Worldwide Agricultural Nanotechnology Market: Strategic Implications for 2026 Decisions

As policymakers, corporate strategists, and investors prepare roadmaps for 2026, understanding the trajectory of agricultural nanotechnology is no longer optional — it is a business imperative. PW Consulting’s latest Worldwide Agricultural Nanotechnology Market report synthesizes empirical trends, primary-market interviews, and scenario modeling to deliver a decision-grade picture of where the sector stands today and how it will evolve through the next funding and deployment cycle.

Worldwide Agricultural Nanotechnology Market

Market Trajectory at a Glance

The market for agricultural nanotechnology has moved from early-adopter experimentation toward meaningful commercial adoption. Our topline modeling — calibrated to primary vendor data and field trials between 2020–2025 — shows the market expanding at a compound annual growth rate (CAGR) of 14.03% over the 2026–2032 forecast window. By PW Consulting’s base year (2025), the industry had reached an inflection point, and our forecasts anticipate continued acceleration through the decade, reinforcing the sector’s attractiveness for strategic investment and corporate development programs.

Worldwide Agricultural Nanotechnology Market

Two numbers are particularly useful for leaders taking decisions next year: the market size as observed in the report’s base year and the industry runway implied by our 2032 projection. They together signal both validated demand and significant upside for incumbents and new entrants that can scale safely and credibly.

Worldwide Agricultural Nanotechnology Market

Why This Report Matters for 2026 Planning

- Actionable Investment Priorities: We translate market growth into prioritized investment areas — from scalable production methods to pilot-to-commercialization programs — with clear criteria for near-term capital allocation.

- Regulatory Playbooks: The regulatory environment remains fragmented and precautionary. Our report supplies step-by-step regulatory engagement templates and safety evidence packages designed to shorten time-to-market while managing reputational risk.

- Commercialization Blueprints: We provide practical go-to-market frameworks for field trials, farmer adoption pathways, pricing experiments, and channel partnerships that move pilots into recurring revenue.

- Supply-Chain and Feedstock Strategies: With input-cost and sustainability pressures mounting, the report outlines options to vertically integrate feedstock supply — including conversion of agricultural waste into nanomaterial feedstocks — to secure cost advantages and reduce carbon intensity.

- Risk & Scenario Planning: Given persistent scientific and regulatory uncertainties, we model alternative adoption paths and their financial impacts, enabling executives to stress-test portfolios under conservative, base, and accelerated scenarios.

Competitive Landscape — Who’s Shaping the Field

The competitive map is a mix of specialized innovators, established agrochemical majors, and materials science players. Market concentration remains moderate: our analysis shows leading groups commanding a material but not dominant share, leaving space for nimble innovators and strategic partnerships.

- Specialist Innovators (e.g., Aqua-Yield/Nano-Yield, Indogulf BioAg, Migrow Agro): These firms have demonstrated early commercial traction with nano-fertilizer and nutrient delivery platforms optimized for crop nutrient-use efficiency. Their advantages are speed of iteration and close farmer engagement, but scaling manufacturing and obtaining broader regulatory approvals are recurring constraints. Recognition of Nano-Yield on national growth lists underscores the ability of focused players to rapidly commercialize niche applications.

- Large Agribusiness and Chemical Players (e.g., BASF SE, Syngenta AG): Multinationals are accelerating product development and portfolio integration. Recent initiatives documented in our dataset show rapid advances in targeted pesticide delivery and seed treatment nano-formulations. These players bring distribution scale, regulatory expertise, and R&D budgets that can quickly raise competitive thresholds in core segments.

- Materials & Technology Suppliers (e.g., Nanoshel, Zyvex Labs, Nanoco Group): Pure-play nanomaterials companies are a critical upstream layer. Their technology platforms determine material properties, cost curves, and environmental behavior — all of which directly affect downstream agronomic efficacy and regulatory acceptability.

- Regional & Integrator Players (e.g., Coromandel, Annadata Organic, Ray Nano Science & Research Center): These organizations blend distribution networks with localized R&D, offering valuable on-the-ground testing and farmer adoption channels, particularly in markets where tailored agronomic solutions matter most.

Collectively, the ecosystem is evolving into a landscape where partnerships — licensing deals, co-development, and contract manufacturing — outpace pure organic expansion. Our report includes detailed partnership archetypes and M&A playbooks tailored to different strategic goals (market access, technology acquisition, capacity expansion).

Key Dynamics and Structural Forces

- Integration with Precision Agriculture: Nanotechnology’s most compelling commercial pathway is as an enabler of precision farming stacks. Nano-biosensors for real-time monitoring, nano-enabled seed treatments that respond to digital inputs, and controlled-release formulations tied to decision-support systems are all identified as critical combinatorial opportunities.

- Feedstock Innovation and Circularity: Converting agricultural waste biomass into nanomaterial feedstocks presents a dual opportunity: cost reduction and emissions avoidance. Our supply-side analysis quantifies how feedstock choices influence unit economics and carbon profiles for production at scale.

- Regulatory and Environmental Safety Considerations: Persistent concerns about nanoparticle fate, soil-ecosystem impacts, and long-term exposure drive conservative regulatory postures in several jurisdictions. The report maps current regulatory frameworks, key evidence gaps, and tactical steps companies can take to build defensible safety dossiers.

- Cost vs. Value Communication: Nano-agrochemicals typically carry higher upfront production costs versus legacy formulations. Success therefore depends on demonstrable lifecycle benefits — reduced application frequency, yield uplift, lower downstream environmental liabilities — and on communicating those benefits to farmers and procurement buyers via rigorous field economics analyses.

