noida manpower agency

Networking |

2026-07-12 09:26:45

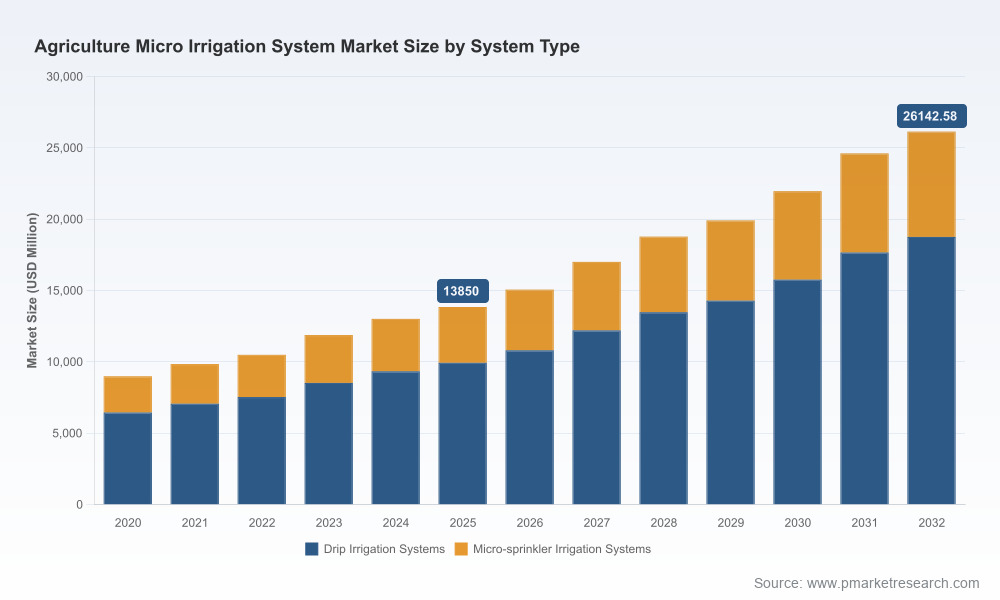

PW Consulting’s latest market intelligence report on the Worldwide Agriculture Micro Irrigation System Market delivers an actionable, executive-level roadmap for companies, investors, and policy makers planning capital and commercial moves in 2026. Built on a robust historical base (2020–2025) and a forward-looking forecast window (2026–2032), the study finds the global market reached USD 13,850 Million in 2025 and is forecast to grow at a sustained 9.5% compound annual growth rate through the projection period. This briefing outlines the report’s strategic value, highlights competitive dynamics, and distills the pragmatic choices leaders must weigh during a pivotal year for adoption, regulation, and supply-chain reconfiguration.

Worldwide Agriculture Micro Irrigation System Market

Macro momentum: A near-double-digit growth trajectory (9.5% CAGR) reflects a structural transition in agriculture — from water-intense practices toward precision water- and nutrient-delivery systems that simultaneously increase yield and reduce resource use. That trajectory creates both scale opportunities and timing risks for vendors, integrators, and financiers.

Worldwide Agriculture Micro Irrigation System Market

Policy and standardization are accelerating adoption: International standards (e.g., ISO 24120-2:2023) and large-scale government investments are making pressurized micro-irrigation an operational and compliance expectation in many markets. Where subsidies and public programs align, adoption curves steepen rapidly — changing addressable markets in months, not years.

Worldwide Agriculture Micro Irrigation System Market

Materials and manufacturing matter: Systems are materially dependent on polyethylene tubing and polymer-based emitters. Volatility in polymer raw material prices, plus rules that condition subsidy eligibility on certified components, mean procurement and local-manufacturing strategies directly influence market access and margins.

Digitalization is redefining product economics: The conflation of hardware (driplines, emitters, filters) with software-enabled fertigation, telemetry and AI-driven dosing converts irrigation vendors into recurring-revenue digital agronomy players — but it raises questions about investment cadence, data ownership and channel conflict.

Market sizing and growth scenarios: A transparent modelling framework built on verified historical data and demand drivers for 2026–2032, including base-case and alternative adoption curves to stress-test capital plans.

Adoption-driver atlas: A granular map of regulatory levers, subsidy programs and farm-level economics that determine uptake speed — including program design features that materially affect vendor eligibility and pricing power.

Technology and product roadmaps: Comparative analysis of system architectures (driplines, micro-sprinklers, emitters, filtration and fertigation integration), with guidance on product modularity, upgrade paths and backward compatibility to protect installed-base monetization.

Supply-chain and raw-material playbook: Risk matrices for polymer inputs, optional hedging strategies, and criteria for localizing production to qualify for subsidies or reduce time-to-market.

Commercial and financing models: Practical structures for channel partners, OEMs and vendors — from lease-to-own for smallholders to service-based agreements for large growers — including example unit economics and sensitivity tests.

