Best Business Listing Sites to Improve Google Rankings

Other |

2026-05-07 13:00:43

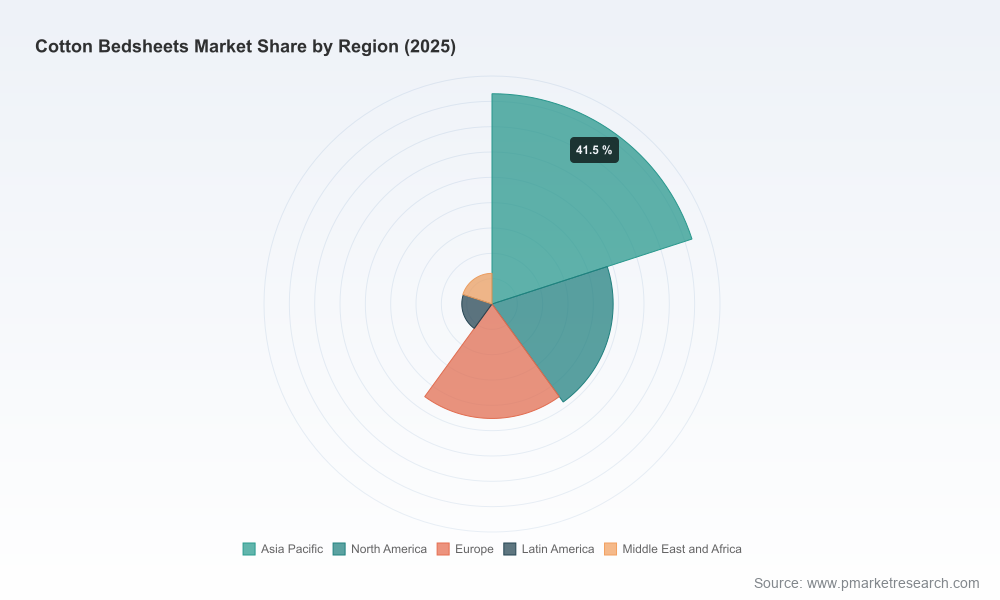

As global bedding demand normalizes into a new post-pandemic rhythm, PW Consulting’s latest market study — the Worldwide Cotton Bedsheets Market (base year 2025; historical period 2020–2025; forecast 2026–2032) — reframes the sector for executive decision-makers planning commercial and capital strategies in 2026. The market reached approximately USD 18,650 million in 2025 and, on the basis of our model, will expand at a compound annual growth rate (CAGR) of 5.12% across the 2026–2032 forecast window. By 2032 the market trajectory supports a sizeable uplift versus the 2025 baseline, driven by a mix of structural demand, premiumization, and supply-side shifts.

Worldwide Cotton Bedsheets Market

Capital allocation: A mid-single-digit CAGR backed by resilient end-use demand validates selective capacity investments that prioritize differentiation (premium cotton lines, certified organic, performance finishes) over broad-volume plays.

Worldwide Cotton Bedsheets Market

M&A and strategic partnerships: Fragmentation in the supplier base creates opportunities for roll-ups focused on scale in procurement, specialized finishing, or distribution control. Our concentration analysis indicates the market remains largely fragmented, with top-three players accounting for a relatively small share of total revenue — an important signal for acquirers seeking consolidation upside.

Worldwide Cotton Bedsheets Market

Risk management: Raw-material price volatility and trade-policy shifts require integrated procurement strategies and hedging frameworks to stabilize margins into 2026.

PW Consulting’s topline forecast synthesizes sales, inventory cycles, and leading indicators across retail, hospitality and institutional channels. With a 2025 market value of roughly USD 18.65 billion and a modeled CAGR of 5.12% for 2026–2032, the sector presents consistent growth potential while exhibiting episodic sensitivity to cotton pricing and trade actions. Our scenarios show that demand resilience is strongest among premium and sustainability‑oriented product tiers, and that hospitality rebounds continue to be a second-order driver as travel and lodging markets stabilize.

Premiumization and direct-to-consumer (DTC) channels: Consumers continue to trade up for differentiated hand-feel, transparency of origin, and brand promise. Brands that can credibly couple quality claims with supply-chain traceability will capture disproportionate value.

Sustainability as a margin lever: Certifications and traceability — especially in organic and ethically sourced cotton — are becoming purchase determinants. In many instances, certified products command price premiums and support retailer shelf differentiation.

Raw-material dynamics: Global cotton production for the 2025/26 season was projected at approximately 121.9 million bales against world consumption near 119.1 million bales, per USDA FAS. Price signals are heightened: U.S. season-average farm prices were forecast at about $0.61 per pound for 2025/26 while cotton futures approached near‑two‑year highs around $0.80 per pound in April 2026. These inputs materially affect cost stacks for mills, converters, and brand margins.

Trade and policy friction: Tariff actions and policy changes — including escalations and expirations of exclusions under U.S. Section 301 measures in 2025 — are already influencing sourcing strategies and landed costs for import-dependent players.

Institutional demand subtleties: Healthcare and hospitality requirements continue to prioritize durability, ease of care, and in some cases antimicrobial finishes — a source of stable OEM relationships and recurring demand.