Strategic Imperatives for 2026 Decision-Makers

Based on our synthesis of market dynamics, competitor moves, and technology maturity, PW Consulting recommends five imperatives for organizations setting strategy in 2026:

- Prioritize Scalable Safety Studies: Invest early in long-term ecotoxicology and soil health studies aligned with regulatory expectations. Being first to publish robust, transparent safety evidence will materially reduce market-entry friction and accelerate acceptance.

- Build Modular Manufacturing Capacity: Favor modular, flexible production footprints that can be scaled with demand and repurposed across material chemistries. This reduces capital risk while enabling rapid product diversification.

- Partner Upstream and Downstream: Secure technology supply (materials and feedstock) and distribution channels (agro-dealers, co-ops, digital platforms) through joint ventures or licensing. Such partnerships are often faster and less capital-intensive than greenfield expansion.

- Embed Into Digital Agronomy: Bundle nanotech products with sensing and decision tools to create measurable farmer-level ROI and to differentiate against commodity inputs.

- Prepare Regulatory Engagement Playbooks: Proactively engage regulators with tiered evidence submissions and real-world monitoring pilots. Anticipatory compliance is a competitive moat in an environment where policy can shift quickly.

What the Report Contains — Practical Deliverables

PW Consulting’s full report is designed to be executable. Highlights include:

- Top-down market sizing and bottom-up vendor validation with scenario sensitivity analyses;

- Commercial playbooks for pilot design, farmer adoption, and channel monetization;

- Regulatory engagement templates and standardized safety dossier checklists;

- Supply-chain blueprints, including feedstock sourcing options and cost curves for scalable nanomaterial production;

- Investment prioritization matrices and M&A playbooks tailored to acquirers, strategic partners, and private equity;

- Competitive benchmarking with capability heatmaps and partner-fit scoring tools.

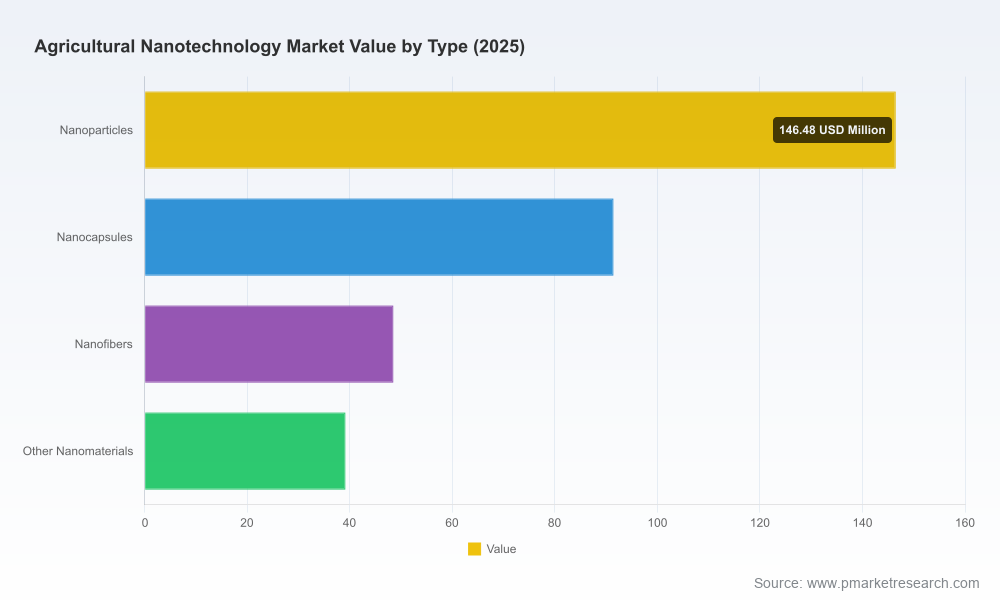

To respect the “trailer” principle, this public executive brief intentionally highlights strategic themes and the report’s practical value without reproducing granular segment-level breakdowns or proprietary vendor-level metrics. The full dataset, including detailed segmentation, per-application forecasting, and vendor revenue benchmarking, is available through our subscription portal and licensing arrangements.

How to Use This Insight in 2026

For CEOs and portfolio managers, the choice in 2026 is between three strategic postures: lead, partner, or follow. Leading requires a sustained investment in safety, manufacturing modularity, and farmer-facing value propositions. Partnering leverages complementary capabilities and mitigates capital exposure. Following — a viable option for some — requires tighter cost control and rapid access to proven third-party technologies.

Our recommendation is pragmatic: treat early-stage nanotech investments as platform bets that must be validated through staged milestones tied to both technical performance and regulatory de-risking. Use the scenarios in our report to align board-level capital allocation with measured commercialization milestones.

Final Note and Next Steps

Agricultural nanotechnology offers a compelling set of levers to improve nutrient efficiency, reduce environmental footprint, and enable new precision farming capabilities. But the window to shape the industry’s structure and standards — through scientific evidence, regulatory engagement, and commercial design — is narrow. PW Consulting’s Worldwide Agricultural Nanotechnology Market report provides the empirical foundation and strategic playbooks to make those 2026 decisions with confidence.

For executives seeking the full dataset, proprietary segment splits, and vendor-level benchmarking that underpin our conclusions, please visit our report page to request access to the complete analysis and licensing options.

For detailed analysis of this topic, please visit the official page:Worldwide Agricultural Nanotechnology Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com