Worldwide Military Off-road Vehicles Market: Strategic Preview for 2026 Decision-Making

As PW Consulting’s Senior Strategy Advisor and Chief Industry Analyst, I present a concise, forward-looking briefing drawn from our new Worldwide Military Off-road Vehicles Market report. This preview is written for defense planners, procurement executives, OEM strategy teams, and private equity investors who must translate macro trends into concrete 2026 actions. It highlights the report’s most consequential, decision-relevant insights while deliberately withholding the full granular segmentation that distinguishes the paid report—our “trailer” approach designed to demonstrate analytic depth and motivate direct access to the source for operational details.

Worldwide Military Off-road Vehicles Market

Market Trajectory: Where the industry stands and where it is going

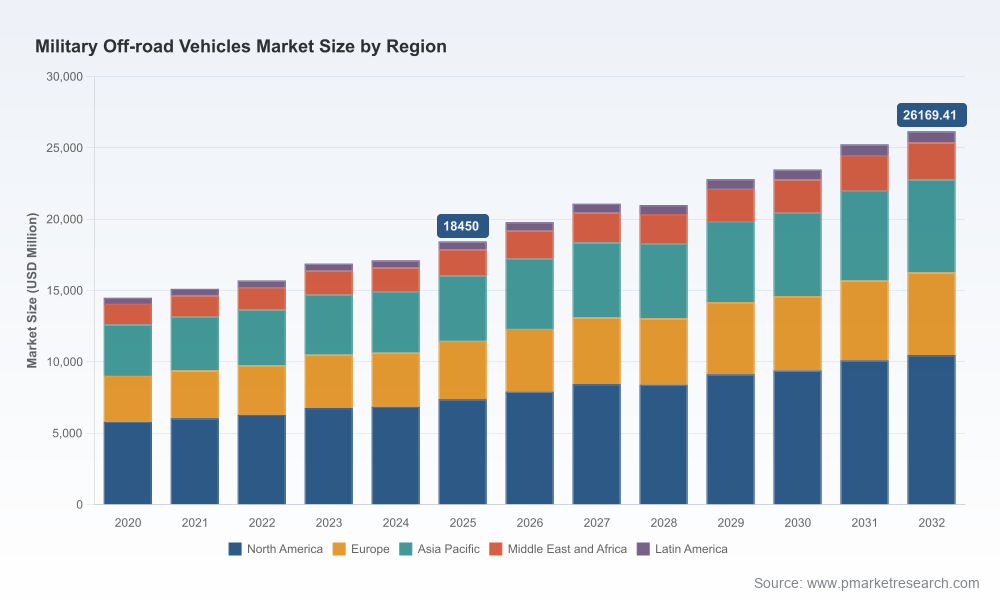

The military off-road vehicles market has returned to steady growth following a period of pandemic-era disruption and near-term procurement churn. Our baseline figures show the market expanding from a 2020 base and reaching an estimated USD 18,450 million in 2025. Under the scenario sets and demand drivers modeled in the report, we forecast the market to grow to approximately USD 19,793 million in 2026 and continue through the 2026–2032 forecast window at a compound annual growth rate (CAGR) of 5.12%, arriving near USD 26,169 million by 2032. These totals incorporate both traditional wheeled tactical platforms and increasingly material contributions from autonomous and hybrid-electric demonstrators.

Worldwide Military Off-road Vehicles Market

Two implications are immediate for 2026 planning cycles: first, growth is meaningful but not runaway—capital allocation must be disciplined and prioritized; second, the composition of that growth is shifting, driven more by capability upgrades, autonomy integration, and supply-chain constraints than by volume-led procurements alone.

Worldwide Military Off-road Vehicles Market

Principal demand and technology drivers

- Capability modernization: Militaries are replacing legacy fleets with vehicles that emphasize survivability, modular protection, and off-road maneuverability while integrating mission systems.