Commodity shock scenario: A sustained spike in cotton prices or supply disruptions could compress margins unless partially offset by index‑linked procurement, vertical integration, or product re-engineering to alternative blends.

Trade-policy escalation: Broader tariff measures or non-tariff barriers targeting key sourcing corridors would raise landed costs and favor nearshoring or regionalization of production networks.

Geopolitical and climate exposure: Concentration of raw-material production in weather‑sensitive regions underscores the need for diversified supplier portfolios and crop‑risk assessments.

The market’s competitive map is populated by large vertically integrated textile groups, specialty manufacturers, premium DTC brands, and hospitality-focused suppliers. Leading manufacturers from India and the United States exhibit contrasting go‑to‑market plays: scale-oriented exporters and converters emphasize cost and distribution breadth, while U.S. incumbents and DTC brands lean into innovation, customer experience and premium claims.

Established exporters and large manufacturers: Companies with large-scale production and integrated supply chains maintain advantages on cost, lead time, and the ability to serve global retail and hospitality chains. For 2026, their strategic playbooks should include targeted product premiumization, sustainability credentialing, and selective automation investments to protect margins amid input price pressure.

Vertically integrated players: Firms that own fiber-to-finished capabilities can better control quality and partial margin capture. For corporates considering M&A, targets that fill capability gaps (e.g., finishing technologies, certification pipelines, or regional distribution) are high priority.

Premium and DTC brands: Consumer-facing brands that emphasize organic cotton and ethical sourcing are positioned to command higher ASPs but must invest in brand durability and supply-chain transparency to scale profitably.

Hospitality and institutional suppliers: Vendors focused on hospitality must balance durability and cost; opportunities exist in product systems (bedding + sheet + laundry program) that lock in recurring revenue.

Notable recent activity — for example, the introduction of a new 100% cotton bath and bedding line by a U.S. manufacturer in late 2025 — underscores continued product development momentum and the importance of trusted provenance marks for consumers and purchasing managers alike.

Our report is expressly designed for commercial leaders, procurement heads, corporate development teams and investors preparing decisions for 2026. Delivered as an actionable toolkit, the study blends quantitative forecasts and qualitative playbooks without diluting practical application:

Topline market model (historical 2020–2025; forecast 2026–2032) with sensitivity scenarios around commodity and tariff shocks.

Segmentation analytics (by region, material type, and end-user) with stratified revenue pools and demand drivers. Note: this release omits the detailed segment tables — full segmented data and downloadable models are accessible via the full report page.

Supply-chain heatmaps identifying freight, finishing, and manufacturing bottlenecks, plus supplier risk scoring tailored to procurement horizons.

Price and input analysis tied to global cotton balances, futures dynamics and farm-price forecasts to support hedging and sourcing strategies.

Competitive benchmarking covering capability gaps, brand positioning, and M&A target screening criteria matched to varied buyer archetypes.

Commercial playbooks for three priority investment types: premiumization & DTC scaling, hospitality program expansion, and regional nearshoring.

Regulatory and trade monitoring templates to operationalize tariff impact assessment (including HS classifications relevant to cotton bed linen).

Prioritize procurement resilience: implement multi-source contracts, add cotton-index hedging where feasible, and develop contingency inventory buffers for peak seasons.

Invest selectively in product differentiation: differentiate through verified sustainability claims, performance finishes and textile innovation that justify price premiums.

Pursue bolt-on acquisitions that close capability gaps — finishing technologies, certification expertise, or last‑mile distribution — rather than large scale roll-ups that dilute focus.

Reconfigure supply networks to mitigate tariff exposure: nearshore in strategic markets where tariffs or logistics create outsized landed-cost risk.

Embed scenario planning into commercial forecasts: run downside cases tied to commodity price spikes and trade escalations so procurement and pricing teams can respond within weeks, not months.

The report base year is 2025, with historical analysis covering 2020–2025 and a forecast horizon of 2026–2032. Our quantitative model synthesizes demand-side indicators, trade flows, company filings, and primary interviews across supply‑chain nodes. Scenario analyses incorporate commodity outlooks (including USDA FAS production/consumption balances and observed futures behavior) and trade-policy permutations. Detailed appendices document sources, assumptions, and sensitivity runs.

This executive release is intentionally selective — it surfaces strategic conclusions and operational priorities while withholding the granular segment tables and downloadable forecasting models that corporate teams require for implementation. To obtain the full dataset (including the segmented revenue pools, downloadable Excel model, company scorecards and playbooks), please visit PW Consulting’s report page for the Worldwide Cotton Bedsheets Market. The full report is equipped with tools to run custom scenarios tailored to your procurement profile, channel mix, and investment horizon.

For boards, corporate development teams, and investors preparing decisions in 2026, our analysis converts global market signals — from cotton bale balances and futures volatility to tariff cycles and consumer premiumization — into a concise, action-oriented agenda. PW Consulting stands ready to support tailored workshops and scenario runs to align your 2026 strategic plan with the market pathways that matter.

For detailed analysis of this topic, please visit the official page:Worldwide Cotton Bedsheets Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com