PW Consulting: Textile Chemicals Market Set for 4.8% CAGR Through 2032

Technology |

2026-07-08 08:28:35

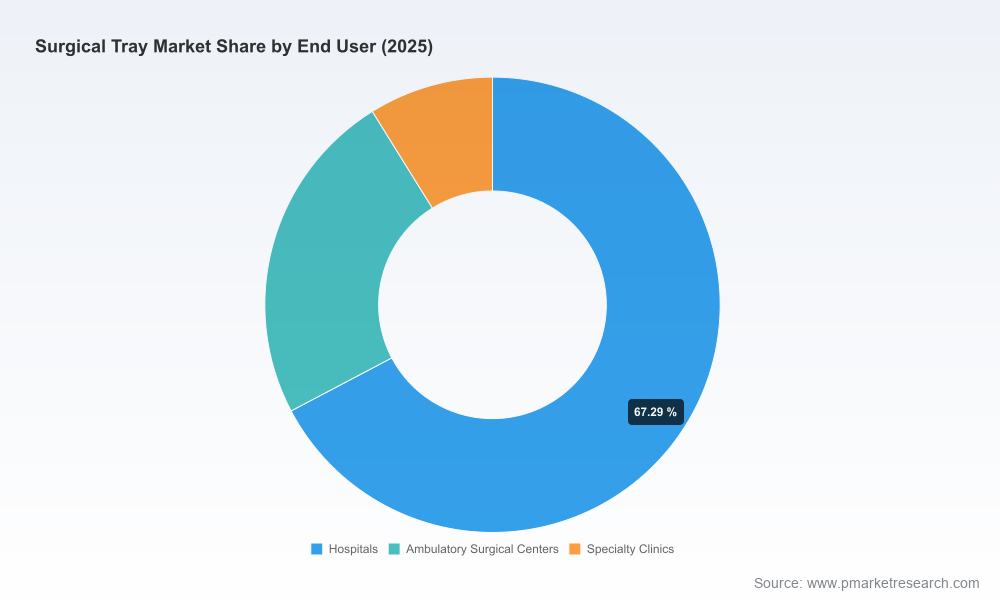

PW Consulting’s latest market study on the Worldwide Surgical Tray Market is designed as a decision-grade briefing for executives preparing plans in 2026. The market has shown steady expansion through the 2020–2025 baseline, reaching an estimated USD 540.2 Million in 2025 and accelerating to an anticipated USD 588.0 Million in 2026. Our forecast period (2026–2032) reflects a compound annual growth rate (CAGR) of 5.81%, with the market projected to approach roughly USD 801.6 Million by 2032. These macro indicators signal a market that is both resilient and receptive to strategic intervention across procurement, manufacturing and service-model innovation.

Worldwide Surgical Tray Market

Timing: The near-term uptick between 2024 and 2026 creates a window for strategic repositioning. Organizations that act in 2026 can capture share as surgical volumes normalize and systems invest in efficiency upgrades.

Worldwide Surgical Tray Market

Margin pressure and unit economics: Persistent upward pressure on raw-material and sterilization-capex costs requires a systematic, data-driven approach to total cost of ownership (TCO) for tray portfolios.

Worldwide Surgical Tray Market

Competitive structure: The market exhibits moderate concentration (CR3 ≈ 34.8%; CR5 ≈ 52.15%), where leading suppliers retain meaningful scale advantages but tangible opportunities exist for niche or service-led entrants.

Regulatory and reimbursement tailwinds: Sterilization standards, device classification frameworks and inpatient reimbursement mechanics are actively influencing buyer behavior—making compliance-driven product differentiation a priority.

Concise market sizing and forecast model (2020–2032) with scenario layers. We provide baseline, upside and downside cases that reflect demand shocks, regulatory shifts and raw-material volatility.

Procurement playbook and TCO templates. Ready-to-deploy RFP language, scoring matrices and a financial model that captures acquisition, sterilization, maintenance and end-of-life costs—enabling a like-for-like comparison of reusable, single-use and hybrid offerings.

Supplier benchmarking and win/loss analysis. Qualitative and quantitative benchmarking of incumbent and emerging vendors across product modularity, sterilization compatibility, supply chain reliability and pricing architecture.

Regulatory & sterilization compliance tracker. A practical checklist mapping ISO 17665-1, AAMI ST79 cleaning requirements and applicable 510(k) pathways to product design and central sterile processing (CSP) workflows.

Operational implementation roadmaps. Step-by-step timelines for pilot deployments, CSP process redesigns and rollouts of asset-tracking technologies (RFID/barcode) designed to preserve sterilization integrity and reduce turn-time.

Risk matrix and mitigation playbooks. Supplier disruption scenarios, raw-material cost sensitivity (including medical-grade 316L stainless steel guidance) and regulatory compliance contingencies with recommended actions.

Executive dashboards & investor snapshots. One-page scorecards for boardrooms and investor committees that highlight key KPIs, break-even horizons for CAPEX investments and payback under varying utilization assumptions.