- Autonomy and robotics: Demonstrations and government-sponsored tests (for example, DARPA’s recent RACER platform trials) are accelerating requirements for unmanned and optionally manned ground systems, creating procurement pathways that blend prototypes and scaled deployments.

- Propulsion and electrification: Hybrid-electric designs and power-electronics integration are progressing from demonstrators to program-of-record contenders, but timeline divergence between commercial EV momentum and military operational constraints remains.

- Supply-chain pressure: Fragility in armor-grade steel and critical power electronics is escalating program risk and delivery timelines—steel price volatility alone increased armor production costs materially in recent years.

- Regulatory and operating environment: Military tactical trucks continue to benefit from regulatory exemptions that allow legacy fuel use and engine architectures optimized for operational resilience rather than civilian emissions standards.

Strategic implications for 2026 decision-makers

Our analysis crystallizes five actionable strategic priorities for organizations making 2026 resource allocation decisions.

- Prioritize interoperable, upgradeable platforms: Investments should be made into base vehicle architectures that support modular mission kits, electronic architecture growth, and future autonomy retrofits—minimizing lifecycle cost and technical debt.

- Plan for staged autonomy adoption: Procurement strategies that blend mature manned platforms with pilot autonomous inserts (squad-level scouts, logistics convoys) will yield better operational outcomes than trying to leap straight into fully autonomous fleets.

- Secure supply-chain resilience: Near-term sourcing and inventory plays for armor steel and power-electronics components are essential—buyers who execute strategic buffer buys or dual-source agreements will reduce schedule risk.

- Reconcile propulsion trade-offs: Military exemptions from civilian emissions regulations remove some constraints on fuel choices and engine staging; however, long-term cost of operations and theater logistics make hybridization a strategic hedge rather than a universal immediate replacement.

- Embed industrial and procurement agility: Given the forecasted moderate growth and concentrated supplier base, competition for contracts will favor firms that can demonstrate rapid prototyping, predictable manufacturing cadence, and documented supply-chain mitigation.

Competitive landscape—who matters and why

The market exhibits moderate concentration. Our concentration metrics indicate that the top three suppliers account for roughly 42% of the addressable market, and the top five approximate 58%—a structure that supports both incumbent strength and targeted disruption. Below we summarize strategic postures and near-term vectors for the most consequential firms covered in the report.

- Oshkosh Defense (Oshkosh, WI) — Sustained leadership through combat-proven platforms. Their JLTV family and TAK‑4i suspension approach continue to set expectations for protected, high-mobility light tactical vehicles. Oshkosh’s roadmap emphasizes incremental upgrades and proven field performance—an advantage in risk-averse procurement environments.

- AM General (South Bend, IN) — The HUMVEE lineage and recent JLTV A2 variants position AM General as a specialist in high-mobility light vehicle families. Their differentiation lies in ruggedization and field-serviceability in austere theaters.

- General Dynamics Land Systems (Sterling Heights, MI) — A focus on platform survivability and systems integration, including explorations in hybrid-electric demonstrators, gives GDLS leverage in higher-end tactical and armored wheeled markets where integration complexity is paramount.

- BAE Systems (London, UK) — Strong in armored wheeled vehicles and MRAP derivatives, BAE’s strength is in protection-centric solutions and global sustainment footprints for institutional customers.

- Rheinmetall AG (Düsseldorf, Germany) — Modular, multi-role wheeled platforms (e.g., Boxer/Lynx family derivatives) underscore Rheinmetall’s capability to migrate chassis into a wide set of mission pods for troop transport and support roles.

- GM Defense (Detroit, MI) — Investing in the next generation of tactical vehicles, including hybrid platforms, and actively demonstrating tactical light vehicles internationally, positioning itself as an innovation-led challenger for new procurements.

- Navistar Defense, Iveco Defence Vehicles, Mack Defense, Arquus, Tata Motors, Hanwha Defense — Each plays a distinct role by emphasizing logistics trucks, regionally dominant platforms, or specialized configurations. Their competitive playbooks often focus on cost competitiveness, regional industrial partnerships, and tailored sustainment packages.

