Worldwide Robotic Scope Holder Market — Strategic Outlook for 2026 Decision‑Makers

PW Consulting’s latest market study on Worldwide Robotic Scope Holders (base year 2025; forecast period 2026–2032) delivers a focused intelligence package designed to inform boardroom choices in 2026. The market has matured into a clearly investable niche: the industry reached approximately USD 310 million in 2025 and is forecast to expand at a 7.5% CAGR through 2032, approaching a half‑billion‑dollar industry by the end of the forecast period. This trajectory reflects accelerating clinical adoption, platform integrations with surgical robotics, and incremental regulatory clarity — all of which raise the strategic stakes for device manufacturers, hospital systems, and private capital alike.

Worldwide Robotic Scope Holder Market

What this report delivers — practical intelligence for immediate action

- Robust market model and demand scenarios: a granular bottom‑up model that reconciles historical performance (2020–2025) with scenario paths for 2026–2032, enabling sensitivity testing against adoption rates, reimbursement shocks, and technology inflections.

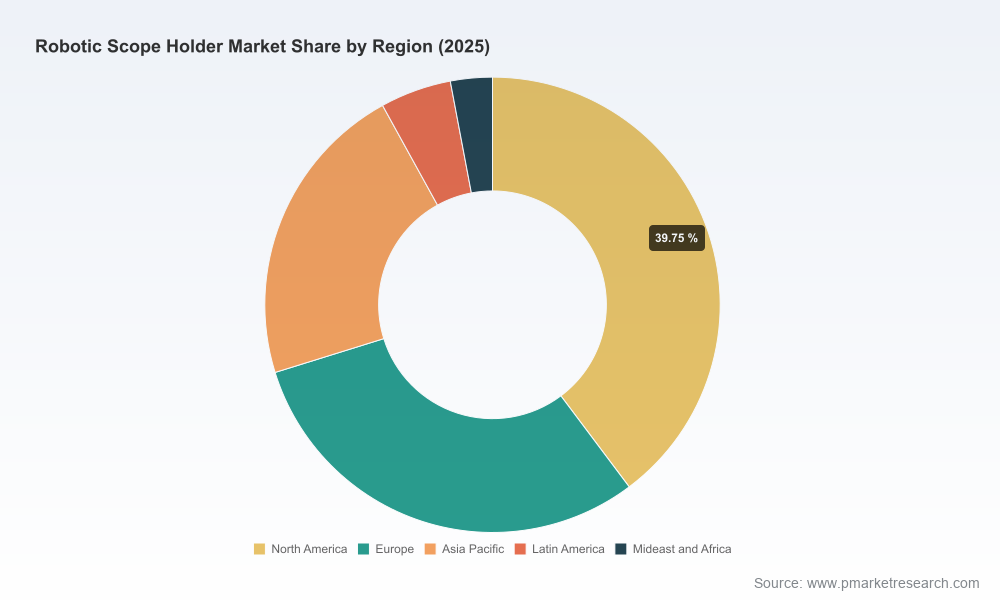

- Segment architecture without data leakage: segmentation across regions, product types (autonomous vs. semi‑autonomous), and surgical applications, together with reproducible segmentation logic you can adapt to your portfolio decisions (note: the executive summary demonstrates overall trends while preserving segment-level tables for report subscribers).

- Actionable go‑to‑market playbooks: channel strategies for OEMs and medtech entrants, procurement templates for hospital procurement offices, and service/consumable monetization strategies that materially improve lifetime customer value.

- Competitive intelligence and vendor scorecards: primary profiles and strategic benchmarking for incumbents and fast followers, including product capabilities, regulatory posture, and partnership footprints.

- Regulatory, reimbursement and clinical pathway maps: end‑to‑end compliance checklists, CPT/reimbursement alignment, and readiness requirements for IEC and FDA pathways.

- M&A and partnership heat maps: targets and partner archetypes prioritized by technology, IP, installed base and go‑to‑market fit.

Key market dynamics shaping 2026 decisions

- Platform convergence: Robotic scope holders are shifting from point products to interoperable modules that either integrate with larger surgical robots or sit alongside hybrid OR platforms. Recent product updates and demos show voice control, advanced kinematic freedom and AI‑assisted positioning are now expected features rather than differentiators.

- Clinical adoption powered by workflow economics: Hospital uptake is increasingly driven by measurable OR efficiencies — steadier camera control, fewer assistant FTEs per OR, and improved turnover times. Buyers prioritize total cost of ownership and clinical throughput gains over one‑time CAPEX alone.

- Regulatory clarity reduces market friction: Compliance to standards such as IEC 60601‑1 and a mature FDA 510(k) pathway for Class II devices lower entry barriers for established medtech players and raise the bar for newcomers on safety documentation and clinical evidence.

- Reimbursement alignment matters: Existing CPT descriptors for computer‑assisted navigation and scope positioning create an avenue for capture; organizations that map clinical coding and economic cases early enjoy faster contract wins with hospital procurement teams.

- Material and sterilization constraints shape product design: Medical‑grade stainless steel and titanium alloys, with autoclave cycles up to 134°C, are the default. These constraints impact strategic choices around disposable vs. reusable interfaces, warranty models, and service infrastructure.

