Worldwide Paper Dry Strength Resin Market — Strategic Preview for 2026 Decision-Making

Executive summary

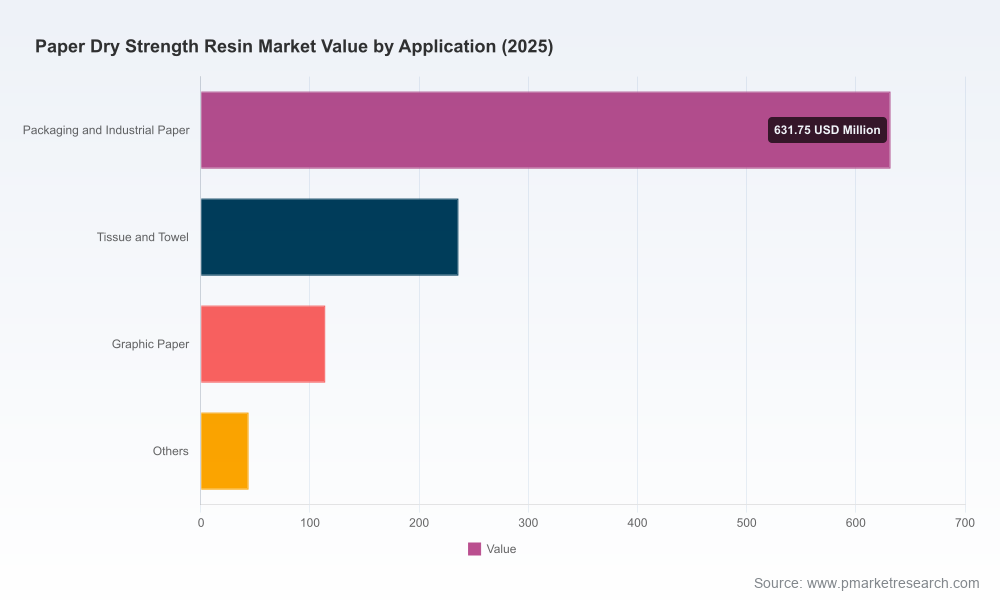

PW Consulting’s new market intelligence brief previews the Worldwide Paper Dry Strength Resin Market and explains why the 2026 planning cycle must treat dry strength chemistry as a strategic lever — not a commodity line item. The sector reached approximately USD 1,025.4 Million in 2025 and exhibits multi-year resilience, with a compound annual growth rate (CAGR) of 3.82% projected across the 2026–2032 forecast window. By 2032 the market is projected to surpass USD 1.3 billion. These headline metrics mask important inflection points driven by raw-material volatility, sustainability transitions, and shifting mill-level optimization priorities; our report translates those dynamics into actionable options for commercial, procurement, R&D and M&A leaders.

Worldwide Paper Dry Strength Resin Market

Why this matters for 2026

- Small percentage shifts in dry strength dosing or product selection deliver outsized economics on paper-making lines — affecting basis weight, energy consumption, machine runnability and finished-product yield.

- Volatile acrylamide feedstock prices and an accelerating shift toward bio-based alternatives create both risk and opportunity windows for suppliers and consumers in the coming 12–24 months.

- Competitive intensity is moderate: a handful of global chemical majors and specialized polymer houses influence pricing, innovation cadence and service models. Market concentration metrics indicate the top three and five suppliers hold meaningful share without forming an impenetrable oligopoly — a structure that favors smart partnerships, targeted innovation and selective consolidation.

Market trajectory and what the numbers imply

The market’s 2020–2025 history shows steady expansion interrupted by episodic headwinds; 2024 represented a near-term peak followed by stabilization into 2025. Our forecast anticipates a near-term normalization around 2026 before sustained expansion resumes through 2032 — culminating in a market value north of USD 1.3 billion. This path reflects two countervailing forces: (1) demand-side pull from lightweighting, tissue/towel performance upgrades and packaging grade optimization; and (2) supply-side pressure from feedstock price swings and regulatory/sustainability constraints.

Worldwide Paper Dry Strength Resin Market

For executives, the practical takeaway is straightforward: 2026 will be a year to operationalize resilience — hedging raw-material exposure, locking in performance contracts with suppliers, and accelerating trials of lower-carbon or bio-based compositions whose value will be priced into procurement conversations by the end of the year.

Worldwide Paper Dry Strength Resin Market

What the full report delivers (highly operational)

- Market sizing and scenario modeling showing base, upside and downside pathways through 2032 — including sensitivity analyses versus feedstock price shocks and rapid adoption of bio-based chemistries.

- Proven vendor selection framework and a supplier capability matrix that compares technical support, dosing systems, regional manufacturing footprint and after-sales trial performance (designed to shorten vendor qualification timelines by months).

- Commercial playbook for procurement: total cost of ownership (TCO) templates, contract clauses for performance guarantees tied to energy and fiber savings, and dynamic pricing triggers tied to acrylamide indices.

- R&D prioritization roadmap: lab-to-machine trial sequencing, KPI templates for tensile/burst vs. drainage trade-offs, and decision gates for when to scale an alternative chemistry.

- M&A and partnership lenses: valuation comparables, technology scouting heatmaps, and three scenario-based integration plans for acquiring specialty polymer capability or entering licensing partnerships with established resin developers.

- Risk and resilience toolkit: supply-chain mapping, dual-sourcing playbooks, and regulatory compliance checklists aligned to likely 2026 policy developments on polymer stewardship and emissions reporting.

