Understanding FEMA Export and Import Regulations: A Complete Guide for Indian Businesses

Other |

2026-06-25 07:50:03

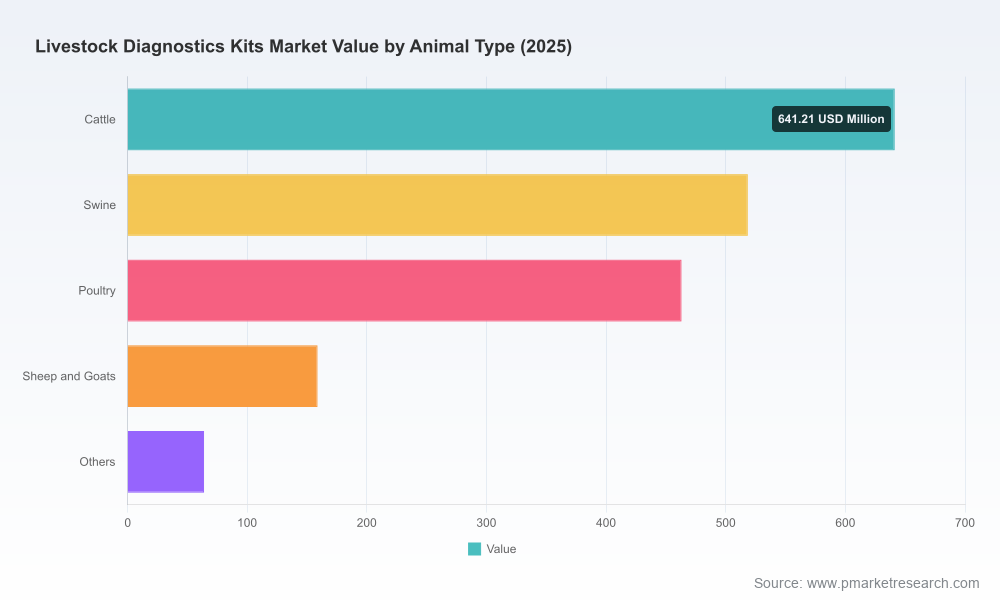

As PW Consulting’s senior industry analyst team, we present a concise strategic preview of our full Worldwide Livestock Diagnostics Kits Market report to support executive decision-making in 2026. The diagnostics kits market for production animals has moved from niche surveillance tools to a central enabler of biosecurity, trade resilience, and farm-level productivity. Our analysis shows the market expanding from approximately USD 1.28 billion in 2020 to USD 1.845 billion in the report’s base year (2025), and we forecast continued growth to roughly USD 3.16 billion by 2032 at a compound annual growth rate (CAGR) of 8.0% across 2026–2032. This brief synthesizes the practical implications executives need now — while preserving the proprietary segmentation matrices and granular forecasts that are published in the full report.

Worldwide Livestock Diagnostics Kits Market

Diagnostic kits for livestock are strategically important for animal health managers, integrated protein producers, diagnostic OEMs, distributors, and public sector agencies. The market’s sustained mid-single-digit to high-single-digit growth is being driven by three converging forces: heightened regulatory scrutiny and harmonization of validation standards; technology-led shifts toward point-of-care (PoC) and multiplex molecular assays; and commercial pressure for faster, lower-cost testing across farm-to-fork value chains. For 2026, companies should treat diagnostic kits not simply as consumables but as platforms that connect data, operations, and compliance into farm-level decision loops.

Worldwide Livestock Diagnostics Kits Market

Two structural features define the market landscape. First, scale and concentration: the market is moderately concentrated with the top three suppliers controlling nearly half of industry revenues and the top five accounting for close to three-fifths — indicating that partnerships, selective M&A, and differentiated value propositions are decisive. Second, technology convergence: established immunoassay formats remain essential for surveillance, while PCR and multiplex molecular solutions are gaining ground for their sensitivity and traceability. Simultaneously, lateral flow and rapid PoC formats are being optimized for on-farm usability and integration with digital reporting systems.

Worldwide Livestock Diagnostics Kits Market

Regulatory and trade considerations are also central. International validation frameworks (such as WOAH’s register and standardized validation procedures) and national guidance (for example, recent USDA APHIS clarifications on validation and shelf-life for immunodiagnostics) are raising the bar for evidentiary dossiers and post-market surveillance. Export-dependent producers must anticipate that diagnostic kits used for certification will be judged against importing country requirements, often aligned with international standards — a dynamic that converts regulatory compliance into a competitive asset.

Against these dynamics, executives should prioritize a three-track agenda for 2026 that balances growth, risk mitigation, and capability building.

The competitive field is a blend of global life-science leaders, specialized veterinary diagnostics companies, and regional technology innovators. The most influential players combine an installed base of laboratory instruments with consumable portfolios and field-ready rapid tests. Representative firms covered in our competitive analysis include:

Recent market events illustrate how product innovation and platform launches will continue to re-shape competition. For example, Zoetis’ roll-out of cartridge-based PoC hematology analyzers and IDEXX’s expansion of diagnostic panels underscore the ongoing cadence of strategic product introductions. These launches presage a competitive era where hardware-enabled diagnostics and ecosystem services matter as much as kit accuracy itself.

Regulators are tightening standards for validation and transparency. WOAH’s register and standardized validation pathways are becoming de facto benchmarks for international acceptance of tests, while USDA APHIS guidance refines expectations around production outlines and expiration dating. Certain assays remain restricted to authorized reference laboratories in some jurisdictions, which affects commercial rollouts and channel strategies. Practically, companies should budget for longer pre-launch cycles, invest in third-party validation partnerships, and embed regulatory strategy at the earliest stages of R&D.

Our full report is deliberately operational and decision-oriented. Highlights include:

Use this preview to prioritize internal convenings and to stress-test near-term budgets. Recommended immediate actions:

This strategic preview establishes the contours of opportunity and risk for the livestock diagnostics kits market as companies plan for 2026. The full PW Consulting Worldwide Livestock Diagnostics Kits Market report contains the proprietary segmentation, regional breakdowns, and granular scenario-models that will enable precise budgeting and target-setting — information we intentionally withhold here to preserve the value of the full intelligence package.

For teams preparing investment memoranda, commercialization plans, or regulatory dossiers, accessing the complete report will convert this strategic preview into executable initiatives. Contact PW Consulting’s report team to secure the comprehensive dataset, model files, and executive workshop sessions that translate these insights into measurable business outcomes.

For detailed analysis of this topic, please visit the official page:Worldwide Livestock Diagnostics Kits Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com