Worldwide Amino Acid Metabolism Disease Market — Strategic Imperatives for 2026

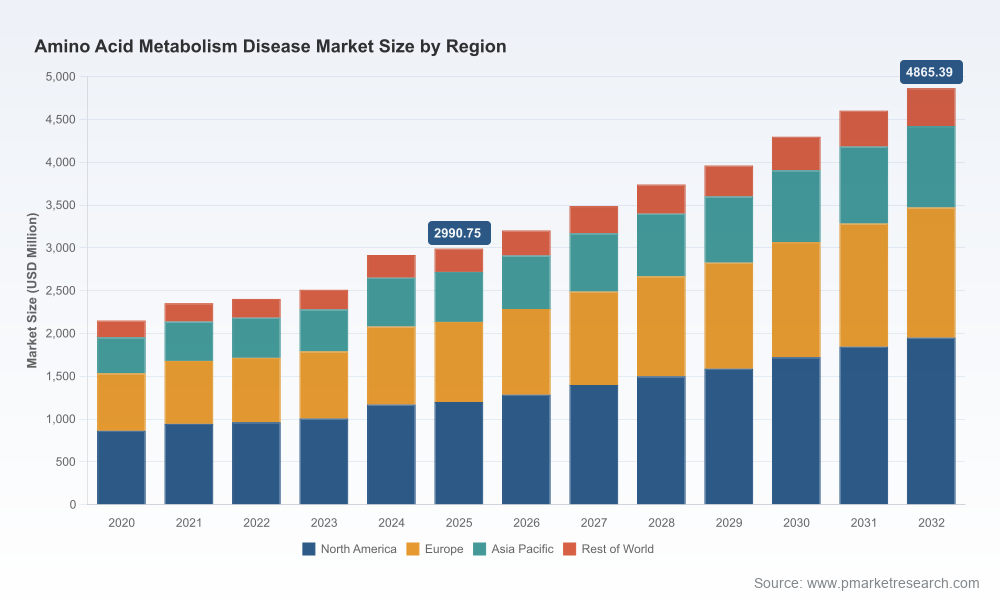

PW Consulting’s latest market intelligence on the Worldwide Amino Acid Metabolism Disease market frames 2026 as an inflection year for biopharma and specialty care investors, product strategists, and health-system planners. Our proprietary analysis shows the market expanding from an estimated USD 2.99 billion in 2025 to roughly USD 4.87 billion by 2032, reflecting a compound annual growth rate (CAGR) of 7.2% across the 2026–2032 forecast window. Those headline metrics matter, but the value for corporate decision-makers lies in the operational playbook and scenario-driven recommendations embedded in the full report.

Worldwide Amino Acid Metabolism Disease Market

Why 2026 Is a Strategic Pivot

Several converging forces make 2026 a critical planning horizon. First, an established base of enzyme replacement therapies, medical foods, and small molecules continues to generate stable revenue while advanced modalities — notably AAV and other gene therapies — progress through late-stage development. Second, regulatory and reimbursement developments are reshaping market access pathways for both incumbent and new entrants. Third, supply-chain and IP dynamics are imposing new constraints and opportunities for manufacturers and specialty ingredient suppliers.

Worldwide Amino Acid Metabolism Disease Market

For executives, this means near-term choices (pipeline prioritization, manufacturing capacity, and payer engagement) will determine who captures the majority of incremental value through 2032. Our report translates the macro growth rate into actionable decisions that align R&D, commercial, and corporate development agendas with realistic timelines and risk profiles.

Worldwide Amino Acid Metabolism Disease Market

What the Report Delivers (Operationally Focused)

- Market sizing and growth trajectories by disease class and treatment modality, with clear implications for market-entry timing and product lifecycle planning.

- Scenario-based financial and operational models that stress-test revenue outlooks under alternative regulatory or reimbursement outcomes.

- Go-to-market playbooks tailored to stakeholder segments (specialty hospitals, metabolic clinics, payers, and patient advocacy groups), including win themes and likely access hurdles.

- Manufacturing and supply-security assessments for critical APIs and medical food inputs, with mitigation pathways for single-source vulnerabilities.

- A prioritized M&A and partnership roadmap — mapping near-term tuck-ins, platform acquisitions, and JV structures that accelerate scale while controlling dilution of core competencies.

- Practical regulatory intelligence: timelines and benchmarks for orphan designations, label expansions, and pediatric formulations that materially affect commercial timing.

Key Market Dynamics Shaping Strategy

- Growth Profile: After steady expansion from 2020 through 2025, the market enters a higher-growth phase driven by better diagnostics, increasing newborn screening coverage in emerging markets, and incremental label expansions for existing therapies.

- Concentration: Market concentration is meaningful but not extreme — the top three players account for roughly 42.5% of reported revenue, and the top five for about 58.8% — creating both defensive advantages for incumbents and realistic disruption opportunities for well-capitalized entrants.

- Modality Shift: Mature categories (medical foods/dietary management) remain revenue anchors today, while enzyme replacement and small-molecule innovations continue to capture share. Gene therapy programs promise step-change value but remain subject to clinical and regulatory timing risk.

- Regulatory & Reimbursement Friction: Orphan designations and label expansions materially accelerate market access, but payer protocols and prior authorization criteria (for example, specific blood biomarker thresholds used in some Medicaid programs) can create unpredictable adoption curves without targeted access programs.

- Supply and IP Chokepoints: Proprietary synthesis routes and patent positions for certain APIs create mid-term supply constraints and pricing leverage for originators until patent expiry dates — a structural factor that should be reflected in sourcing strategies and contract negotiations.