Competitive landscape — incumbents, capability clusters and tactical moves

The market is concentrated, with a small set of vendors controlling a meaningful share of revenue and installed base, creating both competitive pressure and collaboration opportunities. Leading firms demonstrate three distinct capability clusters: integrated surgical platform suppliers, specialized robotic scope holder OEMs, and workflow/software oriented players that enable interoperability and analytics.

Worldwide Robotic Scope Holder Market

- Product‑centric incumbents: Companies producing multi‑axis scope holders with advanced ergonomics and integration capabilities are differentiating on reliability and OR integration. Recent product improvements such as enhanced AI‑assisted positioning and extended kinematic range reflect a maturation of the core mechanical platform.

- Regulatory and market enablement: Vendors that have secured broad regulatory clearances and global distribution (including FDA 510(k) expansions) occupy privileged negotiation positions with health systems and are preferred partners for larger system integrators.

- Clinical workflow innovators: Firms emphasizing voice control, seamless interoperability with endoscopes and analytics around OR utilization are making the strongest case for differentiated value capture beyond hardware sales.

Representative company moves underscore these dynamics. Vendors have introduced AI positioning upgrades and showcased hybrid integration at major surgical congresses; one acquired platform continues to benefit from expanded regulatory filings. These events demonstrate that iterative product evolution, regulatory momentum and trade‑show validation are key signals for investor diligence and buyer shortlists.

Worldwide Robotic Scope Holder Market

Regulatory, reimbursement and supply considerations

- Regulatory: Design and quality systems must align with IEC 60601‑1 electrical safety requirements and the established Class II/510(k) pathways where relevant. Expect regulators to scrutinize software updates (AI assistance/positioning) as changes that may trigger additional documentation.

- Reimbursement: CPT codes covering computer‑assisted positioning exist and should be mapped against hospital revenue cycles to quantify per‑case economics. Early coordination with coding teams accelerates value realization.

- Materials & sterilization: Device architecture must account for autoclave compatibility and durable alloys to meet infection control protocols. Decisions here trade off upfront component costs, instrument longevity, and service burden.

Decision‑maker playbook for 2026 — five prioritized moves

- Prioritize interoperability investments: Allocate R&D and partnership budgets to ensure your scope holder integrates smoothly with dominant surgical robots and endoscopy platforms; interoperability reduces sales friction and speeds adoption.

- Lock down regulatory and clinical evidence pathways: If deploying AI positioning or software updates, define premarket documentation and postmarket surveillance now to avoid rollout delays and to reassure early adopters.

- Create clear economic narratives for procurement: Build hospital-facing value cases that quantify OR time savings, FTE redeployment, and per-procedure economics tied to local reimbursement rules. Embed CPT mapping and payer scenarios in commercial materials.

- Design a service and pricing ladder: Consider blended models — capital sale with premium service contracts, or consumable plus subscription — to balance hospital procurement preferences and to maximize lifetime value.

- Scan M&A for capability gaps: Use targeted acquisitions to accelerate software, AI or global distribution capabilities rather than attempting long, uncertain internal builds.

KPIs and scenario metrics to monitor in 2026

- Adoption velocity: installations per quarter vs. forecast model; attach rate of software modules and consumables to hardware deals.

- Operational impact: OR time saved per case, case volume uplift per OR, and reduction in camera‑operator staffing hours.

- Revenue mix: share of recurring service & consumable revenue vs. hardware, and geographic revenue diversification.

- Regulatory milestones: time to clearance for software updates or new configurations and postmarket event rates.

- Market concentration shifts: monitor top‑three and top‑five vendor shares to anticipate pricing pressure or consolidation opportunities.

Why this report is essential for 2026 planning

For executives making 2026 capital allocation, product roadmap or M&A decisions, the critical choice is not whether the market grows — macro momentum is clear — but which tactical path captures disproportionate value as the ecosystem consolidates. Our study gives leadership three advantages: a validated market sizing and scenario engine keyed to a 7.5% CAGR through 2032; an executable set of go‑to‑market and regulatory playbooks; and a competitor map that highlights who is investing in AI‑assisted positioning, voice control workflows, and platform integrations.

Importantly, the report follows a "trailer" approach: we provide clear signposts and operational frameworks that let you evaluate strategic fit and risk, while reserving detailed segment tables, modeled revenue splits and deal‑level analysis for report subscribers. That balance ensures you can act on high‑confidence insights immediately while accessing the full dataset and vendor scorecards when you’re ready to execute.

Next steps — how to use this intelligence

- For OEMs and investors: prioritize interoperability pilots with anchor hospital partners, validate coding/reimbursement capture on pilot cases, and evaluate tuck‑in acquisitions to close software or distribution gaps.

- For hospital systems: include scope‑holder TCO and OR throughput metrics in 2026 capital planning, and require interoperability and service SLAs in procurement RFPs.

- For private equity and strategic buyers: use the report’s M&A heat map and vendor scorecards to build a 12–24 month acquisition roadmap that maximizes synergies across platforms, consumables and services.

To access the full dataset, vendor scorecards and downloadable modeling tools, please visit the Worldwide Robotic Scope Holder Market report page on the PW Consulting website. Our team is also available for bespoke briefings and scenario workshops tailored to your strategic timeline for 2026.

For detailed analysis of this topic, please visit the official page:Worldwide Robotic Scope Holder Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com