Worldwide Condensation Cure Silicone Rubber Market — Strategic Briefing for 2026 Decision-Makers

PW Consulting today publishes an executive industry briefing derived from our full Worldwide Condensation Cure Silicone Rubber Market report (base year 2025). This briefing distills the report’s most consequential, decision-ready insights for corporate leaders planning 2026 strategies. Drawing on a seven‑year historical window (2020–2025) and a forecast horizon through 2032, our analysis quantifies a steady expansion trajectory (CAGR 4.82% for the forecast period) and translates that trajectory into tangible strategic implications for procurement, R&D, commercial positioning and inorganic growth.

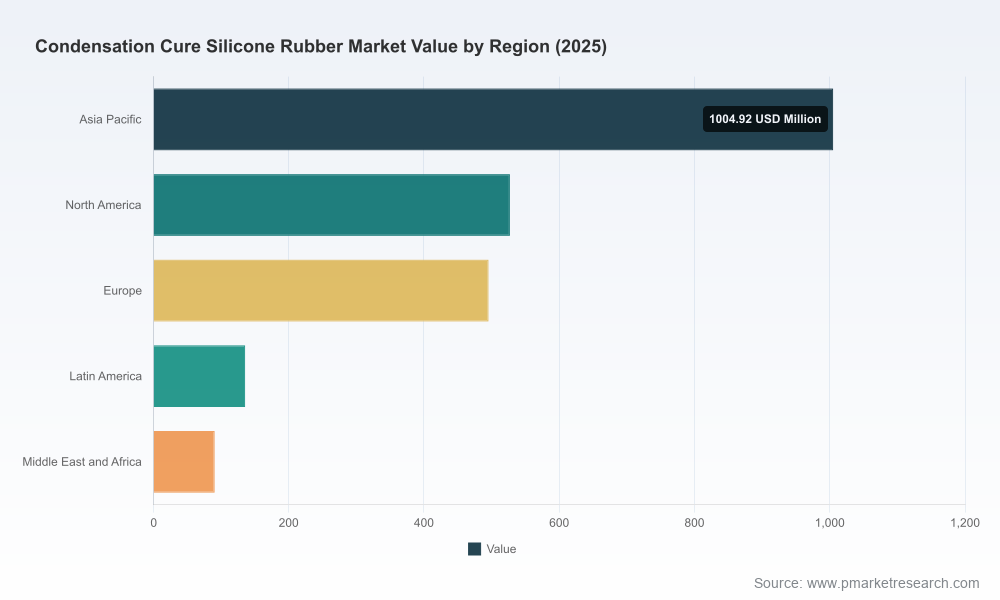

Worldwide Condensation Cure Silicone Rubber Market

Snapshot: Market trajectory and what it implies

At the macro level, the condensation cure silicone rubber market moved from the lower‑end of the billion‑dollar range in 2020 to more than two billion USD by the 2025 base year, reflecting resilience across end‑use sectors and a rebound from mid‑cycle volatility. Under our central model the market continues to expand through 2032, reaching just over three billion USD under current assumptions (compound annual growth 4.82%). For 2026 planning this means companies should treat demand as growth‑oriented but exposed to cost and supply shocks — a combination that rewards proactive commercial and procurement playbooks rather than tactical, transactional responses.

Worldwide Condensation Cure Silicone Rubber Market

Why this report is directly relevant to 2026 decisions

- It translates macro growth into actionable levers: cost sensitivity to key feedstocks, technology trajectories, and service differentiation opportunities that materially affect margin in 18–36 months.

- It isolates three practical decision horizons: near term (6–12 months) for procurement and price protection; medium term (12–24 months) for product and process investments; and strategic (24–60 months) for capacity and M&A choices.

- It maps regulatory and raw‑material risk onto commercial outcomes so pricing and contract structures can be stress‑tested with realistic scenarios rather than ad‑hoc assumptions.

Primary market dynamics and pressure points

The market’s growth is driven by sustained demand from tooling and moldmaking, construction sealing, electronics encapsulation, and maintenance/repair applications. However, two cost‑side realities dominate strategic tradeoffs in 2026:

Worldwide Condensation Cure Silicone Rubber Market

- Raw material squeeze: Key siloxane intermediates experienced significant price pressure through 2025. In particular, feedstocks linked to cyclic siloxanes rose materially, lifting upstream costs and compressing typical manufacturer margins unless price pass‑through mechanisms were adapted.

- Regulatory tightening: Environmental policies introduced in major producing jurisdictions affected production economics and, in some cases, availability. Companies that anticipated regulatory cost transfer were better positioned to sustain margins in 2025; those that did not found themselves negotiating spot premiums for constrained product families.

On the demand side, technology choices continue to segment the market. Condensation‑cure chemistries retain advantages in mold making and certain potting applications due to simplicity and formulation flexibility, while concerns around cure inhibition and compatibility remain differentiators versus addition‑cure systems. Product innovation that reduces cure time, improves tear strength, or eases post‑cure handling repeatedly shows up as a commercial lever in our customer interviews.

Segmentation and growth patterns (what we cover without giving away proprietary splits)

The report models growth across primary segmentation axes — by product technology (one‑component vs two‑component systems), by application vertical, and by region — and includes scenario‑based outlooks that flex for raw material shocks and regulatory changes. Rather than list proprietary segment shares here, we present directional findings useful for immediate planning:

- Technology bifurcation: One‑component and two‑component systems follow distinct adoption curves tied to end‑use technical requirements and service convenience. Each technology family requires different inventory, handling and technical support investments.

