Worldwide Charging Port Door Actuators Market — Strategic Outlook for 2026 Decision-Makers

As electric vehicle (EV) architectures continue to evolve from accessory components into strategic differentiators, charging port door actuators (CPD actuators) have emerged as a small part with outsized implications. For OEMs, Tier‑1 suppliers and component investors, the actuator is no longer a commodity hinge — it is a convergence point where safety, user experience, software integration and supply‑chain resilience meet. PW Consulting’s new market study synthesizes five years of historical performance with forward‑looking scenario analysis to equip executives making 2026 investment, sourcing and product decisions.

Worldwide Charging Port Door Actuators Market

What the market looks like at a glance

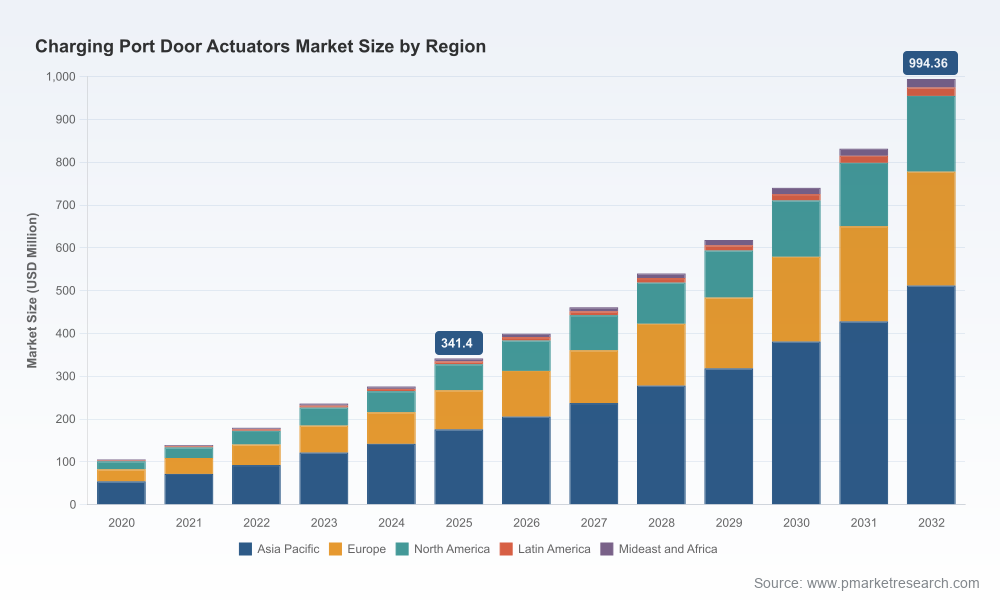

Our base‑year assessment (2025) shows the global CPD actuator market at approximately USD 341.4 Million, following robust expansion from the early 2020s. The market is projected to grow at a compound annual growth rate (CAGR) of roughly 16.5% through the 2026–2032 forecast window, with total industry revenues approaching the USD 1 billion mark by the end of that period under the base scenario. This trajectory reflects accelerating BEV program ramps, regulatory standardization of charging interfaces, and a steady migration toward electronically controlled, feature‑rich actuator designs.

Worldwide Charging Port Door Actuators Market

What the PW Consulting report delivers — practical, actionable outputs

- Top‑line and repeatable forecasting models: downloadable scenario spreadsheets (base, upside, supply‑constrained) calibrated to OEM program timelines and vehicle production cycles.

- Procurement playbook: supplier scorecards, critical‑component risk maps, and recommended contract structures (long‑term buy, safety stock, consignment) tailored for 2026 supplier negotiations.

- Technical deep dives: comparative analysis of actuator architectures (BLDC with LIN control vs. traditional mechanical release), failure‑mode catalogs, and compliance checklists tied to functional safety (e.g., ISO 26262) and environmental sealing requirements.

- Go‑to‑market and partnership frameworks: decision trees for co‑development with OEMs, strategic sourcing options with Tier‑1s, and integration blueprints for HMI/vehicle network stacks.

- M&A and investment pipeline: an annotated list of acquisition targets and capability gaps (mechatronics, sensor fusion, IP around fail‑safe locking), with valuation sensitivity under different adoption scenarios.

- Supply chain diagnostic tools: lead‑time heatmaps, single‑point‑of‑failure analysis for rare‑earth magnet and precision gear supply, and mitigation playbooks to reduce 12–16 week procurement exposures.

Core dynamics shaping 2026 decisions

- Standards and regulations are accelerating adoption. Regulatory pushes for standardized charging interfaces in key markets — and stringent safety expectations for child‑proofing, fail‑safe unlocking and environmental resistance — are creating an almost prescriptive feature set for CPD actuators. Compliance is table stakes; differentiation now comes from reliability, maintainability and user experience.

- Technology migration toward smart actuation. The functional profile of winning products is shifting toward BLDC motors with LIN/CAN integration, on‑board sensors (position, torque, temperature), anti‑pinch and ice‑breaking capabilities, and HMI features such as capacitive/gesture entry and status lighting. Systems that bundle intelligence and diagnostics reduce warranty exposure and unlock recurring revenue via telematics‑enabled aftermarket services.

- Supply‑chain fragility remains a constraint. Specialized components — notably rare‑earth magnets and precision gearing — are creating extended lead times (we see 12–16 week exposures for select actuator families). These bottlenecks amplify the importance of dual sourcing, design for supplier flexibility and early engagement with sub‑tier vendors.

