Industrial Alcohol Market Size, Share, Trends, Growth Opportunities, Key Drivers and Competitive Outlook

Other |

2026-07-01 07:50:25

As PW Consulting’s Senior Strategic Advisor and Chief Industry Analyst, I present a concise, decision-focused briefing drawn from our latest Worldwide Deicing Salt Market research (base year 2025). The global market reached approximately USD 2.7 billion in 2025 and—under our mid baseline—is projected to grow at a compounded annual growth rate (CAGR) of 3.55% through the 2026–2032 forecast horizon, reaching just under USD 3.45 billion by 2032. This briefing synthesizes the report’s most actionable takeaways for procurement leaders, operations executives, and corporate strategists preparing plans for 2026, while reserving the granular segment tables and country-level data for the full report.

Worldwide Deicing Salt Market

Deicing salt sits at the intersection of public infrastructure spending, seasonal logistics, commodity supply chains, and environmental regulation. For organizations that procure, store, distribute, or produce deicing materials, small changes in cost drivers, regulation, or service-level expectations can materially affect 12–36 month plans. Our research shows steady baseline demand with cyclical spikes tied to weather and infrastructure renewal, making 2026 a year to lock in medium-term supply resilience while optimizing for rising sustainability constraints and input cost volatility.

Worldwide Deicing Salt Market

Moderate, predictable growth with episodic risk: The market’s mid forecast growth (CAGR ~3.55% through 2032) implies predictable baseline demand, but volatility remains at the margin due to weather-driven usage and occasional logistic shocks. Scenario planning should therefore combine a stable procurement baseline with contingency capacity for sudden volume surges.

Worldwide Deicing Salt Market

Input-cost pressure and energy exposure: Underground mining operations faced higher energy-driven mining costs in 2024 (industry estimates indicate an increase in rock-salt mining costs of roughly 8–12% in 2024), and evaporation-based producers remain sensitive to natural gas prices (North American natural gas averaged about USD 3.50/MMBtu in Q4 2024). Procurement and production teams must embed energy-price triggers into supplier contracts and capital expenditure models.

Packaging and trade friction: Recent trade measures affected packaging costs—imports faced higher container and steel packaging expenses (e.g., US tariff-related effects increased some packaging costs in 2024). Buyers with cross-border supply footprints should re-evaluate landed-cost models and consider near-shore buffering where economically justified.

Regulatory and environmental constraints: Environmental regulation is an accelerating constraint. In parts of Europe, directives limit chloride discharge into waterways, driving procurement toward lower-chloride alternatives in sensitive catchments; in North America, authorities increasingly recommend magnesium chloride blends to mitigate corrosion to infrastructure. These regulatory shifts change product mix economics and can increase the premium for treated or alternative deicers.

Fragmentation and competitive dynamics: The market is neither highly concentrated nor atomized: leading suppliers command meaningful regional advantages but the top players do not dominate globally. This structure rewards differentiated capabilities—logistics excellence, treated-product formulations, sustainability certifications, and coastal evaporation-based capacity.

Procurement: hybrid contracting and dynamic indexing. Adopt hybrid contracts that combine fixed baseline volumes with indexed surge provisions tied to energy and freight indices. Include clauses that allow temporary substitution to lower-chloride blends in environmentally sensitive jurisdictions, with pre-agreed pricing formulas for treated products.

Inventory & logistics optimization. Shift from a strict “just-in-time” posture to a two-tier inventory model: a guaranteed safety stock covering the base season plus rapid-access satellite holdings for surge months. Prioritize multimodal logistics options and evaluate near-term investments in coastal or rail-served storage to avoid container/tariff shocks.

Capex and supplier engagement. Producers should prioritize capital investment in energy efficiency and treated product capacity, while buyers should stage 2026 strategic sourcing reviews to lock favorable capacity from suppliers making such investments. Look for suppliers with verified sustainability certifications and evaporation capacity that can flex to demand.

Product and service innovation. Municipal and airport customers will increasingly value low-corrosion, low-environmental-impact solutions. Invest in pilot projects for blended chemistries, corrosion inhibitors, and application optimization (e.g., calibrated spreading technologies) that lower lifecycle costs and regulatory exposure.

M&A and partnerships. Given the market’s moderate consolidation and pronounced regional strengths, 2026 is an opportunity window for bolt-on acquisitions that secure logistics or treated-salt capabilities—especially for players aiming to expand cross-border presence or to obtain certified sustainable production footprints.

Risk management and scenario playbooks. Build an operational playbook for three weather/market scenarios (mild, average, severe winter) that prescribes procurement triggers, release of surge inventory, and communications protocols with municipal customers to reduce financial and reputational risk.

The competitive field blends large global miners, regional specialists, and state-owned suppliers. Each archetype presents different strategic trade-offs for buyers and investors.

