PW Consulting Releases Strategic Brief: Worldwide Industrial Diaphragm Pump Market — Essential Intelligence for 2026 Decision-Making

PW Consulting today publishes a strategic industry briefing accompanying our full market research report, Worldwide Industrial Diaphragm Pump Market (base year 2025, forecast 2026–2032). As global capital allocation, product roadmaps, and regulatory compliance programs are re-evaluated for 2026, this briefing explains how senior executives and operating teams can convert market dynamics into defensible actions. The analysis combines historical performance, near-term forecasts and operational playbooks — offering a high-resolution view of where value pools are forming, while preserving the detailed segment-level tables and modeled scenarios for subscribers to the full report.

Worldwide Industrial Diaphragm Pump Market

Market trajectory: stability with steady expansion

The industrial diaphragm pump market demonstrates resilient expansion. After recovering from early-decade volatility, the global market grew from a multi-billion-dollar base in 2020 to an estimated USD 6.86 billion in 2025 (base year). Our modeling projects a compound annual growth rate (CAGR) of approximately 5.15% across the 2026–2032 forecast window, taking the market toward an expected near‑USD 9.75 billion by 2032 under the baseline scenario. That steady trajectory reflects durable demand in industrial water and wastewater, chemicals, food & beverage, oil & gas, pharmaceuticals, and allied sectors — even as individual end markets cycle.

Worldwide Industrial Diaphragm Pump Market

Why 2026 is a pivotal planning year

- CapEx and replacement cycles align. Many industrial operators plan multi-year equipment refreshes and process upgrades in 2026; diaphragm pumps are frequently core to those projects due to their sealless designs, dosing precision and compatibility with corrosive media.

- Regulatory inflection points demand proactive choices. Stricter effluent and fugitive-emission standards, alongside region-specific explosion-proof requirements, elevate the importance of material selection and certified designs. Equipment procured in 2026 will need to serve compliance horizons extending through the next decade.

- Energy and sustainability targets reframe value. Advances in electric diaphragm technologies and improved system integration mean energy consumption is no longer a secondary consideration for procurement teams; lifecycle energy savings are increasingly central to ROI models.

Key trends and dynamics shaping supplier and buyer strategy

- Sealless designs gain share in hazardous and regulated environments. Compliance trends (ATEX, ISO fugitive-emissions) and the push to reduce leak risk are accelerating demand for diaphragm-based, sealless pump architectures in chemical and petrochemical plants.

- Material and input-cost pressure is structural. Volatility in stainless steel, aluminum and high‑grade elastomers has increased manufacturing cost variability. PTFE remains the leading solution for chemical-resistant diaphragms, underpinned by robust industrial demand for fluoropolymers.

- Electrification and digitalization shift procurement criteria. New electric diaphragm platforms and sensor-integrated models (flow/pressure/vacuum/dosing) allow buyers to optimize total cost of ownership and process control; operators are beginning to quantify energy and performance gains in procurement tender documents.

- Product differentiation relies on system-level engineering. Leading suppliers are pairing pumps with controls, leak-detection, and containment interfaces — moving beyond commodity units to systems that reduce integration risk for OEMs and end users.

- Channel and aftermarket monetization are strategic battlegrounds. With replacement demand steady, aftermarket parts, service contracts and digital predictive-maintenance offerings represent high-margin opportunities for OEMs that can scale technical service capabilities.

What PW Consulting’s report delivers (practical, operational intelligence)

Our report is built for operators, corporate development teams, and procurement leaders who must make justifiable, near-term commitments while protecting optionality. Core deliverables include:

Worldwide Industrial Diaphragm Pump Market

- Validated market-sizing and scenario modeling for 2020–2032, including alternative-demand scenarios tied to regulatory tightening and energy-pricing shocks.

- Segment prioritization frameworks that align product attributes (e.g., elastomer compatibility, pressure ratings, ATEX-certified designs) to buyer requirements across industrial use cases.

- Supply-chain risk maps with mitigation playbooks covering raw‑material concentration, single-source components, and geographic manufacturing exposure.

- Competitor benchmarking and capability matrices that evaluate product breadth, channel strength, service networks and digital features — designed to inform M&A screening and partnership strategies.

- Commercial playbooks: tender language templates, lifecycle-cost calculators, and aftermarket-transition strategies to increase attachment rates for parts and services.

- Investment memos and quick-win lists for new-product initiatives, with estimated payback periods under multiple pricing and input-cost assumptions.

