Isopropyl Biphenyl Heat Transfer Fluid Market: Strategic Roadmap for 2026 Decision-Makers

PW Consulting today releases a strategic preview of our forthcoming market study on the Isopropyl Biphenyl (IPB) heat transfer fluid market. The research equips executives, procurement leads, and R&D heads with actionable intelligence to shape investment, sourcing and product strategies as we move into 2026. In short: the market is established, concentrated, and growing at a predictable clip — but the competitive and regulatory vectors that will determine winners and losers in the next three years are nuanced and actionable.

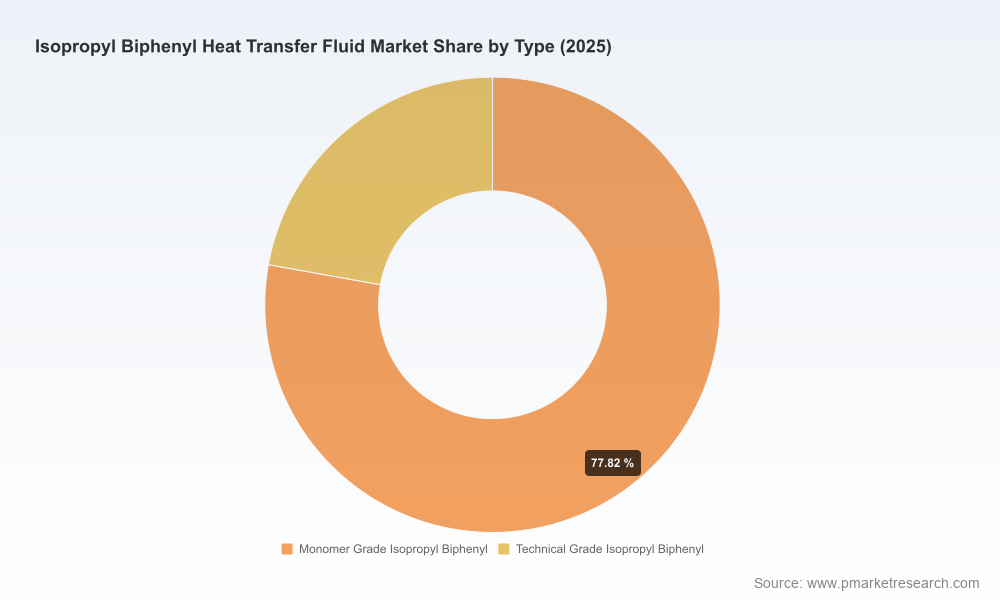

Isopropyl Biphenyl Heat Transfer Fluid Market

Headline market context

Our macro analysis shows the market scale rising from a mid-hundreds million-dollar base in the early 2020s to a larger, more diversified market by the end of the decade. Specifically, total market revenues increased from USD 185.12 Million in 2020 to USD 238.50 Million in 2025 (base year). Under our central forecast, the market is projected to grow to USD 346.61 Million by 2032, reflecting a compound annual growth rate (CAGR) of 5.48% across the 2026–2032 forecast window. These trajectory dynamics combine steady end‑use demand with pockets of premiumization driven by high‑temperature industrial applications and replacement cycles tied to regulatory and environmental drivers.

Isopropyl Biphenyl Heat Transfer Fluid Market

What the report contains — pragmatic deliverables for 2026

- Quantitative market sizing and topline forecast (historical 2020–2025; forecast 2026–2032) with base-year normalization and scenario variants.

- Proprietary vendor scorecards assessing technology, geographic reach, manufacturing capacity, and commercial readiness for rapid scale-up.

- Supply‑chain heat maps that identify single‑point risks in IPB feedstocks, manufacturing capacity concentrations, and logistics chokepoints.

- Regulatory impact assessment assessing legacy PCB phase‑outs, dielectric substitution dynamics, and emerging environmental constraints that could reshape specifications and acceptance timelines.