Large diversified producers (e.g., Cargill, Compass Minerals): These firms offer scale, integrated logistics, and product breadth—ranging from raw rock salt to treated salts and liquid brines. Recent moves include capacity expansion and treated-product innovation (for example, a capacity expansion announced in late 2024 and treated salt launches focused on corrosion inhibition). For buyers, scale suppliers reduce availability risk; for competitors, scale raises the bar on service and pricing.

Regional miners and specialty players (e.g., K+S, Ineos, Sudsalz, Cheetham): European and APAC producers are important where logistics cost and regulatory compliance are decisive. Upgrades in environmental management and certifications have become differentiators—K+S’s recent ISO 14001 certification update is a case in point, signaling reduced environmental compliance risk for customers.

State-owned and large-capacity exporters (e.g., CNSIC): These suppliers can offer large volumes from solar-evaporation facilities, providing pricing stability in some corridors but also raising geopolitical and quality considerations for buyers seeking consistency in treated-product performance.

For 2026, supplier selection should emphasize: demonstrated capacity flexibility, evidence of treated-product R&D, verified sustainability credentials, and transparent total-cost-of-supply models that include packaging and tariff impacts.

The PW Consulting report is built for operational use. It includes:

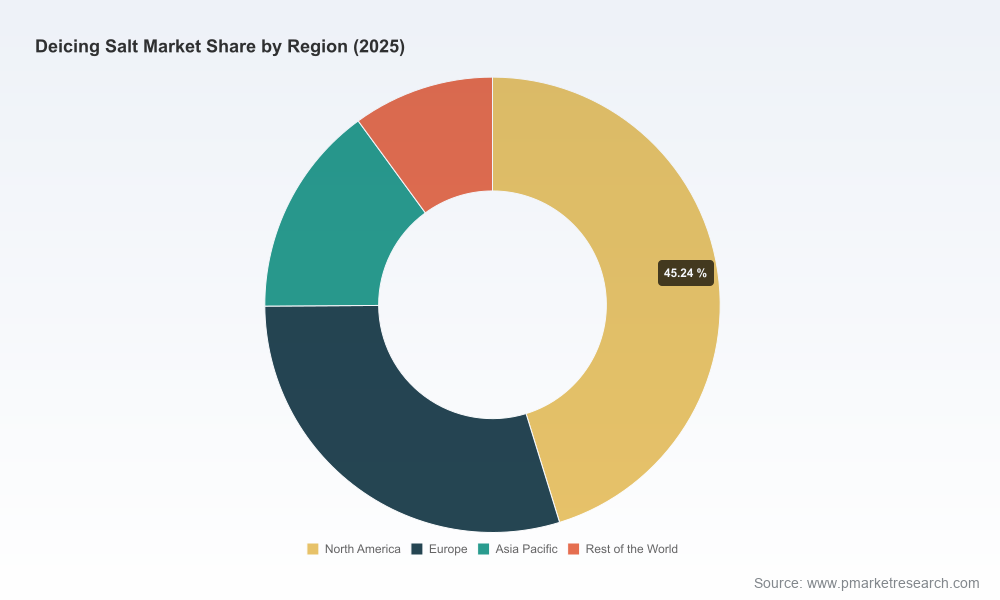

Note: The report contains the full datasets and segment-level tables (regional, product type, and application splits). We intentionally omit those granular figures here—access to the full spreadsheet and appendices is available on the report’s webpage for procurement teams conducting supplier bids or capital-allocation exercises.

For procurement chiefs: Initiate supplier requalification with emphasis on treated-product performance and energy-indexed pricing. Run a two-week tender window with staged awards to secure base capacity and optional surge volume.

For operations leaders: Rebalance inventory strategy to secure at least one seasonal safety buffer and identify two alternative logistics corridors to mitigate container and tariff risks.

For corporate strategists and M&A teams: Screen targets that add treated-salt capability, coastal evaporation capacity, or certified sustainable operations—these will command a pricing premium as regulations tighten.

For public sector purchasers: Define environmental performance specifications early and pilot low-chloride alternatives in sensitive catchments with clear monitoring protocols.

The worldwide deicing salt market in 2026 represents steady, low-single-digit growth but is increasingly shaped by energy costs, packaging and trade dynamics, and environmental compliance. Organizations that pair disciplined procurement frameworks with targeted investments in treated-product capability and logistic resilience will convert a steady market into strategic advantage. PW Consulting’s full report equips decision-makers with the quantitative models, supplier intelligence, and contract tools needed to pursue those opportunities—while our scenario toolset helps translate uncertainty into executable seasonal playbooks.

To review the complete data tables, supplier scorecards, and downloadable modeling tools referenced in this briefing, please visit the report page where the full dataset and appendices are available for licensed subscribers.

For detailed analysis of this topic, please visit the official page:Worldwide Deicing Salt Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com