Competitive Landscape — Strategic Takeaways

We profile leading and adjacent players to assess where value is concentrated, who is investing in platform technologies, and which companies are most likely to define standard-of-care shifts over the next three years. Highlights include:

- BioMarin Pharmaceutical Inc.: An incumbent with commercial-scale enzyme and small-molecule assets for PKU and related disorders. Recent label expansions enabling self-administration are commercially significant because they materially lower clinic burden and can expand addressable patient populations. Strategic implication: build differentiated patient support and home-delivery services to capture downstream benefit from self-administration approvals.

- Travere Therapeutics, Inc.: Though best known for kidney-focused assets, recent positive late-stage readouts in studies with implications for cystinuria-related conditions signal adjacent-market mobility. Strategic implication: monitor cross-therapy synergies and consider partnering for distribution in metabolic specialty networks.

- Chiesi Farmaceutici S.p.A.: Maintains a strong position with nitisinone products—their API synthesis approach creates near-term supply barriers for competitors until patent expiries. Strategic implication: assess vertical integration or long-term supply contracts for any program dependent on nitisinone precursors.

- Recordati Rare Diseases: A focused rare-disease player with niche treatments for organic acidurias. Strategic implication: attractive target for specialists seeking product-line depth in metabolic emergency care.

- Takeda / Dimension Therapeutics & AstraZeneca / LogicBio lineage: Both programmatic acquisitions have positioned large-cap pharma to field AAV-based gene therapies for methylmalonic acidemia (MMA) and arginase deficiency. Strategic implication: anticipate premium pricing and specialized center-of-excellence delivery models; preparedness for real-world evidence generation will be a bargaining chip for payers.

- PTC Therapeutics: Active in advancing novel small-molecule approaches for PKU. Strategic implication: small-molecule entrants can achieve meaningful market share if they lower administration burden or cost compared to enzyme therapies.

Recent Developments — Implications for 2026 Planning

- FDA approvals and label expansions (e.g., self-administration permissions) accelerate decentralization of care and shift value to home-care enablement and digital adherence solutions.

- Positive late-stage trial readouts for related indications suggest expanding therapeutic overlap and potential for cross-label strategies.

- Late-stage clinical starts for novel assets raise competition in core indications within a 24–48 month window; companies should determine whether to compete on efficacy, convenience, or economics.

- Orphan Drug exclusivity, patent timetables, and absence of commercial approvals for certain gene therapies create asymmetric windows for upstream revenue capture — a central consideration for licensing and acquisition timing.

Operational Playbook for 2026

- Portfolio Prioritization: Recalibrate R&D portfolios to favor assets that either reduce total cost-of-care or enable clear payer savings. In 2026, payers will reward demonstrable downstream cost offsets.

- Access & Evidence Strategy: Invest in pragmatic real-world evidence programs and early payer engagement. Prior authorization realities mean that clinical-label claims alone will no longer guarantee uptake.

- Supply-Chain Resilience: Secure multi-year supply agreements for proprietary APIs or create contingency synthesis routes. Where single-source APIs exist, consider backward integration or strategic partnerships to avoid supply shocks.

- Commercial Model Innovation: Build hybrid commercial models that couple center-of-excellence referral networks with robust home-delivery and telehealth services — particularly relevant as self-administration approvals expand addressable markets.

- M&A and Alliances: Use the next 24 months to pursue bolt-on acquisitions that expand specialty distribution or add digital therapeutics to improve adherence and outcomes — these often yield faster ROI than large platform buys.

Regulatory, Reimbursement, and Risk Considerations

Regulatory milestones (e.g., orphan designations) materially alter commercial exclusivity and influence valuation assumptions. For example, orphan status can deliver multi-year exclusivity that should be explicitly modeled in pricing and investment decisions. Reimbursement mechanisms — including Medicaid coverage rules tied to biomarker thresholds and prior authorization pathways — are primary gating factors; our report provides templated value dossiers and economic models to support negotiations.

On the risk side, gene therapies remain constrained to clinical use only in certain indications as of early 2026. This creates a timing risk for sponsors and investors: the upside is substantial, but the commercial runway requires careful coordination of manufacturing scale-up, evidence generation, and payer contracting.

How Executive Teams Should Use This Report

- C-suite and corporate development teams: Use the scenario models to stress-test M&A timing and valuation under alternate exclusivity and supply scenarios.

- Chief Medical and R&D Officers: Leverage the clinical and regulatory trackers to prioritize trials with the most favorable access pathways and to accelerate label expansions that meaningfully impact adoption.

- Commercial leaders: Apply the go-to-market playbooks to redesign launch sequences, pricing strategies, and patient-support investments.

- Manufacturing and supply executives: Adopt the supply-security recommendations to reduce single-point-of-failure risks for critical APIs and medical food inputs.

Conclusion — A Tactical Roadmap, Not Just a Forecast

The macro outlook — from approximately USD 2.99 billion in 2025 to about USD 4.87 billion by 2032 at a 7.2% CAGR — signals robust opportunity. But strategy must be actionable: our full report converts that headline growth into prioritized, time-bound moves across R&D, commercial, and corporate development functions. We deliberately present high-confidence recommendations that executives can implement in 2026 to capture disproportionate share of the market’s upside.

Note: This release highlights the analytical framework, strategic levers, and competitive intelligence central to PW Consulting’s research. Detailed regional and disease-type segmentation, revenue breakdowns by treatment category, and the full dataset supporting our scenarios are intentionally reserved for the complete report and interactive dashboards available through PW Consulting’s publications portal.

For organizations preparing 2026 budgets or refining three-year growth plans, the full Worldwide Amino Acid Metabolism Disease Market report is designed to be an operational guide — not just a forecast. Contact PW Consulting or visit our website to access the complete study, granular datasets, and bespoke advisory services tailored to your strategic priorities.

For detailed analysis of this topic, please visit the official page:Worldwide Amino Acid Metabolism Disease Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com