Primary research appendices. Interview summaries with hospital CSP leads, ASC administrators and OEM product managers—preserving directional insights that informed our conclusions.

Cardinal Health: With a track record of custom sterile procedure trays and recent multi-year supply agreements with large health systems, Cardinal remains a go-to for scale integration into hospital supply chains. Their strength is contract depth and logistics integration—an advantage for customers seeking bundled supply agreements.

Medline: A broad manufacturing footprint across reusable and disposable platforms and ongoing product catalog expansion position Medline to appeal to customers demanding both customizability and sterilization compatibility. Their catalog updates reflect continuous product refinement that reduces switching friction for buyers.

B. Braun: A strong engineering emphasis on modular stainless-steel solutions and container systems supports institutional buyers prioritizing steam and EO sterilization compatibility. Their global presence helps in markets where local regulatory conformity and service networks matter.

Steris: The firm’s recent Harmony Next Generation rigid container launch underscores how sterilization-efficiency features are becoming a key product differentiator. Steris’s positioning is tightly coupled to central sterile processing workflows and capital equipment procurement cycles.

Teleflex (Pilling), Integra, BD and Mölnlycke: These players illustrate the divide between specialty-focused actors and integrated systems providers—ranging from neurosurgery/orthopedics-focused instrument trays to bundled procedure kits for vascular and wound-care use cases. Differentiation is being pursued through specialty depth, modular design and integrated disposables.

Implications: Competitive maneuvers—product launches, contract wins and catalog expansions—highlight two enduring plays: (1) scale and integration to capture institutional contracts; (2) product innovation that reduces lifecycle sterilization cost or shortens turnaround. Given the CR3/CR5 profile, mid-size innovators can still win by coupling product features with services (e.g., tray tracking, validated reprocessing programs) that lower buyers’ operational burden.

Standards & pathways: ISO 17665-1 for moist-heat sterilization, AAMI ST79 cleaning validations and FDA 510(k) classifications collectively determine design constraints and speed-to-market. Devices intended for reusable use must be validated against operational cleaning protocols to avoid unacceptable bioburden thresholds.

Reimbursement overlay: Inclusion of tray-related costs within DRG payments alters buyer calculus—institutions increasingly evaluate trays as a component of procedural cost rather than a standalone purchase, favoring solutions that demonstrably reduce per-case expense.

Material cost sensitivity: Inputs such as medical-grade 316L stainless steel (industry pricing guidance indicates a market band) and sterilization consumables materially affect manufacturing economics. This drives design trade-offs between durability, sterilization throughput and commodity exposure.

Operational friction points: CSP capacity, validated cleaning cycle times and turnover requirements for high-throughput environments (including ambulatory surgical centers) create a demand for designs that reduce handling complexity and support automated reprocessing.

Where to deploy capital: Prioritize modular, sterilization-ready product lines and technologies that enable service revenue (tray-as-a-service, managed sterilization and asset-tracking). These models convert one-time sales into recurring revenue and create switching costs.

M&A playbook: Target acquisitions that add sterilization engineering, CSP service capabilities or digital tracking to accelerate go-to-market. Given the market’s moderate concentration, bolt-on deals that expand service breadth or channel access can unlock disproportionate returns.

R&D prioritization: Invest in materials and coatings that lower cleaning time and corrosion risk, and in designs that streamline set-up time in operating rooms. Compatibility with both steam and EO sterilization is increasingly table stakes for institutional buyers.

Commercial models: Explore outcome-aligned contracts (per-case pricing, guaranteed turnaround) with large health systems and ASC groups—these arrangements transfer operational risk to suppliers but command a price premium and sticky revenue.

Run a rapid TCO pilot in two facilities with contrasting CSP profiles (one high-throughput hospital; one ambulatory center) to quantify savings potential and identify hidden process constraints.

Initiate a regulatory and compliance readiness review focused on sterilization validations and device classification to de-risk procurement decisions and accelerate implementation timelines.

Engage a shortlist of suppliers for pilot contracts that embed performance KPIs (turnaround time, contamination incidents, per-case cost) rather than unit-price alone.

Pursue a targeted M&A scan for small players with complementary sterilization tech, digital asset tracking or specialized surgical-domain expertise to leapfrog internal capabilities.

Secure the full PW Consulting report and executable appendices to access our models, RFP templates and supplier scorecards—these deliverables are designed to be directly operationalized within a 90–180 day horizon.

Our preview provides the strategic contours for 2026 decisions: a market growing at a mid-single-digit CAGR with tangible differentiation driven by sterilization efficiency, service models and regulatory compliance. For procurement directors, product leaders and corporate strategists, the full PW Consulting Worldwide Surgical Tray Market report contains the calibrated models, templates and competitive intelligence necessary to convert insight into action.

To access the complete dataset, segmentation analyses and downloadable toolkits referenced here, visit the PW Consulting report page for the Worldwide Surgical Tray Market. The full report contains the granular segmentation and supplier valuations withheld in this preview to preserve the actionable advantage for subscribers.

For detailed analysis of this topic, please visit the official page:Worldwide Surgical Tray Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com