Global Digital Diagnostics Market Forecast and Competitive Analysis 2034

Health |

2026-07-13 15:27:56

PW Consulting's newest market research brief provides a strategic, actionable compass for corporate leaders, project developers, investors and policy teams preparing to make critical hydrochar-related decisions in 2026. Grounded in five years of historical tracking (2020–2025) and a granular forecast through 2032, the report synthesizes technology, feedstock, regulation and commercial dynamics to reveal where value will accrue—and where avoidable mistakes are most common.

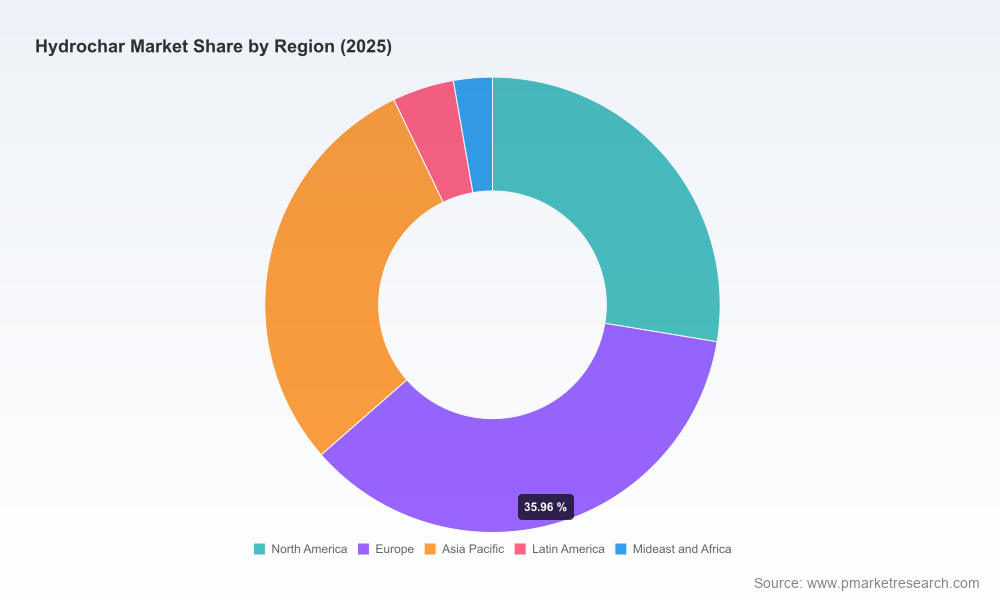

Worldwide Hydrochar Market

Hydrochar has graduated from niche research labs to industrial deployment as operators and utilities seek scalable pathways to decarbonize energy and recycle wet organic residues. Our market model shows a steady expansion from an assessed global market of approximately USD 195 million in 2020 to USD 285.5 million in 2025, with continued acceleration under multiple adoption scenarios. By 2032 the sector is expected to exceed USD 500 million, reflecting an 8.5% compound annual growth rate across the 2026–2032 forecast window.

Worldwide Hydrochar Market

These macro dynamics are reinforced by three structural drivers: (1) regulatory pressure on organic waste management in major markets, (2) compelling material and energy properties of hydrochar, and (3) growing commercial pathways for monetizing carbon benefits—especially in markets where ETS schemes or national incentives allow hydrochar co-firing and carbon crediting.

Worldwide Hydrochar Market

Methodology and model transparency: A reproducible market model built from historical shipments, project announcements, plant capacities, and feedstock availability. The report provides scenario runs (base, policy-up, technology-acceleration) and a clear sensitivity matrix for carbon pricing, feedstock gate fees and energy prices—enabling CFOs to stress-test investment cases.

Commercial playbooks: Go-to-market templates for three archetypal players—technology licensors/OEMs, project developers/independent power producers, and feedstock aggregators. Each playbook includes contracting templates (offtake, feedstock supply), capex/opex benchmarking, and a roadmap for pilot-to-commercial scale-up.

Technology and unit economics: Comparative techno-economic assessments for dominant hydrothermal carbonization (HTC) and emerging process variants (including electrified and heat-integrated lines). The section contains CAPEX and OPEX ranges, break-even offtake prices under different carbon credit assumptions, and optimisation levers (e.g., water recycling, heat integration, pelletisation).

Regulatory and carbon frameworks: A legal and policy primer mapping EU and leading national regulations that materially affect project viability, plus an executable checklist to secure carbon revenue recognition for co-firing and negative emissions claims.

Investment and partnership playbook: M&A target scoring, JV structures, and exit pathways for 2026-2028 execution windows. The report highlights optimal capitalization structures for greenfield plants versus technology roll-outs via licensing.

Operational risk matrices and QA/QC protocols: Feedstock variability diagnostics, emissions and leachate control points, product specification templates, and pilot-to-scale acceptance testing procedures to ensure repeatable material quality for soil amendment or fuel markets.

Case studies and supplier matrix: Confidential commercial diligence on representative projects, and a vetted supplier list for balance-of-plant, pelletising, and emission control—useful for procurement and O&M planning.

