Top 7 Places to Buy Aged verified LinkedIn Accounts and ...

Film |

2026-07-07 09:20:41

By PW Consulting — Senior Strategic Consultant & Chief Industry Analyst

Worldwide Occlusion Spray Market

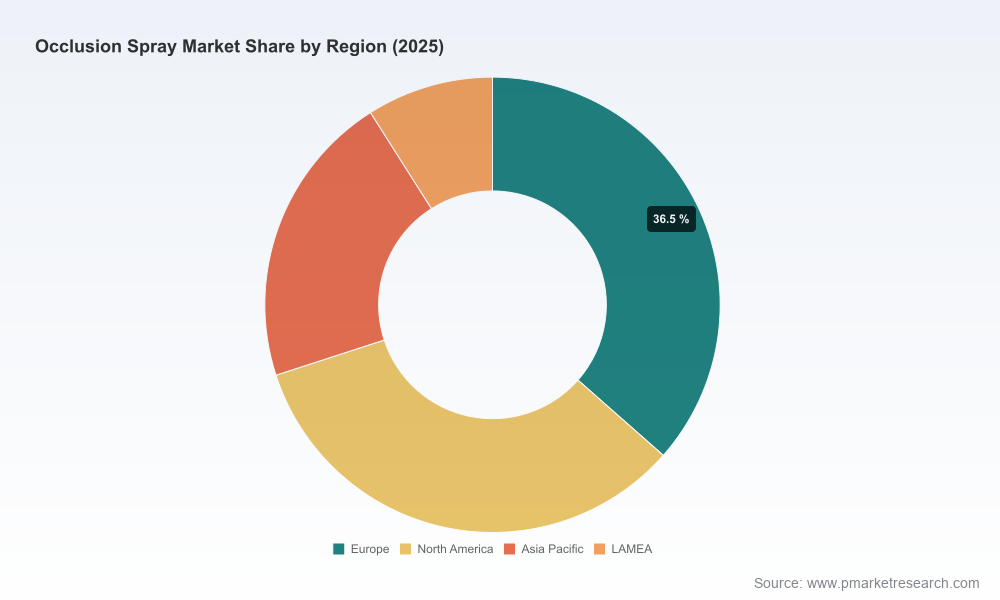

The Worldwide Occlusion Spray Market is on a steady expansion trajectory, driven by incremental adoption in dental and prosthetic workflows, the proliferation of intraoral and extraoral scanning practices, and continued supplier innovation in formulations and delivery systems. Our latest market-sizing indicates a clear upward trend: from an estimated USD 104.2 Million in 2023 to USD 115.45 Million in the base year 2025, with projections showing continued growth to USD 165.72 Million by 2032. This represents a compound annual growth rate (CAGR) of approximately 5.28% across the forecast horizon.

Worldwide Occlusion Spray Market

For executives and strategy teams preparing 2026 plans, these topline dynamics translate into tangible strategic choices — where to invest, which capability gaps to prioritize, how to structure go-to-market, and where to anticipate regulatory or channel friction. This release summarizes the actionable thinking in PW Consulting’s full report while intentionally withholding certain granular segmentation tables to encourage direct engagement with the source for complete details.

Worldwide Occlusion Spray Market

Several structural forces will influence how companies should position themselves in 2026:

This research is constructed for decision-makers who need more than descriptive analysis. Key actionable components include:

The occlusion spray market features both specialized dental suppliers and general laboratory-consumable players. Below is a synthesis of the competitive set covered in our analysis and the strategic implications for 2026.

Known for an intraorally approved aerosol indicator spray tailored to marking occlusal contacts in wet or dry fields. Pascal’s positioning around intraoral safety and clinical precision makes it a strategic partner for restorative clinics focused on chairside workflows. For competitors, the lesson is clear: regulatory-validated intraoral claims materially affect purchasing decisions in clinical settings.

Bausch offers a multi-color articulating spray family that emphasizes thin, removable film properties and compliance with regional medical-device directives. Their broad color portfolio and regulatory alignment strengthen their presence in both labs and clinics. Suppliers aiming to compete should prioritize demonstrable environmental credentials and clinician-facing ease-of-use.

Renfert’s occlusion sprays focus on clear delineation of high spots on model castings and restorations. Their reputation in model-centric workflows positions them well with dental laboratories and technicians. Competing strategies include developing formulations optimized for model adhesion and non-discoloration, as well as lab-focused distribution partnerships.

YETI’s water-soluble, color-recognition products cater to prosthetic work where residue removal and surface compatibility are critical. This highlights an important buyer priority: easy cleanup without compromising visual clarity. New entrants should consider formulation trade-offs between solubility and scan-readiness.

DFS Diamon’s offering emphasizes insolubility and color stability on plaster models — attributes attractive to technicians who prioritize lasting visibility during multiple handling stages. For product teams, this underscores the breadth of sub-segments within the market where differentiated chemistries command premium pricing.

Vacalon’s indicating spray doubles as a digital scan spray, illustrating a bridging strategy between traditional marking and digital scanning workflows. Suppliers who can credibly claim dual-purpose performance will capture a cross-section of digital adopters and legacy users.

Indenco’s multi-SKU, multi-color approach targets both cost-sensitive buyers and practices that prefer vendor choice. For competitors, the implication is that SKU rationalization paired with targeted value messaging can be an effective defense against commoditization.

Regulatory clarity already exists for select articulating sprays in certain jurisdictions, including permissions for intraoral use under established device guidelines. Many established suppliers reference compliance with applicable regional device directives and emphasize physiologically safe ingredients and environmentally neutral propellants. Packaging formats remain dominated by aerosol cans in standardized sizes, though there is variation to meet clinic and laboratory needs. These facts inform supply-chain decisions (e.g., filling capacity, SKU rationalization) and compliance roadmaps for new product introductions.

Our market sizing integrates primary interviews, vendor financials, distributor shipment data, and cross-validated secondary sources. The forecasts incorporate scenario modeling to account for digital-scan adoption curves, regulatory shifts, and potential product discontinuities. Confidence in the near-term trajectory (2026 planning horizon) is high given observable demand drivers and supplier activity, while longer-term projections reflect uncertainty captured in range-bound scenarios.

This article provides a strategic preview intended to inform 2026 planning. The complete Worldwide Occlusion Spray Market report contains the underlying data sets, granular segmentation, pricing matrices, proprietary adoption curves, and executable playbooks required to operationalize these insights. To obtain the full report, supplier benchmarking tools, and tailored advisory sessions, please visit the PW Consulting market portal or contact our research desk.

PW Consulting stands ready to support executive teams in converting this market momentum into measurable strategic outcomes for 2026 and beyond.

For detailed analysis of this topic, please visit the official page:Worldwide Occlusion Spray Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com