Escorts Jebel Ali +971566048177

Other |

2026-07-01 11:54:19

As studios, exhibitors, integrators and strategic investors plan their 2026 initiatives, understanding the macro arc of the digital movie projector market is now table stakes. PW Consulting’s forthcoming report synthesizes a multi-year data series and forward-looking scenario analysis to convert market signals into board-ready actions. The global market has expanded materially over the past half-decade — rising from roughly USD 1.85 billion in 2020 to about USD 4.41 billion in 2025 — and our baseline forecast projects continued growth through 2032 at a compound annual growth rate of 7.21% (USD denominated, revenue unit: Million). This preview outlines why that trajectory matters, the underlying forces reshaping supplier economics and buyer choice, and the practical decisions our clients should be preparing to make in 2026.

Worldwide Digital Movie Projector Market

2026 is the year several technology, policy and demand vectors converge. Semiconductor and DMD chipset advances unveiled at CES 2026, persistent supply concentration in laser-diode inputs, and large-scale cultural and infrastructure investments in select markets are together compressing opportunity windows while increasing downside risk for unprepared organizations. For stakeholders who need to allocate capex, set procurement horizons, or evaluate M&A opportunities, the questions are straightforward: which illumination technologies will dominate screen deployments, how concentrated will supplier power be, and where should revenue and service investments be prioritized to maximize ROI over a 5–7 year horizon? Our analysis reframes these questions into executable choices.

Worldwide Digital Movie Projector Market

The rapid expansion from 2020 to 2025 reflects a combination of post-pandemic recovery in theatrical attendance, widespread replacement of lamp-based systems with laser illumination architectures, and a premiumization of projection hardware to support HDR and high-frame-rate content. According to our model, the market reached USD 4.41 billion in 2025 and is forecast to rise further in 2026 and beyond, reaching multi-billion-dollar scale through the forecast window to 2032 under the baseline scenario. The 7.21% CAGR across the forecast period is not merely a growth statistic — it encodes the return expectations for manufacturers, the depreciation and refresh cycles for exhibitors, and the timing for complementary investments (e.g., sound, screen coatings, and content mastering).

Worldwide Digital Movie Projector Market

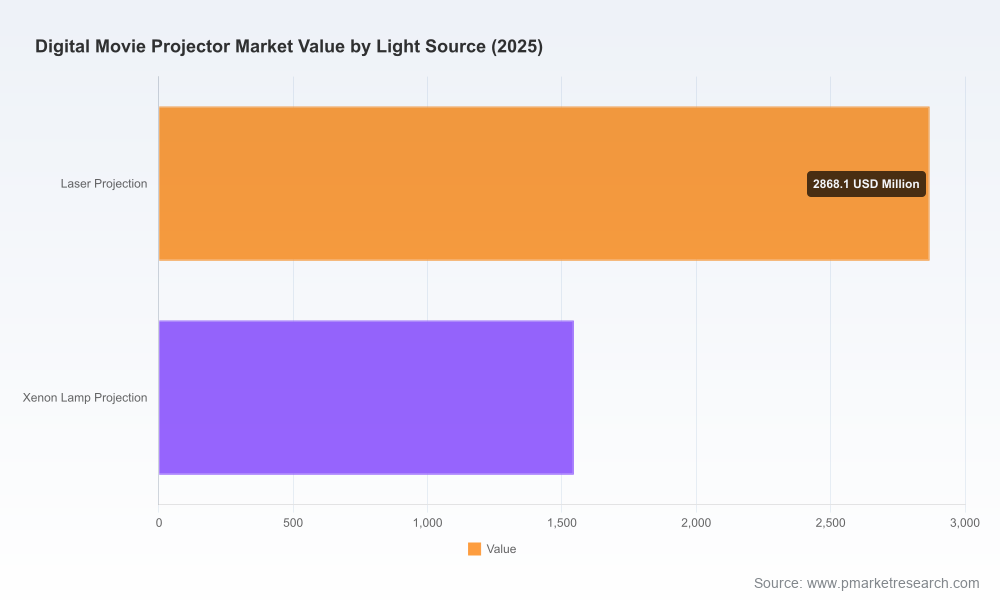

Two additional structural facts are critical for decision-making: (1) market concentration is high among the leading manufacturers, creating pronounced channel dynamics and negotiating leverage; (2) laser-based illumination and advances in DMD/microdisplay technology are reshaping product architectures, spare-parts ecosystems and service models. These dynamics increase the value of forward-looking procurement commitments but also heighten supply chain fragility for those without hedging strategies.

The competitive set is dominated by a small number of global incumbents with differentiated technology stacks and go-to-market models. Rather than recount product names, the strategic implications are what matter:

Recent tactical activity illustrates these dynamics: leading manufacturers expanded laser and Phazer-based product lines in 2025 and 2026, and chipset suppliers showcased next-generation DMDs that make higher-lumen compact projectors commercially viable. For corporate strategy teams, the takeaway is that technological advantage is increasingly a system-level play (illumination + optics + electronics + services), not just a single-component lead.

We translate market intelligence into five pragmatic imperatives that should guide 2026 planning cycles:

Our full Worldwide Digital Movie Projector Market report is built as an executable toolkit for 2026 decisions. Key components include:

For integrators and exhibitors: translate the forecast and scenario outputs into rolling capex plans that balance upgrade urgency with service revenue capture. For OEMs and investors: use our competitive matrices and supply maps to identify capability gaps that acquisitions or alliances can close within an 18–24 month window. For procurement teams: deploy the report’s supplier-risk scoring to inform contract length, pricing floors and penalty structures that protect against component scarcity.

This article intentionally surfaces the strategic contours and actionable implications of the market while withholding the granular segmentation tables and proprietary split data that underpin our bottom-up model. Those detailed breakouts (including regional, light-source and resolution splits by revenue and unit volumes) are part of the full report and are essential for precise contract-level decisions, site-by-site rollouts or transaction modeling. Consider this a trailer: it demonstrates the narrative and analytic rigor you can expect, while directing you to the source for the data you will operationalize.

PW Consulting’s full Worldwide Digital Movie Projector Market report is structured for immediate operational use by strategy, procurement, product and M&A teams planning for 2026. The report includes the detailed segment-level tables, vendor scorecards, downloadable model templates and a bespoke webinar walkthrough. To receive the complete intelligence package and to request a tailored briefing for your executive team, visit the report page or contact our industry practice lead for a confidential consultation.

In a market where technology cycles accelerate and supply-side concentration raises execution risk, the difference between winning and lagging will be set by the speed and rigor of decisions made in 2026. Use the intelligence — and the playbook — to turn that year into a competitive advantage.

For detailed analysis of this topic, please visit the official page:Worldwide Digital Movie Projector Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com