integration — remains valuable.

Conclusion — positioning for operational advantage in 2026

Aircraft load control is no longer a back‑office compliance line item; it is an operational lever that influences safety, fuel economics and on‑time performance. The market’s steady growth and shifting competitive dynamics present clear choices for 2026 planners: adopt cloud‑first, automation‑centric solutions that integrate with enterprise flight operations; retain or build CLC capabilities where scale creates economic benefits; and insist on traceability and regulatory readiness as non‑negotiables. PW Consulting’s report equips decision‑makers with the data, vendor insights and practical tools required to turn these choices into executable programmes.

Next steps

To access the full intelligence — including the complete vendor profiles, the procurement toolkit, implementation blueprints and the detailed scenario models that underpin our market projections — download the PW Consulting Worldwide Aircraft Load Control Solution Market report from our research portal. The full report contains the granular segmentation and actionable appendices needed to convert strategic intent into delivery-ready plans for 2026 and beyond.

For detailed analysis of this topic, please visit the official page:Worldwide Aircraft Load Control Solution Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com