Recent vendor and program developments illustrate the competitive dynamics: GM Defense’s public demonstrations in the UK indicate an acceleration of international market engagement; Oshkosh continued public showcasing of JLTV capabilities at industry conferences; DARPA’s RACER tests demonstrate growing operational proof points for complex-terrain autonomous mobility; and government-level selections for integrating autonomy into squad vehicles suggest that prototype-to-program timelines are shortening.

Technology, procurement and industrial considerations

- Autonomy is shifting from lab novelty to procurement line item. But procurement authorities must define realistic IOC timelines and clear capability acceptance criteria—our report maps technical risk to procurement milestones.

- Hybrid-electric and power-electronics integration will be selective and mission-dependent. Strategies that pilot hybrids in logistics and command-post roles before front-line combat adoption reduce operational risk.

- Value-capture will increasingly come from software and mission systems rather than raw chassis alone. Contracts that include long-term software support and upgrades change lifecycle economics.

- M&A and industrial partnerships will be tools to close capability gaps quickly—especially for suppliers lacking autonomy stacks or high-performance powertrains.

Supply chain and regulatory headwinds

Two non-technology risks warrant urgent attention.

- Material supply and price volatility: Armor-grade steel and power-electronics constraints continue to create lead-time and cost pressure. Historical swings in steel costs materially increased production expense for armor components in recent years; programs that do not plan for price-protection or alternative sourcing will face performance shortfalls.

- Regulatory exemptions and operational trade-offs: U.S. tactical military off-road trucks retain exemptions from many civilian emissions regulations, enabling operational engine and fuel choices optimized for theater needs (including the continued use of JP‑8 where appropriate). While this preserves tactical performance, it complicates comparisons with commercial electrification roadmaps and can delay force-wide propulsion transitions.

What our full report delivers (high level)

The PW Consulting report goes well beyond high-level forecasts. It is structured as an operational playbook for 2026 decision-making and includes:

- Robust market sizing and baseline reconciliation across 2020–2025, and modeled scenarios through 2032 with sensitivity analyses.

- Segmentation by vehicle class, application, and region (note: this preview omits the detailed segment tables that subscribers will access).

- Supplier benchmarking with capability matrices, program pipelines, and procurement-ready scorecards to inform bid/no-bid and partnership choices.

- Technical risk assessments for autonomy, hybridization, and material substitutes, including timeline-aligned mitigation strategies.

- Supply-chain risk heat maps and recommended mitigations—contractual, inventory, and sourcing measures tailored to minimize schedule slippage.

- Scenario-based procurement playbooks (rapid acquisition, incremental modernization, and long-term recapitalization), with recommended contracting structures for each.

- M&A and JV opportunity pipelines calibrated to buyer synergies and regional industrial strategies.

Conclusion and recommended first steps for 2026

For organizations setting 2026 budgets and roadmaps, the decision framework must balance capability urgency against industrial and supply constraints. Prioritize investments that increase platform flexibility (modularity, open electronic architectures), secure supply-chain continuity for armor and electronics, and adopt phased autonomy pilots with clear acceptance gates. Use the market’s moderate concentration to negotiate favorable industrial partnerships and avoid single-supplier dependencies where possible.

PW Consulting’s full report contains the proprietary segment-level data, vendor-level market shares, pricing models, and procurement templates that enable operational execution. This preview has outlined the strategic contours; the full dataset and playbooks are available to inform specific contracting, R&D, and M&A moves in 2026.

To obtain the complete Worldwide Military Off-road Vehicles Market report—including the detailed segment tables, competitive share matrices, and procurement-ready tools—visit PW Consulting’s published report page or contact our advisory desk for a tailored briefing.

For detailed analysis of this topic, please visit the official page:Worldwide Military Off-road Vehicles Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com