- Application momentum: Established categories such as mold making and construction remain foundational demand pools; electronics and automotive pockets show faster year‑on‑year normalization and premiumization potential as formulations adapt to higher thermal and electrical performance requirements.

- Regional dynamics: Supply chain and regulatory differentials will shape competitive positioning. Capacity siting and distribution strategies that explicitly account for these differentials outperform peers in margin retention during stress cycles.

Competitive landscape — structure, incumbents and strategic implications

Market concentration metrics indicate a moderately consolidated industry: the top three firms account for a meaningful share of market revenue while the top five capture well over half of market value. This structure produces both stability (predictable supply from tier‑one producers) and opportunity (niche specialists and regional players remain viable targets for partnerships or bolt‑on acquisitions).

Highlighted companies examined in the full report include global majors and specialty producers who together illustrate the competitive playbook set:

- Smooth‑On, Inc. (Macungie, PA, USA) — Broad product lines for moldmaking, including shore‑hardness variants tailored to casting with wax, gypsum, urethane, epoxy and polyester resins; customer‑facing technical service is a core strength.

- Polytek Development Corp. (USA) — Specialty in tin‑cured room‑temperature vulcanizing rubbers with focus on tear strength and release properties; positions itself against addition‑cure inhibition risk through formulation choices.

- Silicones, Inc. (USA) — Longstanding producer of condensation‑cure RTV‑2 systems with a portfolio spanning mold‑making to electronics potting and custom grades for special effects industries.

- CHT Group (Germany) — Offers condensation cure silicones plus catalysts and thixotroping agents to modify rheology and cure; active in trade forums and visible in product marketing.

- BBN Materials Co., Limited (China) — Regional specialist offering customizable cure profiles and operational parameters for craft and industrial moldmaking markets.

- Silpak, Inc. (USA) — Two‑component condensation cure RTV solutions with an emphasis on high‑strength rubbers for moldmaking.

- Elkem Silicones (Norway/global) — Supplies polycondensation systems suited to architectural and cast applications; global footprint supports large project supply.

- Shin‑Etsu Chemical Co., Ltd. (Japan) — Producer of rapid cure and high‑thermal stability grades; R&D emphasis on performance under thermal stress.

- Momentive Performance Materials (USA) — Established supplier of condensation cure systems with emphasis on validated recipes and catalyst systems.

From a strategic standpoint, incumbents are leveraging one or more of the following approaches: expand specialty formulation portfolios, deepen technical support to lock distribution channels, pursue selective capacity investments near feedstock hubs, and enter partnerships to compensate for regional regulatory impacts. For challengers, the two most repeatable paths to economic return are either (a) regional dominance with highly differentiated service and logistics, or (b) formulation leadership that unlocks premium pricing in constrained application niches.

What the full report gives you (practical, executable content)

The complete PW Consulting report delivers the following decision tools designed to be applied directly in 2026 planning cycles:

- A transparent financial model with base‑case and stress scenarios that quantify revenue, margin and cash‑flow sensitivity to feedstock price shocks and pass‑through speeds.

- Competitive benchmarking that includes product portfolios, go‑to‑market models, recent developments and an M&A target shortlist for buyers and PE sponsors.

- Procurement playbook with indexation templates, hedging strategies, supplier scorecards and sample contract clauses to mitigate D4 and other feedstock volatility.

- Regulatory risk map that translates policy changes into cost, capacity and compliance timelines for major producing jurisdictions.

- R&D prioritization matrix linking customer value to realistic development timelines and estimated incremental margin uplift for cure speed, thermal stability and low‑VOC formulations.

- Commercial growth plan templates by end‑use segment, including value‑added services where premiumization is achievable.

Immediate, high‑impact actions for 2026

Based on our analysis, companies that act early on a short list of measures will materially improve 2026 outcomes:

- Lock conditional pricing frameworks with suppliers today — adopt hybrid indexation that blends spot, monthly and quarterly adjustments to share upstream risk with suppliers and customers.

- Prioritize R&D projects with the fastest path to margin: faster cure cycles and thermal stability upgrades often unlock higher ASPs and lower lifecycle costs for customers.

- Test dual‑sourcing and regional buffer strategies for critical lines; small capacity cushions reduce exposure to localized regulatory disruptions.

- Use the report’s M&A diagnostic to evaluate regional platform targets or specialty formulation plays that can be integrated within 12–18 months.

- Augment commercial teams with technical application engineers to convert specification‑led opportunities into premium, higher‑margin contracts.

Next steps and where to get the complete intelligence

This release is a strategic preview designed to demonstrate the report’s practical orientation without disclosing the proprietary segment breakdowns, company benchmarking scores and the interactive forecast model that underpin our recommendations. For full access to the granular data, segment‑level forecasts, company scorecards and the downloadable financial model, please consult the PW Consulting report page linked from our corporate site.

In a market where a combination of steady demand growth and periodic supply‑side shocks creates both opportunity and risk, 2026 will reward firms that translate market intelligence into concrete procurement, R&D and M&A moves. PW Consulting’s full condensation cure silicone rubber market report provides the connective tissue between data and decision: models you can run, scenarios you can stress, and playbooks you can execute.

For detailed analysis of this topic, please visit the official page:Worldwide Condensation Cure Silicone Rubber Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com