Best Plastic Surgeon in Dubai for Botox with Modern Beauty Enhancement

Health |

2026-07-08 09:40:32

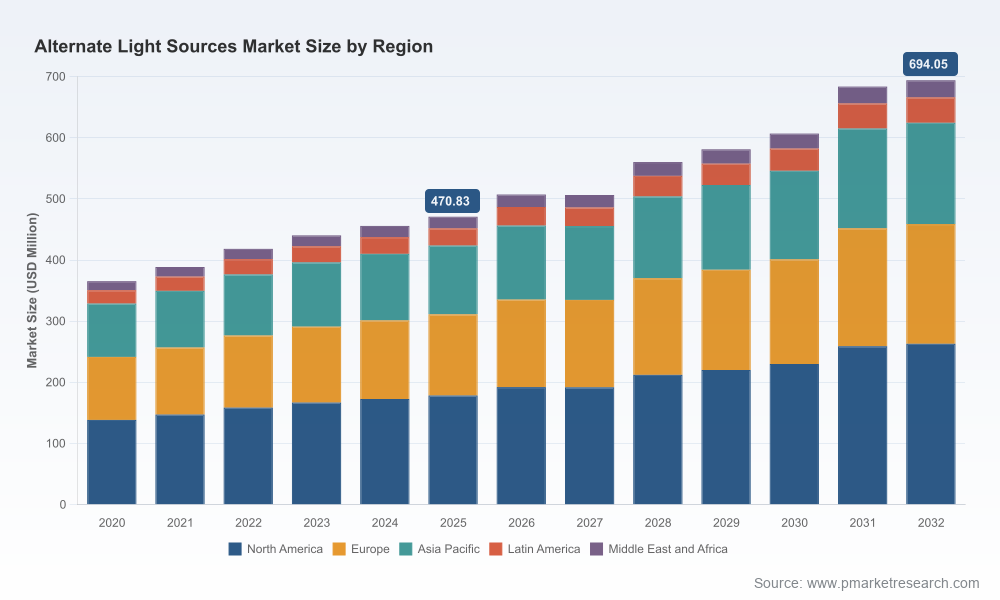

As forensic practitioners, procurement officers, and investors prepare budgets and roadmaps for 2026, the Worldwide Alternate Light Sources (ALS) market is presenting a mix of steady expansion, evolving technical priorities, and regulatory-driven product expectations. PW Consulting’s latest market study — with base year 2025 and a forecast horizon through 2032 — synthesizes five years of historical observation (2020–2025) and forward-looking scenario analysis to turn raw market movement into actionable choices. Our analysis finds the global ALS market rising from a mid‑hundreds million USD base in 2025 and tracking toward a materially larger market by the end of the decade, with a compound annual growth rate (CAGR) of 5.72% over the forecast period. This briefing highlights the strategic value of the report for decisions you must make in 2026, while intentionally withholding segment level line‑items to encourage direct consultation of the full report for procurement and competitive playbooks.

Worldwide Alternate Light Sources Market

Between 2020 and 2025 the ALS market experienced durable growth, driven by increased crime‑scene investment, wider adoption of LED technology, and expanding non‑forensic applications in medical diagnostics and industrial inspection. The market size in 2025 stood at approximately USD 470.8 Million (revenue unit: Million USD). Our base-case outlook anticipates continued expansion in 2026 and through 2032, with the market reaching a substantially higher level by 2032. The forecasted CAGR of 5.72% reflects a market that is neither nascent nor fully mature: it is large enough to attract sustained supplier investment, yet dynamic enough to reward targeted differentiation.

Worldwide Alternate Light Sources Market

Importantly for 2026 planning cycles, the dataset indicates a short window where technology refresh budgets, procurement timetables, and standards alignment will intersect. Buyers planning equipment replacement or laboratory upgrades in 2026 will find vendors actively marketing next‑generation LED and compact laser systems; vendors will also be fine‑tuning service bundles to capture after‑sale revenue. The implication is clear: decisions taken this year will set product and partner trajectories for the next five-to-seven years.

Worldwide Alternate Light Sources Market

Technology consolidation around LED and portable systems: LED‑based handheld and laboratory ALS solutions have emerged as the dominant architecture for crime‑scene and lab use. This is reflected in product roadmaps, vendor R&D prioritization, and the cost‑performance calculus of public‑sector buyers seeking durable, battery‑operated kits.

Regulatory and standards tailwinds: National and international guidance is increasingly explicit about ALS use, documentation, and safety. For example, authoritative glossaries and program lists now codify ALS equipment definitions and recommended kit components; homeland security equipment lists identify portable forensic light kits as standard issue for certain law enforcement tasks. Compliance with photography and evidence documentation guidance further raises the bar for vendor verification, especially in laboratory and judicial contexts.

Safety and training requirements: Shortwave ultraviolet components remain a safety consideration — manufacturers and users must invest in PPE and training for safe operation. The combination of product complexity and legal defensibility is elevating demand for validated workflows, calibration services, and operator credentialing.

Wide price dispersion and market breadth: The ALS landscape ranges from very low‑cost tools to specialized, high‑performance units and laboratory systems — a span confirmed by independent landscape studies showing price bands across multiple orders of magnitude. This creates attractive entry points for new vendors, but also entrenches value propositions for premium suppliers who bundle validation, service, and documentation capabilities.