Competitive landscape — who matters and why

The category blends global chemical majors, specialty polymer houses and regional formulators. Market concentration metrics show the top three players control a meaningful plurality of the market, while the top five approach parity with nearly half of market share — a structure that shapes negotiation dynamics and partnership opportunities.

- Solenis (Wilmington, DE, USA) — Strength: broad performance portfolio across amphoteric, anionic and cationic chemistries and strong track record in mill-level sustainability projects. Tactical implication: ideal partner for mills seeking turnkey trials tied to decarbonization KPIs.

- Kemira (Helsinki, Finland) — Strength: engineered systems combining synthetic PAM chemistries with fiber and cellulose additives; recent product launches show focus on "pump-and-go" operational simplicity. Tactical implication: attractive for manufacturers targeting rapid conversion with measurable refining and basis-weight benefits.

- Buckman (Memphis, TN, USA) and SNF Group (France) — Strengths: deep polymer expertise and scalable manufacturing; SNF in particular offers resilience for grades limited by poor fiber quality. Tactical implication: prime candidates for long-term technical supply agreements tied to capacity guarantees.

- BASF, Harima Chemicals, Ecolab (Nalco Water) — Strengths: R&D muscle, global service networks and integrated paper-chemical portfolios. Tactical implication: best positioned to bundle strength chemistry with other wet-end chemistries and digital process optimization services.

- Regional specialists (e.g., Shandong Tiancheng, Derypol, Aurora Specialty Chemistries, Thermax, Aries Chemical, Seiko PMC) — Strengths: localized cost competitiveness, niche formulations and rapid customization. Tactical implication: essential partners for regional supply redundancy and cost arbitrage strategies.

Notable recent moves underscore strategic directions: Kemira’s late-2025 launch of a ready-to-dispense strength solution signals a push for operational simplicity and fast ROI for tissue mills; Solenis’ recognition for CO2 reductions tied to a Hercobond product line demonstrates how performance claims anchored to sustainability outcomes can become a competitive differentiator.

Key market dynamics to factor into 2026 plans

- Raw-material volatility: Acrylamide monomer pricing has oscillated considerably in recent cycles. Firms must model procurement scenarios against a realistic price band and consider index-linked contracts, strategic inventory buffers and backward integration where feasible.

- Sustainability as a buyer requirement: Bio-based and energy-efficient formulations are moving from “nice-to-have” to procurement prerequisites in progressive mill chains. Early adopters of lower-carbon chemistries can use product claims to renegotiate downstream commercial terms.

- Technology-service convergence: Suppliers that pair polymer formulations with dosing systems, digital monitoring and machine-optimization services capture higher margin and stickier contracts.

- Operational trade-offs: Decision-makers need to weigh tensile and burst improvements against drainage and retention impacts — the optimal formulation is almost always application- and machine-specific, requiring fast, rigorous trial protocols.

Practical recommendations for 2026

PW Consulting advises executive teams to adopt a three-track approach in 2026: protect, optimize and transform.

- Protect (short term, 0–12 months): Lock in critical supply via dual-source agreements; negotiate performance-based contracts that include trial-to-production transition timelines; implement acrylamide hedging or index-linked pricing to reduce P&L volatility.

- Optimize (next 6–18 months): Run prioritized machine trials with 3–5 shortlisted chemistries using the supplier capability matrix from our report; measure full TCO impacts (energy, refining, basis weight, waste) rather than unit price; adopt dosing automation to reduce variability.

- Transform (12–36 months): Invest selectively in bio-based or hybrid chemistries where lifecycle analysis indicates clear carbon or cost advantage; consider bolt-on acquisitions to fill formulation gaps or gain regional footholds; integrate strength chemistry strategy with fiber sourcing and product portfolio decisions to capture lightweighting upside.

Use cases — how companies are already converting insight to value

- A large tissue producer used a supplier performance contract to reduce refining energy per tonne while maintaining tensile targets — the arrangement paid for itself within two production cycles.

- A packaging board mill adopted a staged trial sequence from lab to full machine that reduced time-to-decision by 60% and avoided a costly mis-specification tied to drainage degradation.

- A specialty chemical supplier bundled a new resin launch with a software-driven dosing monitor, increasing renewal rates and pushing average contract tenures upward.

What the PW Consulting report does not disclose here — and why

In keeping with the "trailer" principle, this press brief demonstrates analytical depth and immediate applicability while deliberately withholding detailed segment-by-segment market shares, region-by-region percentages, and specific price point forecasts. Those proprietary tables, interactive scenario models, supplier scorecards and granular application-level economics are reserved for the full report—where they are presented with source-level data, model assumptions and downloadable spreadsheets to support procurement RFIs, R&D roadmaps and M&A diligence.

How to act

For commercial, procurement and R&D leaders preparing 2026 plans: begin with a rapid internal audit of current strength-resin dependencies, then run a three-month supplier qualification sprint integrating the procurement and technical gates outlined above. PW Consulting’s full Worldwide Paper Dry Strength Resin Market report includes the precise templates and modeling workbooks to accelerate those steps from concept to contract.

Methodology and credibility

The full study synthesizes primary mill- and supplier-level interviews, company disclosures, patent and product-release analysis, and a proprietary demand model calibrated to historical volumes and pricing dynamics. Sensitivity testing against feedstock price bands and policy shift scenarios underpins our scenario outputs for 2026–2032.

To access the full dataset, granular segmentation, supplier scorecards and executable playbooks that support decisive 2026 investments, please consult the PW Consulting report package and our advisory service options.

For detailed analysis of this topic, please visit the official page:Worldwide Paper Dry Strength Resin Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com