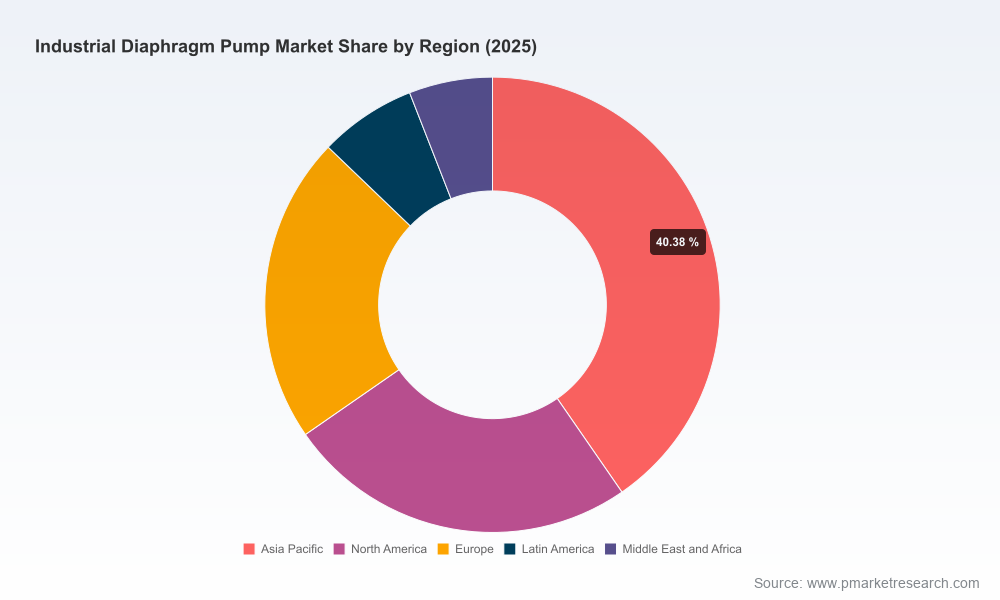

To honor the “trailer” principle of this release, we intentionally withhold the report’s granular segmentation tables and forecast permutations here. Those detailed slices — including regional and application-level revenue allocations and company-level share estimates — are available in the full report.

Competitive landscape — who matters and why

The market is moderately concentrated: established pump OEMs maintain scale advantages through broad installed bases and service networks, while specialized manufacturers compete on niche performance attributes. Executives should weigh three factors when benchmarking suppliers — system engineering capability, aftermarket reach, and regulatory/certification track record.

- Xylem Inc. (Washington, DC) — leverages water-treatment expertise to offer diaphragm-based solutions within broader positive-displacement portfolios focused on municipal and industrial water applications.

- Wanner Engineering (Hydra-Cell) (Minneapolis) — known for high-pressure, seal-less positive-displacement designs suitable for demanding industrial fluid-handling tasks.

- Graco Inc. (Minneapolis) — dual strategy across air-operated and electric diaphragm platforms, including high‑chemical-resistance ChemSafe paths and energy-efficient QUANTM electric units.

- Dover Corporation (PSG brands: Wilden, Blackmer, All‑Flo) (Downers Grove) — large portfolio serving chemical and sanitary markets, with strong distribution channels for AODD technologies.

- Ingersoll Rand (ARO) (Davidson) — offers both air-operated and electric pumps, emphasizing reliability and industrial-grade specifications for process plants.

- IDEX Corporation (Warren Rupp / Sandpiper) (Northbrook) — recognized for AODD pumps targeting heavy-duty industrial and mining applications.

- Grundfos, Flowserve, Yamada, Tapflo, Verder and others — collectively provide a mix of dosing, hygienic, corrosive‑service and high-performance units that span global OEM and aftermarket needs.

- Regional specialists — firms such as KNF, ProMinent, LEWA and others bring precision dosing, gas-handling and high‑pressure metering expertise that is mission‑critical in pharmaceutical and specialty-chemicals applications.

Near-term product and M&A watch — signals for 2026

- Sensor integration and smart dosing: recent product launches include sensor-enabled diaphragm pumps with integrated flow, pressure and vacuum control — a trend that favors suppliers with electronics and software development capabilities.

- High-flow electric units and pressure-relief controllers: new electric diaphragm models introduced at major trade shows demonstrate widening replacement opportunities for legacy air-operated equipment in energy-conscious plants.

- M&A focus areas: buyers will target firms that enhance digital service stacks, expand aftermarket footprint in fast-growing industrial water segments, or add certified hazardous‑area designs.

How executives should use this intelligence in 2026

- Procurement leaders: Incorporate lifecycle energy and compliance metrics into RFP scoring; require supplier roadmaps for material security and regulatory certification timelines.

- Product and engineering teams: Prioritize modular designs that support PTFE and high‑elastomer variants, and accelerate sensor-integration pilots to capture aftermarket service revenues.

- Corporate development: Use the report’s benchmarking outputs to screen acquisition targets that close capability gaps in control electronics, aftermarket service scale, or hazardous‑area certified product lines.

- Service organizations: Build predictive-maintenance offerings tied to performance data; structure contracts to convert one-time sales into recurring revenue streams.

About the methodology and validation

PW Consulting’s modeling combines primary interviews with OEMs, distributors and end users, proprietary shipment data, and a bottom‑up bill‑of‑materials analysis to reconcile supply‑side economics with end‑use consumption. We stress‑test projections against three macro scenarios (baseline, regulatory acceleration, input‑cost shock) and produce actionable sensitivities for capital planners and M&A teams.

Next steps — where to get the full intelligence

This briefing is an executive synopsis designed to surface the strategic implications of our findings for 2026 planning. The full Worldwide Industrial Diaphragm Pump Market report includes the detailed segment-level forecasts, regional and application revenue breakdowns, company market shares, modelled supplier scorecards, and downloadable financial templates for scenario testing.

For access to the complete report and proprietary datasets — including the detailed segmentation tables withheld from this release — please visit our report page or contact PW Consulting’s industrial fluids practice. Subscribers gain immediate access to the data visualizations, decision‑grade models and a briefing session with our senior analyst team to align findings to your 2026 priorities.

PW Consulting — helping executives convert market clarity into confident, executable strategy.

For detailed analysis of this topic, please visit the official page:Worldwide Industrial Diaphragm Pump Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com