- Commercial playbooks for buyers and suppliers: procurement levers, contract structures, and inventory strategies tailored to a moderately concentrated supplier landscape.

- Use‑case ROI models for key industrial deployments (high‑temperature thermal loops, CSP, electronics cooling, waste heat recovery) that translate technical performance into TCO outcomes.

- M&A and partnership screens highlighting realistic entry points for market consolidation, backward integration opportunities, and licensing models for proprietary blends.

We intentionally present these headlines and capabilities here while withholding detailed segmented tables and line‑by‑line vendor scoring to preserve the “trailer” effect — a view that demonstrates depth and immediately useful implications while motivating decision‑makers to obtain the full dataset and appendices.

Isopropyl Biphenyl Heat Transfer Fluid Market

Key market dynamics and implications

- Thermal performance premiumization. End users with high temperature setpoints prioritize fluids with wide liquid‑phase temperature windows and long oxidative stability. This creates a tiered market where premium grades command technical preference and, increasingly, contractual commitments around lifecycle management.

- Infrastructure and retrofit demand. Industrial retrofit cycles and investment in waste‑heat recovery and electronics cooling are steady contributors to demand. The predictable replacement cadence of heat transfer fluids supports a stable service and aftermarket opportunity beyond initial sales.

- Regulatory and historical legacy effects. IPB‑based fluids have a notable historical role as replacements for polychlorinated biphenyls (PCBs) following regulatory phase‑outs; this legacy continues to influence procurement specifications and risk assessments, particularly in sectors sensitive to dielectric performance and environmental compliance.

- Supply concentration. The market shows a meaningful degree of supplier concentration at the top end; our concentration metrics indicate that the leading three and five suppliers account for a substantial portion of global supply. This concentration elevates strategic sourcing importance for large end users and increases the attractiveness of backward integration or long‑term supply agreements.

- Raw material and capacity signals. Select manufacturers maintain dedicated annual production capacity for isopropyl biphenyl as an upstream component — a fact that matters for lead times and spot price volatility when demand steps up.

Competitive landscape — who matters and why

The competitive structure is characterized by a mix of global chemical majors and regional specialists. The report assesses technology positioning, certification footprints, global distribution channels and service capabilities for the leading suppliers. Highlights:

- Eastman Chemical Company (Kingsport, TN, USA; https://www.eastman.com) — A global incumbent with Therminol-branded fluids. Eastman’s strength lies in global availability, formulation expertise and a well‑established reputation for high‑purity products suitable for low‑pressure liquid phase systems with elevated bulk temperatures. Their brand position supports premium pricing and preferred supplier relationships in capital‑intensive industries.

- Nippon Chemical Texas Inc. (NCTI) (Texas, USA; https://nctius.com) — Known for SS‑300, a blend that emphasizes thermal stability across a broad temperature window including sub‑zero handling. NCTI’s engineering focus and product suitability for extreme conditions make them a logical partner for niche high‑temperature and cold‑start applications.

- Dalian Richfortune Chemicals (Dalian, China; http://www.richfortunechem.com) — A supplier with offerings positioned as equivalents to established Therminol formulations and with track records in concentrated solar power (CSP) and other industrial projects. Their capability to support large industrial deployments is a differentiator in price‑sensitive segments.

- Jiangsu Zhongneng Chemical Technology (Lianyungang, China; https://www.dynovacn.com) — A regional player delivering IPB‑based fluids across broad temperature bands. Their local manufacturing footprint and product range support rapid regional response and competitive cost structures.

- Manto Chemistry (Jiangsu Manto Chemistry Co., Ltd.; https://mantochem.com) — Produces Mantherm IBP and maintains a dedicated annual production capacity for isopropyl biphenyl (~3,000 tons). This capacity is strategically meaningful for buyers assessing supply continuity and negotiating offtake security.

- Rütgers GmbH (Germany) — Offers Ruetasolv BP series and related isomer blends for high‑temperature applications. Their European base and product quality emphasize regulatory compliance and high‑performance use cases.