Competitive capability maps and M&A screening: Benchmarked profiles of leading incumbents and challenger types, capability gaps, and an M&A prioritization matrix focused on assets that accelerate time-to-scale (manufacturing, digital platforms, distribution).

Note: this briefing highlights the report’s functional components. The full report contains the detailed segmentation matrices, region- and crop-level demand curves, and downloadable financial models required to operationalize strategy; those detailed tables are intentionally withheld here to preserve the value of the full dataset.

Netafim (Orbia): Continues to lead on precision and digital integration, positioning itself around end-to-end fertigation solutions and real-time agronomic optimization. Recent product introductions and strategic partnerships demonstrate a two-pronged approach: (1) premium, software-enabled systems that command recurring value, and (2) partnerships that accelerate field penetration at scale.

Jain Irrigation Systems: Leverages vertical integration and local-market scale to deliver cost-competitive systems, often coupled to subsidy-driven adoption programs. Its focus on ultra-low energy solutions and rice-drip innovations exemplifies how product adaptation to crop and energy constraints unlocks new acreage.

The Toro Company & Rain Bird: Focused on components, filtration and greenhouse solutions; they play to strengths in clog-reduction, reliability and channel depth for specialty agriculture and controlled-environment farming.

Lindsay / Valmont (Valley): Compete on systems integration and large-scale irrigation management. Their strength is in marrying macro-scale water management with precision components — a position attractive to large growers seeking single-vendor accountability.

Rivulis, Hunter, Nelson: Represent modular challengers and regional accelerators — expanding manufacturing footprints and iterating on product ergonomics (e.g., rotator sprinklers, pressure-compensating emitters) to reduce maintenance needs for growers and shorten lead times for distributors.

Market concentration metrics indicate a moderately consolidated landscape (top-three firms account for a significant share, with a broader top-five dominance). This structure favors large incumbents for scale plays, while targeted regional or technology-focused entrants can win by owning niche product architectures, manufacturing, or channels.

Prioritize digital + hardware convergence: Invest selectively in telemetry, AI dosing and fertigation control features that can be monetized as subscriptions or service contracts. The premium on data-enabled agronomy increases lifetime value and creates stickiness across retrofit cycles.

Secure raw-material pathways and local manufacturing: Create dual-sourcing for polymer inputs, consider toll-manufacturing partnerships, or expand regional factories where subsidies or procurement rules (e.g., local-certification requirements) materially affect tender outcomes.

Design market entry around subsidy mechanics: Map subsidy designs to product eligibility (certifications, BIS-type marks) and structure price-package offers that capture the subsidized share of farmer capital outlays while preserving margin.

Adopt a channel-flexible GTM: Blend corporate sales for high-value large farms, dealer networks for mid-sized customers, and fintech partnerships for smallholder finance. Tailor after-sales and agronomic support to each channel to reduce attrition and ensure performance guarantees.

Use M&A and JVs to close capability gaps fast: Prioritize acquisitions that deliver local production, digital platforms or last-mile distribution. Consider joint ventures with local engineering firms or e-commerce players to compress sales cycles (e.g., recent strategic collaborations demonstrate utility of platform partners in accelerating adoption).

Operationalize sustainability and standards compliance: Align product development and field trials to ISO guidelines and national certification routes. This reduces procurement friction and becomes a differentiator in public tenders and corporate ESG commitments.

Adjustments to national subsidy programs and the emergence of new large-scale public investments in irrigation modernization.

Polymer raw-material price swings and the speed at which firms secure localized or long-term supply contracts.

Rate of adoption of international and national standards that change procurement criteria for large installers and government tenders.

New product introductions and factory expansions that alter lead times or local availability.

Strategic partnerships between irrigation vendors and digital or logistics platforms that shorten customer acquisition cycles.

For CEOs, the report provides the quantified growth envelope and scenario-driven stress tests necessary to set R&D and capex budgets for the next three years. For commercial leaders, it supplies subsidy maps, channel segmentation and pricing playbooks to accelerate quarter-over-quarter penetration. For corporate development and private equity, the M&A prioritization matrix and valuation sensitivity models fast-track candidate screening and integration planning. For policy advisors, the document decodes how standardization and subsidy design change adoption economics and ultimately water security outcomes.

We have intentionally presented this briefing as a strategic “trailer” — to establish the depth and immediacy of the findings while preserving the detailed drilldowns and proprietary models that power operational decisions. The full report includes complete segmentation matrices, regional and crop-level demand forecasts, downloadable financial models (USD Million base), and company-level scorecards required to execute on the scenarios above.

To access the full dataset, company scorecards, and implementation playbooks, visit the PW Consulting report page or contact our industry team to schedule a briefing. Our analysts are prepared to run bespoke sensitivity analyses tied to your portfolio or market-entry plan for 2026.

For detailed analysis of this topic, please visit the official page:Worldwide Agriculture Micro Irrigation System Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com