The hydrochar industry remains early-stage and geographically fragmented: the three largest suppliers hold under one-third of the market by revenue (CR3 ~28.5%), and the top five collectively account for a minority share (~35.2%). That fragmentation creates windows for regional consolidation, technology licensing and differentiated service models. PW Consulting’s competitive profiles synthesize technology maturity, feedstock focus, commercial traction and strategic intent for the leading active companies.

Ingelia (Barcelona, Spain) — Specialises in HTC plants processing sewage sludge and biowaste into hydrochar for fertilizer and fuel use. Notable milestone: commercial plant start-up in Italy announced in November 2022. Ingelia’s strength lies in municipal market access and sludge handling expertise—advantages for operators seeking a feedstock-linked route to scale.

TerraNova Energy GmbH (Münster, Germany) — Developer of HTCycle industrial-scale technology. Recent commercial partnership for a high-capacity HTCycle installation underlines TerraNova’s ambition in the industrial biowaste segment. Their engineering-first approach suits large project EPCs and utility partnerships.

BlackCarbon GmbH (St. Pölten, Austria) — Produces hydrochar from wood waste and agricultural residues, positioning it as a drop-in coal replacement for industrial boilers. Facility scale-up in 2023 signals appetite among industrial heat users for near-term fuel substitution strategies.

Arbaflame A/S (Aarhus, Denmark) — Focused on pelletised hydrochar for co-firing in power plants. Their product strategy is aligned with utilities seeking logistic-compatible bio-coal alternatives.

Haffner Energy (Vitry-le-François, France) — Operates an ERC process producing SynChar from wet waste; pilot certification in 2022 demonstrates technical validation for small-scale energy and carbon storage use-cases.

Antaco (Santiago, Chile) — Regional player producing hydrochar from forestry residues and sewage sludge for local soil amendment and biofuel markets; representative of distributed, feedstock-proximate business models that are attractive in emerging markets.

Policy timing is decisive. Regulatory measures such as extended biowaste collection mandates in major jurisdictions and the inclusion of hydrochar co-firing within ETS frameworks materially change revenue and offtake math. Companies that align pilot and permitting timelines with policy windows can capture premium carbon and gate-fee economics.

Feedstock scale and quality create winners. Large pools of wet biomass residues exist in several regions—our assessment flags supply aggregation and logistics as a primary barrier to scaling. Technical yield metrics (typical carbon yield in the 70–80% range and energy densification towards ~25 MJ/kg for many hydrochar products) determine product-market fit between soil amendment and fuel pathways.

Value chain capture matters. Firms focused purely on equipment licensing earn different margins and face different risks than vertically integrated players that control feedstock sourcing, fuel processing and offtake contracts. Our scenarios quantify how margin pools shift across these models under varying carbon pricing and energy price assumptions.

Financing sophistication will be required. Lenders and sponsors increasingly demand verified lifecycle analyses, traceability of feedstock and robust offtake or gate-fee structures before committing. Projects that can demonstrate repeatable product quality and low counterparty risk will secure preferential financing terms.

Geopolitical demand reshuffles opportunities. National decarbonisation plans—such as targets for biomass energy share—create import and export dynamics that can alter the optimal siting of capacity. For example, demand-side growth in major Asian markets creates potential export volumes for producers in Europe and Latin America.

Prioritise modular scale-up over premature consolidation. The cost of error rises with size—start with a well-instrumented demonstration plant and secure repeatable product specs before committing to multi-tens-of-thousands tpy capacity expansions.

Lock in feedstock and carbon revenue lines. Negotiate multi-year feedstock agreements with flex provisions and structure offtakes to capture both energy and carbon value streams where regulatory recognition exists.

Design financing around verification. Allocate budget for third-party lifecycle assessments, QA/QC labs and traceability systems to satisfy both carbon market registries and institutional lenders.

Develop dual product strategies. Keep optionality between soil amendment and fuel markets to manage price cycles—product differentiation (pelletisation, particle-size control, ash content) will materially expand buyer sets.

Monitor policy windows and align permitting pathways. Time the commercial ramp to match expected regulatory shifts that unlock carbon revenues—delay can materially reduce IRRs even when technical fundamentals are strong.

Our full report goes beyond this strategic preview. PW Consulting provides an integrated set of deliverables that operational teams can use immediately: detailed model files, plant-level TEA templates, sample offtake and feedstock contracts, jurisdictional permitting checklists and a ranked supplier shortlist with procurement guidance. The preview you are reading highlights high-level contours and priority actions—but omits the granular segment tables, regional split dynamics and project-level numbers that are essential to underwriting a binding investment decision. Those detailed analytics are available in the full report and associated model package.

Hydrochar offers a pragmatic route for industry and waste managers to convert wet organic residues into value while contributing to decarbonisation goals. The market is maturing rapidly: from a modest base in 2020 and steady growth through 2025, the sector is on a trajectory to more than double by 2032 under the baseline case. For executives making strategic choices in 2026—whether to invest, partner, license technology or secure feedstock—the combination of policy timing, technical yield, feedstock logistics and verified carbon value will determine winners and laggards. PW Consulting’s full Worldwide Hydrochar Market report is designed to be the operative playbook for that moment.

For access to the complete dataset, segmented forecasts, and our executable templates, visit the PW Consulting report page and download the full Worldwide Hydrochar Market package.

For detailed analysis of this topic, please visit the official page:Worldwide Hydrochar Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com