The ALS market is characterized by a mixture of specialist forensic vendors, optics and scientific instrument companies, and a cohort of ruggedized lighting OEMs targeting first responders and field investigators. Market concentration data indicate a meaningful role for established vendors while leaving room for niche innovation and selective partnerships. Below we summarize the strategic posture of several market leaders covered in our study (company profiles and URLs are provided for reader follow‑up):

Foster + Freeman (United Kingdom) — Known for high‑intensity LED forensic light sources under the Crime‑lite family, Foster + Freeman combines multi‑wavelength laboratory systems and specialized laser units with a reputation for forensic validation and laboratory workflows. Their productization strategy emphasizes evidence screening throughput and multi‑spectral capability.

Labino AB (Vallentuna, Sweden) — A specialist in waterproof, user‑friendly ALS kits designed for crime‑scene investigators. Labino’s product approach prioritizes field reliability and simple operation, appealing to agencies seeking low‑friction deployment. Their 2025 product catalog updates signify a steady refresh cadence aimed at field usability.

Sirchie (United States) — A broad supplier to law enforcement with an ALS catalogue ranging from compact shortwave UV tools to larger 3‑watt systems. Sirchie plays to the tactical and operational buyer, emphasizing ruggedization and kit completeness.

HORIBA Scientific / SPEX Forensics (United States) — Plays at the intersection of laboratory instrumentation and forensic imaging, offering LED handscopes and bench units suited to rigorous lab documentation and research applications.

FoxFury (United States) — Focuses on rugged, cordless forensic lighting and ALS kits tailored for scene safety and mobility. Their strength is in hardware robustness and power management for extended field operations.

Lynn Peavey Company & UltraLite ALS (United States) — Distributors and focused ALS product providers who serve a wide network of forensic practitioners, offering portable kits and integrated supply chains for evidence processing.

Recent product and catalog activity from Labino (product folder release in January 2025) and Foster + Freeman (new Crime‑lite variants spotlighted in April 2025) underscores vendor efforts to refresh portfolio positioning ahead of procurement cycles. Buyers should expect incremental product improvements focused on multi‑wavelength consolidation, battery life, and integration with photographic workflows.

For public‑sector procurement officers: Prioritize total cost of ownership and validation over headline device cost. Require vendor documentation that maps wavelength selection to forensic evidence types, includes barrier filter compatibility, and provides safety protocols for UV components. Structure RFPs to favor kits with clear service-level agreements and training bundles rather than equipment alone.

For forensic laboratory managers: Integrate ALS procurement with imaging workflows and evidence management systems. Seek devices that simplify reproducible documentation — tripod interfaces, aperture control guidelines, and wavelength‑specific SOPs reduce courtroom risk and improve throughput.

For vendors and OEMs: Differentiate on validation, documentation, and after‑sales. The market rewards firms that offer packaged compliance support (e.g., calibration services, operator training, and traceable documentation). Consider modular product strategies that allow field kits to interoperate with lab imaging systems.

For private investors and M&A teams: Look for targets that combine strong forensic domain credibility with scalable manufacturing and service platforms. Firms that can compress time‑to‑validation for judicial acceptance or that offer recurring revenue via consumables and calibration services are particularly attractive.

Our scenario analysis identifies several upside and downside risks that should be modeled in 2026 planning:

Upside scenarios: Faster-than-expected adoption of validated ALS protocols in developing forensic markets; improvements in LED and battery technology that drive premium share; and adoption of ALS‑enabled diagnostics in adjacent medical applications.

Downside scenarios: Heightened regulatory burdens around UV safety that increase procurement friction; commoditization driven by low‑cost entrants that depresses margins; or a shift in evidence‑collection methodologies that diminishes some ALS use cases.

Given the market’s moderate level of concentration—where a group of established vendors hold significant share while specialist players populate the long tail—strategic flexibility matters. Buyers and suppliers that anticipate short-term consolidation and longer-term technological migration will fare best.

The full study provides the operational detail and data necessary to convert the strategic guidance above into a procurement or investment plan. Key components include:

Detailed forecasting and sensitivity analysis across multiple scenarios for 2026–2032, including technology adoption curves and service revenue projections.

Vendor benchmarking with product feature maps, validation evidence, and go‑to‑market assessment. (Note: the report preserves full regional and application splits behind our data wall to protect competitive value — high‑resolution tables are available in the paid package.)

Regulatory and standards compendium that compiles relevant guidance — from official equipment lists to photography and documentation standards — and translates them into procurement checklists.

Operational playbooks — RFP language templates, evaluation rubrics, and supplier negotiation tactics tailored to law‑enforcement, laboratory, and private‑sector buyers.

2026 represents a pivotal year for ALS market participants. Budgets allocated or deferred this year will influence product roadmaps, vendor market share, and the institutionalization of validated forensic workflows. PW Consulting’s report equips decision‑makers to navigate the tradeoffs between short‑term cost savings and long‑term evidentiary rigor, and to seize opportunities created by technological and regulatory shifts.

To access the full dataset, vendor scorecards, and downloadable procurement templates — including the region‑ and application‑level splits we intentionally summarized here — visit PW Consulting’s report portal. For tailored briefings and scenario modelling specific to your organization’s role in the ALS ecosystem, contact our forensic technology practice for a confidential consultation.

For detailed analysis of this topic, please visit the official page:Worldwide Alternate Light Sources Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com