- Concentration and competition. The market is moderately concentrated: a handful of established Tier‑1s and specialist OEMs together control a meaningful portion of demand, but there remains room for agile entrants with IP differentiation or privileged OEM relationships.

Competitive landscape — who to watch and why

Our supplier mapping balances product capability, integration depth and go‑to‑market reach. Leading incumbents have moved beyond single‑component supply to offer system‑level solutions: actuator + flap + locking + diagnostics. The following profiles capture strategic positioning rather than full commercial terms — consult the full report for supplier scorecards and relational histories.

Worldwide Charging Port Door Actuators Market

- Magna International (Aurora, Canada) — Strong in system integration with its SmartAccess™ Charge Port Door, pairing high‑torque actuators with intelligent entry and optional HMI elements. Appealing to OEMs seeking turnkey assemblies and a supplier capable of scaling across platforms.

- Motion Controls Inc (MCi) (United States) — Focus on high speed/torque actuators and patented motion control (Lead‑Follow) suited to aggressive aerodynamic or active‑flap programs; relevant for customers prioritizing actuation performance.

- NMB Technologies / MinebeaMitsumi (Japan) — Offers bespoke BLDC actuator systems with integrated sensors and advanced control options; strengths lie in customization and compact electromechanical solutions.

- Haoyong Automotive Controls (China) and Padmini VNA Mechatronics (India) — Regional specialists with a focus on durable, cost‑sensitive models for high‑volume platforms and a growing role as procurement partners for cost‑driven programs.

- WITTE Automotive, Röchling, Marquardt, Johnson Electric, TE Connectivity — These firms bring complementary strengths: compact module design, kinematic engineering, advanced locking mechanisms, and robust connector/actuator suites for OBC and charger interfaces.

Recent industry moves underscore the competitive intensity: strategic co‑development agreements between major system suppliers and OEM groups, modular product launches enabling faster multi‑platform adoption, and program wins that secure multi‑year volumes for established suppliers. These events are symptoms of a market transitioning from early adoption to mainstream supply agreements.

Strategic implications and recommended actions for 2026

Executives preparing plans for 2026 face a narrow window to position assets and contracts before next‑generation OEM programs enter mass production. We recommend the following prioritized actions.

- Lock critical components through multi‑year agreements. Negotiate conditional long‑term supply contracts for magnets, precision gearsets and semiconductor drivers. Include tiered price‑protection clauses and accelerated cutover provisions to manage lead‑time volatility.

- Design for supplier flexibility. Transition to modular actuator platforms that can accommodate alternative motor types, control modules and gear trains without redesigning the vehicle bodywork. This reduces OEM release risk and shortens qualification cycles.

- Invest in software and diagnostics. Differentiate via remote health monitoring, over‑the‑air parameter updates, and richer telemetry to reduce field failures and enable aftermarket services.

- Prioritize functional safety certification. Make ISO 26262 compliance and rigorous IP/temperature testing part of the procurement checklist; non‑compliant bids should be treated as high‑risk regardless of price.

- Use scenario planning to size capacity and inventory. Model a base case, an accelerated BEV adoption case, and a supply‑constrained case to set buffer inventory and make CapEx timing decisions robust to demand swings.

- Explore bolt‑on M&A for critical capabilities. Consider acquiring specialist electromechanical or sensor integration firms to accelerate time‑to‑market and internalize key risks (e.g., proprietary gear trains, anti‑pinch algorithms).

- Structure pricing and warranty to incentivize quality. Use milestone‑based pricing and shared warranty reserves for first‑program supplies, shifting more risk back to suppliers proven on prior launches.

Risk map — what could derail 2026 plans

- Material supply shocks for rare‑earth magnets or precision gearing that extend lead times beyond mitigation buffers.

- Accelerated standard consolidation by charging network owners (lock formats) that outpace supplier compatibility roadmaps.

- Failure to achieve functional safety objectives during vehicle homologation, causing program delays and costly redesigns.

- Consolidation among Tier‑1s leading to re‑sourcing of volumes and margin compression for smaller suppliers.

How PW Consulting helps — the missing pages you’ll want in Q1 2026

The published executive summary is deliberately focused to provoke strategic discussion. Clients who license the full market study receive the proprietary data tables, supplier scorecards, BOM estimates by actuator family, and editable financial models that allow program‑level sensitivity testing. These deliverables were designed specifically to support supplier selection, make/buy decisions, negotiation of long‑lead components and M&A diligence ahead of 2026 program freezes.

For teams evaluating immediate tactical choices — whether to qualify an alternate supplier, commit to inventory, or pursue co‑development — the report provides the empirical foundation and decision templates required to move from conversation to contract.

Next steps

If your 2026 roadmap depends on reliable CPD actuator supply, resilient sourcing or differentiated actuator functionality, PW Consulting’s full Worldwide Charging Port Door Actuators Market study is built to be the working document that informs those decisions. Visit our report page or contact our industry practice to arrange a briefing, view sample models, and discuss an executive workshop tailored to your program timelines.

PW Consulting — turning actuator complexity into strategic advantage for 2026 and beyond.

For detailed analysis of this topic, please visit the official page:Worldwide Charging Port Door Actuators Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com