Across these suppliers, our vendor assessment shows marked differences in formulation sophistication, service models (e.g., technical advisory for closed‑loop systems), and contractual flexibility. For many buyers, supplier selection will hinge as much on after‑sales engineering support and supply reliability as on per‑unit price.

Strategic implications for 2026 decisions

- Procurement strategy: With a moderately concentrated supply base and predictable growth (CAGR 5.48% in the forecast period), buyers should prioritize multi‑sourcing within a two‑tier strategy: a primary long‑term partner for guaranteed capacity and a secondary supplier for tactical volume. Consider volume‑based price collars and conditional offtakes tied to product quality metrics.

- Supply‑chain resilience: Factor in regional manufacturing footprints and feedstock dependencies. The presence of dedicated IPB production capacity at select suppliers reduces but does not eliminate single‑supplier risk; build inventory buffers and flexible shipping options for projects with strict uptime requirements.

- Product and specification strategy: Differentiate procurement by application class. High‑temperature and electronics cooling use cases justify investment in higher‑grade formulations and lifecycle testing; commoditized thermal loops can leverage cost‑efficient equivalents pending validated performance trials.

- R&D and formulation partnerships: For OEMs and industrial operators, co‑development agreements with established suppliers can secure access to tailored blends and first‑mover advantage in new thermal management concepts, particularly where dielectric performance and oxidative stability are differentiators.

- M&A and strategic partnerships: The observed concentration among top suppliers and steady market growth create fertile ground for bolt‑on acquisitions, joint ventures for localized capacity expansion, and licensing models for proprietary blend IP.

Methodology and confidence framing

PW Consulting’s forecast draws on a multi‑method approach: bottom‑up demand modelling by end‑use, supplier capacity and utilization analysis, price sensitivity scenarios, and expert interviews across supply, OEM and end‑user segments. The report’s base year is 2025, with a historical window spanning 2020–2025 and a forecast horizon of 2026–2032. We apply alternative scenarios to reflect potential acceleration of retrofit programs, regulatory shifts, or feedstock‑driven supply shocks. Our market concentration indicators (three‑ and five‑firm concentration ratios) support robust qualitative inferences about negotiating power and market entry barriers.

Regulatory context and legacy considerations — concise FAQ

- Why does regulatory history matter? IPB‑based fluids gained traction historically as replacements for polychlorinated biphenyls (PCBs) after regulatory phase‑outs, a fact that continues to shape procurement specifications and institutional acceptance in sensitive end markets.

- Are there immediate regulatory risks? Current dynamics emphasize compliance, proper handling, and end‑of‑life management rather than wholesale bans; however, environmental reporting and tighter lifecycle scrutiny are likely to inform purchasing conditions and supplier selection.

- How should buyers prepare? Require supplier transparency on formulation, test data for oxidative and dielectric stability, and commitments to responsible waste management and regulatory compliance in contractual terms.

Next steps — how to use this intelligence in 2026

For executives preparing 2026 capex plans or negotiating multi‑year supply agreements, use the report’s headline projections (base‑year normalization to 2025 and a 5.48% forecast CAGR across 2026–2032) to stress‑test internal demand models and procurement commitments. Prioritize supplier‑led trials where your application’s temperature profile is near the margins of standard product claims. Build contractual flexibility into long‑term agreements to capture potential benefits of scale while mitigating supply concentration risk.

PW Consulting’s full report contains the detailed segmentation, vendor scorecards, downloadable datasets, and appendices required to convert these strategic implications into executable actions. This preview intentionally omits line‑level segmentation tables and vendor scoring to illustrate the report’s scope while preserving the full analytic value for registered clients. For access to the complete study, dataset exports and advisory engagement options, contact PW Consulting or visit our website for the full report release.

For detailed analysis of this topic, please visit the official page:Isopropyl Biphenyl Heat Transfer Fluid Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com